Financial News Highlights

- U.S. inflation rose more than anticipated to start the year, on a Consumer Price Index basis, largely due to greater price pressures within the services sector in financial news.

- However, retail spending surprised to the downside in January, suggesting that consumer spending may be less vigorous than the stunning pace of last year.

- A slowdown in housing starts and less optimistic small businesses also suggest that economic momentum may be cooling.

Inflation Progress Stalls and Spending Falls in January

This week saw some key data releases to help gauge the state of the U.S. economy at the start of 2024, and the likely timing of a Fed rate cut. Among them were the CPI inflation and retail sales reports for January. While inflation was higher than expected, retail spending came in notably lower. Markets reacted strongly to the inflation data with stocks falling sharply and treasury yields rising.

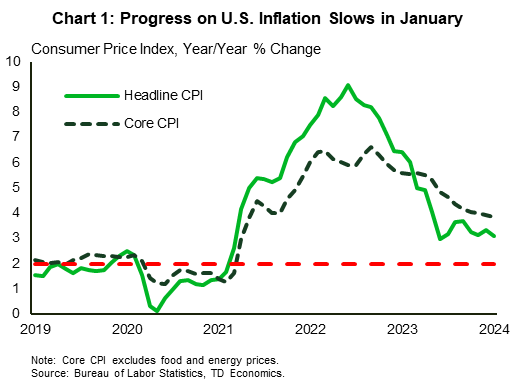

Taking a closer looker at CPI, the headline figure came in at 3.1% year-on-year (Chart 1). While this was lower than December’s 3.4%, it was higher than market expectations for 2.9%. The core measure matched December’s pace at 3.9%, but again was higher than expectations (3.7%) in financial news. The near-term movements showed that progress on the disinflation front stalled a bit, largely due to services. Both monthly headline and core inflation accelerated relative to December. Also, both the 3-month and 6-month annualized growth for core CPI accelerated, suggesting that the process to tame inflation is likely to progress in uneven spurts. The producer price index corroborated the stalled CPI signal, with the PPI rising by 0.3% m/m in January (markets expected 0.1%) relative to -0.1% in December.

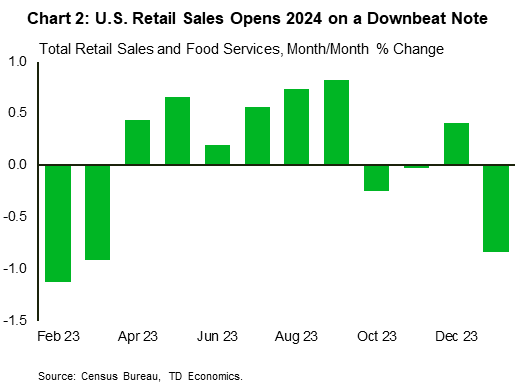

Turning to retail spending, consumers were a lot less jolly coming off the holiday season. Retail sales declined by 0.8% m/m in January (Chart 2). The sizeable decline was much larger than market expectations, however severe winter weather during January likely played a part in keeping consumers on the sidelines. Technical aspects of how the seasonally adjusted data is calculated may also have contributed to the relatively large decline. Nonetheless, the pullback suggests that consumer spending may be less of tailwind to U.S. economic resilience than it was last year.

Signals from the small business sector also suggest that economic activity might be slower in 2024. The NFIB’s small business optimism index declined to 89.9 from 91.1 in December, marking the biggest monthly decline since late-2022. On balance, small firms were generally less upbeat about their economic prospects, with the net percent of firms anticipating a better economy falling by 2 points. Given the higher exposure of small businesses to domestic economic conditions compared to larger firms, their downbeat mood points to headwinds ahead for the economy.

On the housing front, starts also disappointed expectations falling 14.8% to a five-month low (1.33 million) in January. The decline was in both the single and multi-family segments. Permits for future construction also fell on the month, implying that recovery in the housing market will be slow as buyers await lower mortgage rates.

Overall, data for January largely came in below expectations. This has left many market participants wondering what it all means for the timing of rate cuts. FOMC members have repeatedly stated that they need to see steady evidence that inflation is on a consistent path back to 2%. While the CPI and PPI data suggest that progress may be slow going for a bit, the pullback in other indicators point to an economy that is cooling. As such, Fed members may soon have the evidence that they need to begin the cutting cycle – it may just be later than markets desire.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.