FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The economic data was subdued this week. Retail sales fell 0.3% in September, ending their six month growth streak. Industrial production also fell. Multifamily starts took a step back, but single-family starts fared better.

- The Fed’s Beige Book confirmed that economic activity has moderated in the period covering mid-August through September. Tariffs, prolonged uncertainty and slower global growth were deepening the manufacturing slump and pushing businesses to trim their growth outlooks.

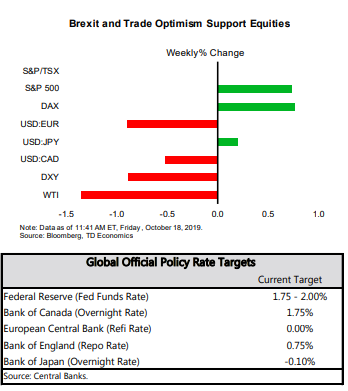

- Internationally, the U.K. and the E.U. have agreed on the new Brexit deal, but the bigger hurdle of getting the deal through parliament still looms. Meanwhile, China’s economy grew 6.0% (y/y) in Q3, the slowest pace since 1992.

Economy Sends Mixed Signals

Across the pond, the U.K. and the E.U. have agreed on the new Brexit deal. The news boosted the British Pound to its highest level since May, even though the bigger hurdle of getting the deal through parliament this Saturday still looms. Meanwhile, Chinese GDP data reaffirmed that the U.S.-China trade war was weighing on economic growth. Real gross domestic product (GDP) rose 6.0% year-on-year (y/y) in the third quarter of 2019, a tenth of a point below market expectations, and the slowest pace since data collection began in 1992. “Synchronized slowdown” across major economies and slumping international trade has led the IMF to downgrade it’s global growth forecast for 2019 to 3% – down 0.2pp from its the previous release in July.

State-side, the economic data flow was mixed this week. September’s retail sales report showed that American shoppers appeared to have switched into a hibernation mode as cooler weather set in. Retail sales fell 0.3% in September, ending their six month growth streak (Chart 1). Even online sales took a breather, edging lower for the first time since last December. However, consumer activity remained healthy on a quarterly basis, with sales up 6% (annualized) in Q3. This leaves our third quarter tracking for consumer spending just shy of 3% – a downshift from the second quarter, but still a solid print. Still, with consumer spending currently being a key driver of economic growth as activity slows in other sectors, the decline in September will not escape the Fed’s attention ahead of the FOMC meeting at the end of the month.

These developments were corroborated by the Fed’s Beige Book this week. The report confirmed that economic activity has moderated in the period covering mid-August through September. Tariffs, prolonged uncertainty and slower global growth were deepening the manufacturing slump (echoed in the industrial production data this week) and are pushing businesses to trim their growth outlooks. The limited agreement between China and the U.S. reached last week is unlikely to do much for the business climate while tariffs remain in place. With no signs of stabilization in domestic economic backdrop, the Fed will likely continue to err on a side of caution, opting to support the economy with another interest rate cut this year.

Ksenia Bushmeneva, Economist | 416-308-7392

Financial News- October 18, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.