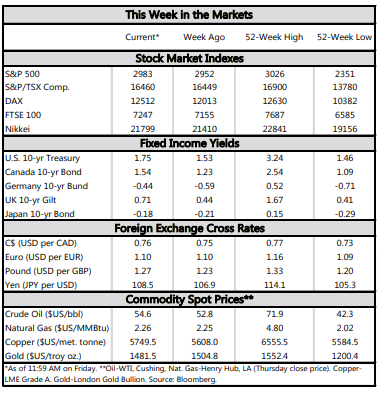

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- CPI report – the only key data release this week – confirmed that inflation remained tame in September. Both headline and core inflation registered a muted 0.1% increase on the month, leaving the readings flat on a year-over-year basis.

- Meanwhile, the JOLTs survey showed that worker demand had softened over summer. The number of job openings fell in August on a year-on-year basis – a third drop in as many months.

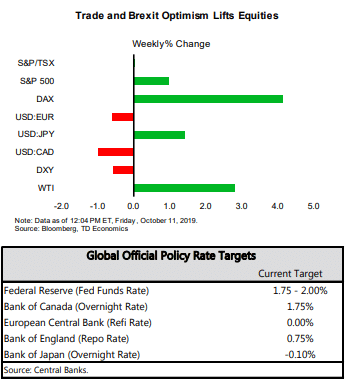

- Unless a breakthrough in the U.S.- China trade impasse is reached later today, benign inflation and further signs of the domestic economy cooling off should lead to an even broader agreement for further monetary easing among the FOMC members when they meet later this month.

Fed Leaves the Door Open for Another Cut

The new leaders of the IMF and World Bank warned about the deteriorating global economic backdrop ahead of their annual meetings next week. The new head of the IMF, Kristalina Georgieva, said that the global economy is now in a “synchronized slowdown”, and that the IMF expects slower growth than last year in 90% of the world. The new head of the World Bank, David Malpass, in turn highlighted the long list of looming risks, such as “Brexit, Europe’s recession, and trade uncertainty,” which may lead to a further downgrade to their global growth estimate.

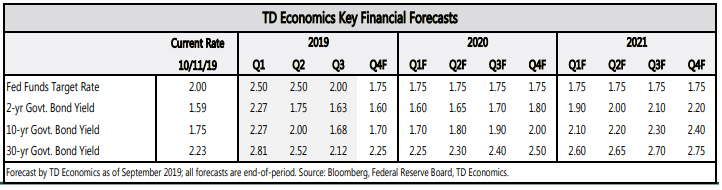

Chair Powell expressed similar concerns in his speech this week, acknowledging that the U.S. economy has slowed. He also reaffirmed that while the 50 basis point reduction in the fed funds rate so far is providing support, the FOMC committee will continue to assess incoming data signals on a meeting-by-meeting basis. The next meeting will take place at the end of October, and markets are expecting another quarter-point rate cut. Powell’s speech this week did not dispel those expectations, with the chairman reiterating that “policy is not on a preset course”.

Separately, the NFIB small business confidence index showed that businesses may be stuck between a rock-and-a-hard place, as they face rising costs (especially for labor), but are unable (or unwilling) to increase selling prices (Chart 2). Indeed, despite new tariffs coming into effect in September on many consumer goods, inflation remained tame. Both headline and core inflation registered a muted 0.1% increase on the month, leaving the readings flat on a year-over-year basis at 1.7% and 2.4%, respectively. Unless a breakthrough in the trade impasse is reached later today, benign inflation and further signs of the domestic economy cooling off should lead to even more agreement at the FOMC table for the need of at least another rate cut this year.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.