Financial News Highlights

- The U.S. economy added 275k jobs in February, but job gains in the prior two months were revised down significantly and the unemployment rate ticked up to 3.9% in financial news.

- In his testimony before Congress this week, Federal Reserve Chair Powell noted that economic resilience gave the FOMC time to assess the sustainability of current disinflation trends.

- Congress is set to pass half of the federal spending bills for the 2024 fiscal year this week, five months and four continuing resolutions after the fiscal year began in October.

A Busy Week in Washington

With the first quarter entering its final weeks, we received a host of important economic data this week that will help form expectations for the year ahead in financial news. This included a labor market pulse check in addition to Federal Reserve Chair Powell’s semi-annual testimony before Congress. Equity markets continued to notch record highs, with the S&P 500 rising 0.8% on the week, while Treasury yields fell by roughly 10 basis-points as of the time of writing.

With the first quarter entering its final weeks, we received a host of important economic data this week that will help form expectations for the year ahead in financial news. This included a labor market pulse check in addition to Federal Reserve Chair Powell’s semi-annual testimony before Congress. Equity markets continued to notch record highs, with the S&P 500 rising 0.8% on the week, while Treasury yields fell by roughly 10 basis-points as of the time of writing.

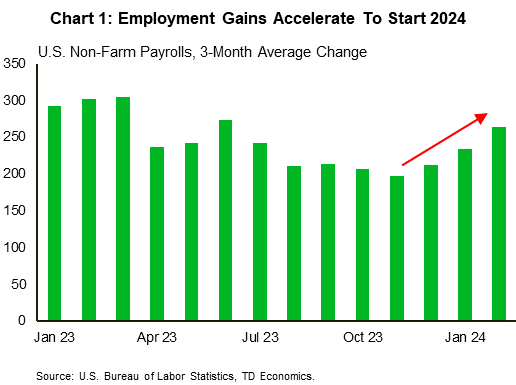

The headline release for this week was Friday’s employment report, which showed that 275k jobs had been added in February. While job gains in the prior two months were revised down by a considerable 167k jobs, the economy still saw solid and accelerating job growth moving into 2024 (Chart 1). However, the unemployment rate ticked up by 0.2 percentage-points to 3.9%, in part due to a return of positive labor force growth. On aggregate, the labor market remains healthy but is continuing to moderate towards a more balanced state. This will be welcome news for the Federal Reserve as they target their dual mandate of maximum sustainable employment and price stability.

The shift towards a more balanced risk outlook was also noted in Chair Powell’s testimony to Congressional committees this week. In his remarks he stated that the resilience of the economy and the labor market gave the FOMC time to assess the sustainability of current disinflation trends. While Powell did note that it would likely be necessary to implement less restrictive policy this year, he cautioned against the risk of easing pre-maturely. Solid job growth and an economy that continues to exhibit above-trend growth support Chair Powell’s assessment and our expectation that the FOMC will hold off until July to begin lowering interest rates.

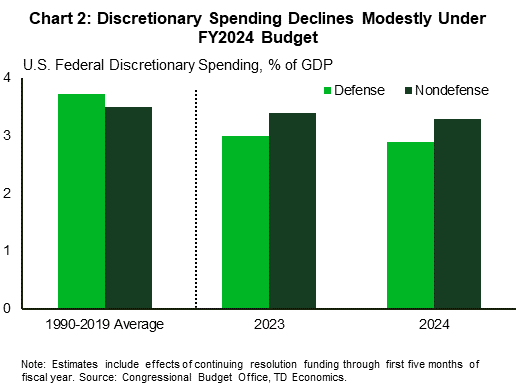

Also on Capitol Hill this week, Congress passed half of the federal spending bills for fiscal year 2024. With funding for six federal departments set to expire on Friday – legislated by the fourth continuing resolution of this cycle passed last week – the House passed a package of appropriation bills on Wednesday for the departments subject to the deadline. Senate approval and the President’s signature is expected ahead of the midnight deadline on Friday. The other six appropriations bills will need to be passed ahead of their March 22nd deadline, but aggregate spending levels are expected to be consistent with the limits previously agreed to by Congress (Chart 2). Removing the near-term risk of a government shutdown is undoubtedly positive, but ongoing structural deficits leave the sustainability of the national debt a long-term risk, which was also noted by Chair Powell in Congress this week.

Also on Capitol Hill this week, Congress passed half of the federal spending bills for fiscal year 2024. With funding for six federal departments set to expire on Friday – legislated by the fourth continuing resolution of this cycle passed last week – the House passed a package of appropriation bills on Wednesday for the departments subject to the deadline. Senate approval and the President’s signature is expected ahead of the midnight deadline on Friday. The other six appropriations bills will need to be passed ahead of their March 22nd deadline, but aggregate spending levels are expected to be consistent with the limits previously agreed to by Congress (Chart 2). Removing the near-term risk of a government shutdown is undoubtedly positive, but ongoing structural deficits leave the sustainability of the national debt a long-term risk, which was also noted by Chair Powell in Congress this week.

In the near-term, markets will be closely watching the February CPI inflation data release next week, which is expected to show a deceleration from January’s unexpected uptick. Further progress on disinflation will be required before the Federal Reserve considers shifting its current policy stance.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.