HIGHLIGHTS OF THE WEEK

- After some optimism early in the week, financial market sentiment soured as focus shifted back to fears of an escalation in trade tensions, Brexit uncertainty, and a potential economic downturn in 2019.

- The U.S. consumer remained unbowed in November, with consumer spending now tracking above 3% annualized in Q4. Inflation has cooled in line with oil prices, which should help to support real spending going forward.

- The FOMC makes its final decision of 2019 next week, and a hike is universally expected. We will be watching closely to see how members’ views have changed about how many hikes will ultimately be required in this cycle.

U.S. – “Bah! Humbug!”

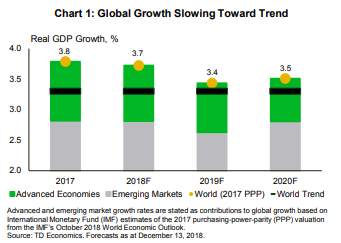

Our latest outlook did feature a small downgrade to global growth (Chart 1). However, the selloff in global risk assets in the fourth quarter has been outsized relative to the magnitude of the economic slowdown. The selloff likely reflects the build-up of unresolved global risks, coupled with a delayed adjustment in growth expectations from lofty levels. Taking a step back from the downturn in equity markets, there are few signs that the economic expansion is nearing an end, other than the fact that the expansion is approaching the longest on record. One worry is that negative sentiment can become self-fulfilling (see our Perspective). We remain vigilant in monitoring signals of an impending downturn, such as yield curves, business confidence, risk-assets, and labor market conditions.

The consumer is in pretty good shape. The job market is strong and inflation is contained. Economy-wide growth in wages and salaries has averaged roughly 4% over the past six months. And, headline inflation has cooled in line with lower oil prices. CPI inflation was at 2.2% year-on-year in November’s data. Our forecast is for inflation to remain around that level through 2019. That sets the consumer up for some decent real income gains. Therefore, we expect consumer spending to slow only modestly in 2019, as the windfall from tax cuts fades, but still running at a very healthy 2-2 ½% clip in real terms.

Overall, the U.S. economy is strong, and the Federal Reserve is well justified in raising rates another quarter point at its meeting next Wednesday. The real question is how the FOMC’s views have changed about how much further rates need to rise. Given the fairly benign inflation backdrop recently, we expect the Fed to hike rates more gradually in 2019.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.