HIGHLIGHTS OF THE WEEK

- Data released this week remains consistent with the view that U.S. economy continues to expand at an above-trend pace.

- Although disappointing in terms of the headline, job gains were also consistent with an economy running near capacity. Furthermore, wage growth held at a healthy pace in November.

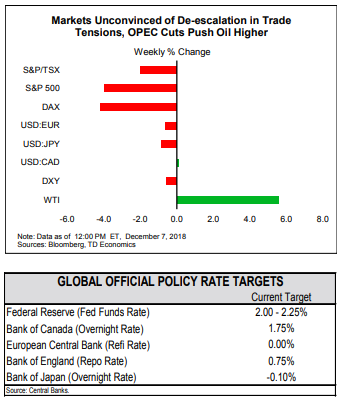

- An agreement between the U.S. and China to delay an escalation of tariffs until April failed to convince financial markets that trade tensions are easing.

Markets Gyrate on U.S.-China Trade Headlines

Manufacturing and non-manufacturing activity picked up a bit in November, but is still off the highs recorded earlier this year. Firms continue to report capacity constraints, including labor and component shortages. Import tariffs remain a key concern. Similar worries were echoed in the Fed’s latest beige book report. Respondents to the Fed’s survey for the month of November indicated that labor shortages were being felt across a broad range of industries, and that tight labor markets were preventing them from getting the workers that they needed. In addition, rising costs, although offset in part by the falling price of oil, were impacting margins and leading firms to raise prices to offset them.

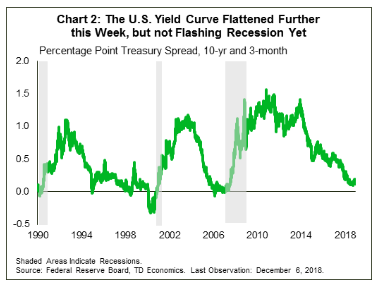

Strong fundamentals, however, are providing little comfort to financial markets. News headlines about slowing foreign demand growth, ongoing trade tensions, and Brexit have driven equity market volatility up, and prices down in the past couple of months. Fear lit a bid for bonds this week, with the U.S. 10-yr yield falling below 2.9% – its lowest level since early September. Although a flattening yield curve typically forebodes an increased chance of recession in the quarters ahead, there is little in the way of corroborating evidence (Chart 2). Instead, the recent move is likely a reflection of near-term concerns about temporary weakness in inflation and trade risks, rather than a deterioration in economic fundamentals.

Undoubtedly, an easing of trade tensions would be a welcome development. The G20 summit proved somewhat constructive as it produced a 90-day break from an escalation in import tariffs between the U.S. and China. But, news of the arrest of Huawei’s CFO later in the week revealed how fraught the relationship is currently between the U.S. and China. Tariffs appear to be just the first step in planned engagement with China on a set of deeper issues that need to be addressed.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.