Financial News Highlights

- The Federal Reserve opted to hold rates steady in their first decision of the year in order to give themselves more time to assess the sustainability of current disinflation trends in financial news.

- Employment gains in January nearly doubled expectations as strong upward revisions to December carried forward into 2024.

- U.S. Treasury markets experienced volatility this week as a decline in yields prompted by a dovish interpretation of Wednesday’s Federal Reserve decision was reversed by stronger than expected employment data on Friday.

Resilient Labor Demand and A Patient Fed

January ended with a big week for economic data, including the first Federal Reserve decision of the year and the first employment data reading in financial news. While the Fed’s statement dropped any tightening bias, Chair Powell’s press conference curtailed market hopes for a near-term pivot to less restrictive monetary policy. This saw Treasury yields fall steeply after the meeting. However, this descent was ultimately short-lived, as much stronger than expected employment data on Friday sent yields higher. At time of writing, the ten-year Treasury yield was 12 basis-points lower on the week.

January ended with a big week for economic data, including the first Federal Reserve decision of the year and the first employment data reading in financial news. While the Fed’s statement dropped any tightening bias, Chair Powell’s press conference curtailed market hopes for a near-term pivot to less restrictive monetary policy. This saw Treasury yields fall steeply after the meeting. However, this descent was ultimately short-lived, as much stronger than expected employment data on Friday sent yields higher. At time of writing, the ten-year Treasury yield was 12 basis-points lower on the week.

Overall, the messaging from the Federal Reserve on Wednesday was positive. Chair Powell stated that the committee was pleased by the progress made thus far on returning inflation to their 2% target, but noted that they would require more time to assess the sustainability of current disinflation trends (Chart 1). With economic growth accelerating last year on the back of strong consumption growth, the labor market remaining solid, and geopolitical tensions posing challenges to supply chains (and hence inflation), caution is likely wise. Chair Powell also stated that he viewed it as unlikely that the FOMC would possess the confidence to reduce interest rates by the March meeting in six week’s time.

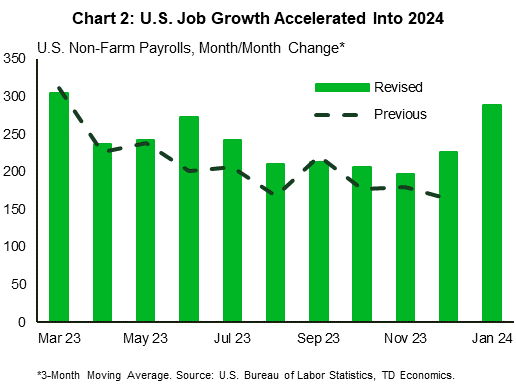

Powell’s caution was further validated when we received the January employment data on Friday. Not only did we see a very strong 353k jobs added in the first month of the year, but last year’s total job gains were also revised up to 3.1 million, well above the prior reading for 2.7 million, with much of the revised strength coming through the second half of the year (Chart 2). Furthermore, wage growth appears to be accelerating, with the three-month annualized change in average hourly wages rising to a twenty-month high in January. Although near-term strength in the labor market is expected to recede over the coming months, sustained imbalances in the labor market is a risk that the Fed is acutely aware of.

Elsewhere this week, the ISM Manufacturing Purchasing Managers’ Index (PMI) showed that industrial activity continued to contract in January, but by less than expected. Elevated interest rates continue to weigh on the sector, but demand has begun to show signs of improvement, which has stabilized aggregate production output. Forward pricing in financial markets for the eventual decline in interest rates expected this year will likely provide relief to the manufacturing sector moving forward as the demand for goods improves.

Elsewhere this week, the ISM Manufacturing Purchasing Managers’ Index (PMI) showed that industrial activity continued to contract in January, but by less than expected. Elevated interest rates continue to weigh on the sector, but demand has begun to show signs of improvement, which has stabilized aggregate production output. Forward pricing in financial markets for the eventual decline in interest rates expected this year will likely provide relief to the manufacturing sector moving forward as the demand for goods improves.

The lingering question, however, is when will the Federal Reserve begin to drawdown interest rates? Markets have broadly abandoned their hopes for a March cut after this week, with May now being the expected timeline with about 80% probability as of the time of writing. Upcoming data will likely provide greater clarity on the timing of the introduction of less restrictive monetary policy, including a 60 Minutes interview with Chair Powell on Sunday and the Federal Reserve Senior Loan Officer Opinion Survey on Monday.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.