FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

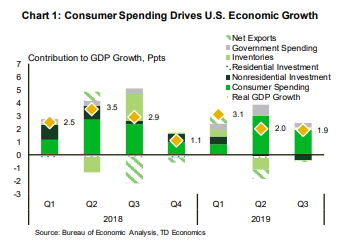

- U.S. economic activity decelerated in the third quarter to a 1.9% annual pace from 2% in the second quarter, with consumer spending doing much of the heavy lifting.

- The Federal Reserve implemented its third, and likely final, interest rate cut of this year, citing muted inflation pressures and staid global developments. The bar for future rate cuts, however, has shifted higher

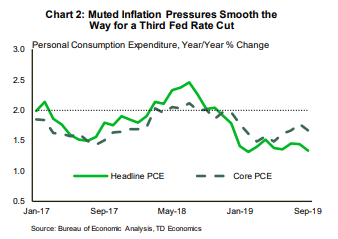

- PCE inflation continues to undershoot the Fed’s 2% target, with the headline measure at 1.3% year-on-year and core at 1.7%..

Consumers Step-Up, Businesses Pull-Back

Other big entries did not fare as well. Most notably, business investment declined for the second straight quarter (-3%), while net exports and inventories were minor drags. The falloff in business spending is the worst performance since late 2015, reflecting a confluence of factors ranging from slowing global growth, rising trade protectionism, and elevated policy uncertainty to appreciation of the U.S. currency. On the flipside, residential investment, having declined for six consecutive quarters, finally returned to positive territory, spurred by falling interest rates and high demand for homes.

The headline PCE price index rose 1.3% y/y in September, while the core measure, the Fed’s preferred inflation gauge, was up 1.7% – well below its 2% target (Chart 2). This allowed the Fed ample room to implement its third consecutive quarter point cut, lowering the fed funds target range to 1.50%-1.75%. Although some easing bias remains, the accompanying policy statement signaled a higher bar for future interest rate reductions. The two previous cuts appear to be paying off by giving a lift to household spending in the most interest rate sensitive areas, such as housing and autos. This outcome has helped to offset a slump in manufacturing. Encouragingly, that slump eased a bit in October, with the ISM manufacturing sentiment index ticking up to 48.3 from 47.8 in September (see report).

Across the pond, Britain not only got a Brexit extension but also an early election. The Brexit deadline was extended to Jan. 31, while British lawmakers voted to hold a December 12th election. This paves the way for one of the most unpredictable and divisive national ballots in Britain, but inches the Brexit issue closer to resolution.

Overall, it appears a healthy jobs market, supported by monetary easing is keeping Americans spending (though with less gusto than before), and helping to make up for a shortfall in business investment.

Shernette McLeod, Economist | 416-415-0413

Financial News- November 1, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.