Financial News Highlights

- U.S. inflation rose more than anticipated to start the year, on a Consumer Price Index basis, largely due to greater price pressures within the services sector in financial news.

- However, retail spending surprised to the downside in January, suggesting that consumer spending may be less vigorous than the stunning pace of last year.

- A slowdown in housing starts and less optimistic small businesses also suggest that economic momentum may be cooling.

Slow Your Roll

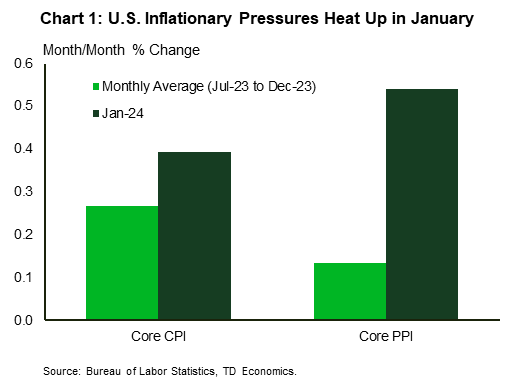

Slow your roll. That was the messaging communicated in the Federal Reserve’s meeting minutes released earlier this week. In hindsight, Fed officials had every reason to remain cautious in timing the pivot to policy easing. Since the January 30th-31st FOMC meeting, the economic data has done little to instill further confidence that inflationary pressures will continue to recede over the coming months. Not only did the January employment report come in more than double expectations, but a few inflation indicators (including CPI, PPI, and ISM price sub-indices) all came in much hotter-than-expected in January (Chart 1).

Slow your roll. That was the messaging communicated in the Federal Reserve’s meeting minutes released earlier this week. In hindsight, Fed officials had every reason to remain cautious in timing the pivot to policy easing. Since the January 30th-31st FOMC meeting, the economic data has done little to instill further confidence that inflationary pressures will continue to recede over the coming months. Not only did the January employment report come in more than double expectations, but a few inflation indicators (including CPI, PPI, and ISM price sub-indices) all came in much hotter-than-expected in January (Chart 1).

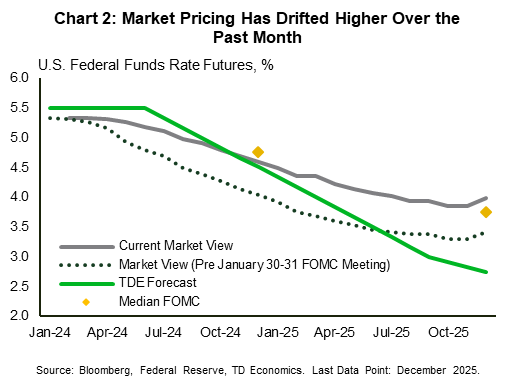

Market pricing has adjusted accordingly in recent weeks, with investors now positioned for a June rate cut and 100 basis points (bps) of policy easing by year-end – a trajectory that more closely aligns to both the FOMC’s and our own forecast (Chart 2).

While Fed officials acknowledged that inflation and employment risks are coming back into better balance, the minutes revealed that most participants remain concerned about the risk of “moving too quickly to ease the stance of policy”. Moreover, some officials cited the risk that stronger aggregate demand or a slow-down in the supply-side recovery could impede further progress on the inflation front. All of this argues for a more agile, data dependent approach to reducing the policy rate.

This is especially true given the recent growth dynamics. Economic growth remained incredibly resilient through the second half of last year – averaging an impressive 4% (annualized) or more than double its long-run potential. While first-quarter momentum looks to have lost a step, it’s still tracking a relatively robust 2-2.5%. As highlighted in our Quarterly Q&A publication released earlier this week, our current forecast assumes economic momentum will continue to soften as the year progresses. However, this is largely predicated on a further cooling in the labor market, resulting in slower income growth and weaker consumer spending. Should the labor market prove more resilient, then there’s an obvious upside risk to both spending and near-term inflation dynamics.

Next week we’ll get a pulse check on consumer spending and income trends for January. Accompanying the release will be the core PCE inflation data, which is likely to show an increase of 0.4% month-on-month – the strongest monthly gain in a year. It remains to be seen if January’s acceleration is a one-off, perhaps influenced by businesses increasing prices at the start of the year in a way that may not be fully captured by seasonal adjustment factors, or whether it’s the beginning of something more insidious. Either way, the recent uptick in inflationary pressures serves as a reminder that the descent back to 2% will likely come with some turbulence.

Next week we’ll get a pulse check on consumer spending and income trends for January. Accompanying the release will be the core PCE inflation data, which is likely to show an increase of 0.4% month-on-month – the strongest monthly gain in a year. It remains to be seen if January’s acceleration is a one-off, perhaps influenced by businesses increasing prices at the start of the year in a way that may not be fully captured by seasonal adjustment factors, or whether it’s the beginning of something more insidious. Either way, the recent uptick in inflationary pressures serves as a reminder that the descent back to 2% will likely come with some turbulence.

This is exactly why Fed Governors have been preaching patience over the past few weeks. Perhaps no one said it better than Christopher Waller, who noted “the strength of economy and the recent data on inflation mean it is appropriate to be patient, careful, methodical, deliberate – pick your favorite synonym”. “Whatever word you pick, they all translate to one idea: What’s the rush?”.

Thomas Feltmate, Director & Senior Economist | 416- 944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.