Financial News Highlights

- January’s personal and income spending report landed just where it was expected to, with the only surprise coming from a bigger than expected lift from nominal personal income growth in financial news.

- The Fed’s preferred measure of inflation, core personal consumption expenditure prices, cooled to 2.8% year-on-year, with near-term trends suggesting it has room to fall.

- A weaker-than-expected ISM manufacturing report helped support the notion that demand is cooling.

Coming Off the Boil?

January’s personal and income spending report landed just where it was expected to, with the only surprise coming from a bigger lift from nominal personal income growth in financial news. The as-expected print comes on the heels of updated GDP data that showed consumer spending closed out last year at an even better pace than originally thought. Most importantly, an upside inflation surprise was averted in January, allowing markets to let out a sigh of relief. After the data release Treasury yields tumbled and equities rallied. The data showed that price pressures continue to cool off. However, for a cautious Fed more progress will have to be made, leaving the first policy rate cuts a ways away.

January’s personal and income spending report landed just where it was expected to, with the only surprise coming from a bigger lift from nominal personal income growth in financial news. The as-expected print comes on the heels of updated GDP data that showed consumer spending closed out last year at an even better pace than originally thought. Most importantly, an upside inflation surprise was averted in January, allowing markets to let out a sigh of relief. After the data release Treasury yields tumbled and equities rallied. The data showed that price pressures continue to cool off. However, for a cautious Fed more progress will have to be made, leaving the first policy rate cuts a ways away.

First and foremost, this week’s personal income and spending report showed real personal consumption expenditures (PCE) pulled back 0.1% in January after healthy gains in November and December. Not a big surprise after January’s retail sales report showed a significant pullback. With some weather related factors weighing on demand it’s likely that this was more of a one-off than a new trend and February will likely show some bounce back.

Stronger-than- expected growth in personal income was largely a result of a larger cost of living adjustment in social security payments (and other government transfers), and the inflation adjusted real personal disposable income (PDI) measure showed no growth. Looking forward, this is what we’re interested in, as the downbeat month shaved two percentage points off of annual real PDI growth, bringing it down to 2.1% year-on-year. A deceleration in total real income growth is going to be part of the formula that cools the relentless consumer demand we’ve seen from the U.S. since the pandemic.

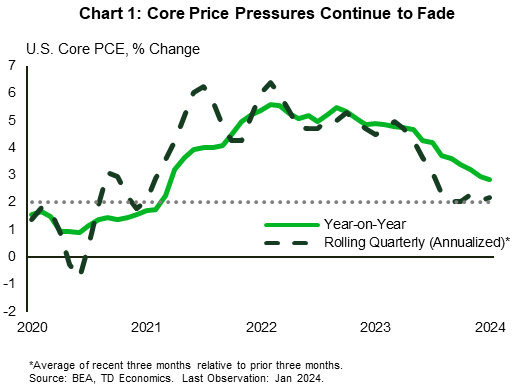

Of course, the Fed isn’t after just slowing the economy, but bringing demand and supply into better balance to tame inflation. On this front, yesterday’s report brought welcome news. The Fed’s preferred measure of inflation (core PCE) cooled to 2.8% year-on-year. Yes, still above the Fed’s target, but this is owing to base-effects from last year. Take a closer look at any near-term metrics and inflation is looking a lot closer to target. The three-month and six-month rates are at 2.6% and 2.5% (annualized), respectively. Smooth out some of the month-to-month noise in the series by taking a rolling quarterly rate of change, and core PCE prices have been advancing between 2% and 2.3% (annualized) since last September (Chart 1).

Of course, the Fed isn’t after just slowing the economy, but bringing demand and supply into better balance to tame inflation. On this front, yesterday’s report brought welcome news. The Fed’s preferred measure of inflation (core PCE) cooled to 2.8% year-on-year. Yes, still above the Fed’s target, but this is owing to base-effects from last year. Take a closer look at any near-term metrics and inflation is looking a lot closer to target. The three-month and six-month rates are at 2.6% and 2.5% (annualized), respectively. Smooth out some of the month-to-month noise in the series by taking a rolling quarterly rate of change, and core PCE prices have been advancing between 2% and 2.3% (annualized) since last September (Chart 1).

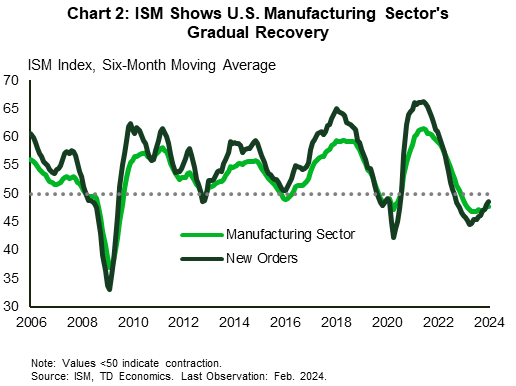

February’s ISM manufacturing report closed out the week, and supported the notion that demand is coming off a boil. With a 47.8 print for the month, the reading fell well short of market expectations and signaled that the recovery in the manufacturing sector is progressing rather slowly (Chart 2). Moreover, new manufacturing orders show that demand remains tepid.

For the Fed, these indicators come as signs that the relentless demand that powered the U.S. economy in late-2023 might be cooling off. Next Tuesday’s February ISM services report should shed light on the much larger services sector, while Fed Chair Jerome Powell’s testimony on Wednesday will hopefully give us a better sense of how the Fed is viewing these latest numbers.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.