Financial News Highlights

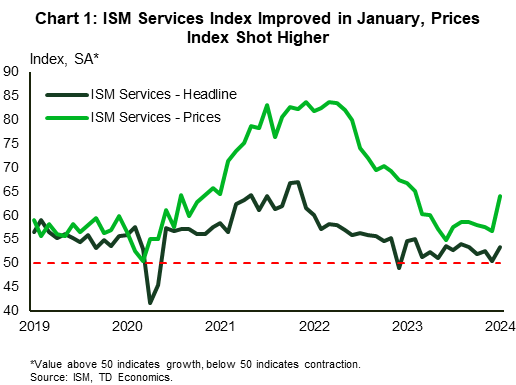

- The ISM Services index, which was on the cusp of falling into contractionary territory in December, improved notably in January, rising 2.9 points to 53.4 in financial news. The one blemish to the report was a sharp move up in the prices index.

- With little on the data front, a series of Fed speeches took center stage this week. The key message was that with the economy remaining on decent footing, the Fed could afford to show patience on rate cuts. This didn’t interrupt the uptrend in equity markets, with the S&P 500 reaching a new milestone – the 500 mark.

Fed Officials Continue to Signal Patience on Rate Cuts

Recent economic reports focusing on GDP and employment growth have driven home the point that the U.S. economy remains on solid footing. This week’s limited data provided further support to this view. In this vein, several Fed officials this week reiterated their message that there’s no rush to cut interest rates, with bond yields trending moderately higher as a result. In what appeared to be a return of ‘good news being good news again’, stock markets shrugged off the prospect of interest rates remaining higher for longer and continued to trek higher, with the S&P 500 reaching another milestone by hitting the 5000 mark.

Recent economic reports focusing on GDP and employment growth have driven home the point that the U.S. economy remains on solid footing. This week’s limited data provided further support to this view. In this vein, several Fed officials this week reiterated their message that there’s no rush to cut interest rates, with bond yields trending moderately higher as a result. In what appeared to be a return of ‘good news being good news again’, stock markets shrugged off the prospect of interest rates remaining higher for longer and continued to trek higher, with the S&P 500 reaching another milestone by hitting the 5000 mark.

The ISM Services index, which was on the cusp of falling into contractionary territory in December, moved up notably in January, rising close to three points to 53.4. Looking under the hood, gains in three of the four main subcomponents helped lift the index higher. Of note, the employment sub-component flipped to signaling growth, as it jumped 6.7 points to 50.5. The one blemish to the report, was the fact that the prices index shot higher in January (Chart 1). A month of data does not make a trend, but the increase could signal additional inflationary pressure ahead.

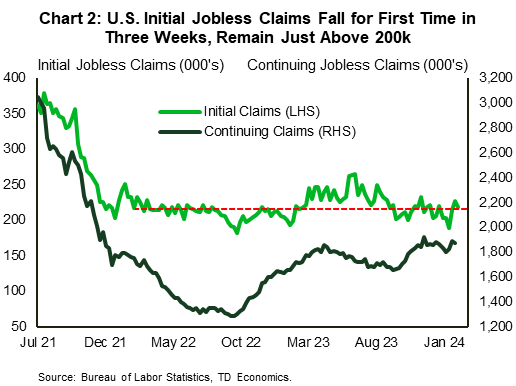

Weekly jobless claims data were consistent with a healthy labor market. Initial and continuing jobless claims continued to head lower (Chart 2). While several companies have announced plans to trim headcount this year, this is not yet being reflected in labor market data, suggesting that other businesses are growing.

With very little in the way of primary data releases, speeches from several Fed presidents and other Fed officials took center stage this week. Overall, the messaging was similar: the Fed needs to see further improvement on inflation, and with the economy on solid footing it can afford to be patient about the timing of rate cuts in financial news. Their remarks largely echoed those made by Fed Chair Powell on Sunday. Besides reiterating his message that the Fed is wary of cutting rates too soon, Powell covered a lot of ground in the ‘60 Minutes’ interview. Two comments a bit peripheral to monetary policy stood out. The first was on commercial real estate (CRE), where Powell characterized the risks as a ‘manageable’ problem for larger banks and alluded to the low probability of a repeat of the events that unfolded during the Global Financial Crisis. However, he did note that some smaller banks that have large exposures to CRE may ‘close or be merged out’.

With very little in the way of primary data releases, speeches from several Fed presidents and other Fed officials took center stage this week. Overall, the messaging was similar: the Fed needs to see further improvement on inflation, and with the economy on solid footing it can afford to be patient about the timing of rate cuts in financial news. Their remarks largely echoed those made by Fed Chair Powell on Sunday. Besides reiterating his message that the Fed is wary of cutting rates too soon, Powell covered a lot of ground in the ‘60 Minutes’ interview. Two comments a bit peripheral to monetary policy stood out. The first was on commercial real estate (CRE), where Powell characterized the risks as a ‘manageable’ problem for larger banks and alluded to the low probability of a repeat of the events that unfolded during the Global Financial Crisis. However, he did note that some smaller banks that have large exposures to CRE may ‘close or be merged out’.

The other comment from Powell that stood out was his assertion that the U.S. is on an “unsustainable” fiscal path, with debt growing faster than the economy in the long run. To this end, the Congressional Budget Office (CBO) released new 10-year projections this week, which showed that the ratio of federal publicly held debt to GDP will rise from 97.3% last year to record high of 116% by 2034.

Looking ahead to next week, January’s inflation report will take center stage. The BLS released revisions to CPI data this morning, which were relatively minor and left the year-on-year path for inflation broadly unchanged. As for January, the market consensus expects a further moderation in the core measure.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.