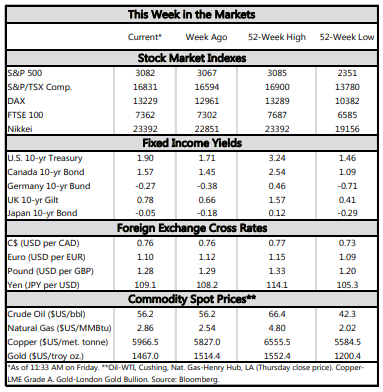

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- It was a relatively quiet week for economic data. The trade deficit narrowed a bit in September, but new tariffs appear to have weighed on both exports and imports. The ISM non-manufacturing index followed its manufacturing counterpart higher in October, with the recent trend indicating a stabilization in activity.

- Trade negotiations continued to dominate headlines. Comments from the U.S. Commerce Secretary suggest that the U.S. is likely to avoid a major escalation in trade tensions with Europe next week over autos.

- The interim U.S.-China trade deal is unlikely to be signed this month, but the mid-December tariffs still appear likely to be scrapped. Pres. Trump poured cold water on the notion that there was an agreement on removing existing tariffs.

The Deal With The Deal

The ISM non-manufacturing report, on the other hand, ushered in a bit of optimism. The headline index followed its manufacturing counterpart higher in October, with the improvement broad-based across the subcomponents. While a bit better than expected, the October uptick was not large enough to offset the decline in the month prior. As such, instead of a major strengthening in the pace of expansion, the recent trend is more indicative of a stabilization in activity (Chart 1).

Other second-tier data reports did little to rock the boat. Of note, job openings continued to edge lower in September, reinforcing the notion that appetite among U.S. employers for labor, while elevated, has waned a bit recently. The September data also affirmed that the pullback in job openings so far has limited geographic breadth, with recent pressures concentrated in the Midwest (Chart 2; for more see here).

When it came to China, developments were more capricious. For starters, contrary to initial hopes, the Trump-Xi meeting to sign the ‘Phase One’ trade deal is unlikely to happen this month. On the other hand, it appears likely that the tariffs that were slated to go into effect in mid-December will still be scrapped (provided that the interim deal remains on track to be signed in the near-term). China’s Commerce Ministry spokesperson suggested that the two economic heavyweights had agreed to roll back existing tariffs in phases as trade talks advanced. But this morning, President Trump poured cold water on the notion of such an agreement, while also stating that he will not fully eliminate tariffs on China. This softened some of the optimism that had built from China’s earlier announcement, highlighting the delicate and volatile nature of trade negotiations.

All in all, there are indeed signs of a de-escalation in trade tensions, which help dilute some of the near-term risk as economic activity shows signs of stabilizing. But, as today’s events have shown, we caution against reading too much into the recent optimism, for as long as core issues remain unaddressed, a re-escalation in the trade war remains a distinct possibility.

Admir Kolaj, Economist | 416-944-6318

Financial News for the week of Nov. 8, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.