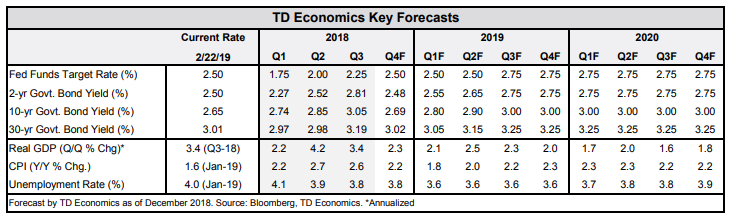

HIGHLIGHTS OF THE WEEK

- The barrage of negative U.S. data continued this week, with weakness in December durable goods orders and a decline in existing home sales in January.

- Still, markets were hopeful that progress would be made in the China-U.S. trade talks, which could help remove a cloud of uncertainty that has weighed on investment.

- The data affirms that the Fed made the right choice to shift off of gradual rate increases, and wait patiently to see if the U.S. economy remains resilient in the face of global weakness. We expect these signs to become clearer in the spring.

U.S. – Awaiting Signs of Spring

Overall durable goods orders rose 1.2% in December, but the underlying business-investment gauge – nondefense capital goods orders ex-aircraft – declined 0.7%, the fourth decline since August. Capex spending had already slowed in the third quarter of 2018 after a period of strength (Chart 1), and the durables data suggests a similarly modest pace in Q4. That lines up with our capital expenditure tracker, (based on Fed sentiment surveys) and points to more modest growth into early 2019 as well.

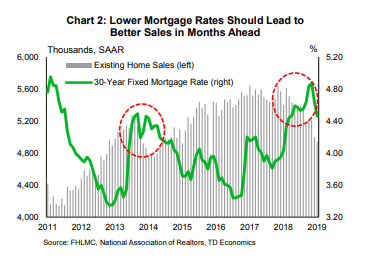

Deteriorating affordability has cut into housing demand over the past year, but mortgage rates have dropped about 60 basis points since late 2018, which should show up in improved sales in the months to come (Chart 2). Homebuilder confidence also improved in February, supporting a more positive housing narrative ahead.

Finally, on the data front, the delayed fourth quarter GDP report is released next week. We expect growth moderated to 2.2% in Q4, after running above 3 ½% through the middle of the year. With the government shutdown and the continued phenomenon of residual seasonality, the first quarter of 2019 is likely to be even weaker at 1.6%. For now, this lackluster data affirms that the Fed made the right choice to shift off of gradual rate increases, and wait patiently to see if the U.S. economy remains resilient in the face of global weakness. The minutes from the January FOMC meeting showed members debating whether further rate hikes will be necessary, but not contemplating cuts. Members continued to view sustained expansion strong labor market conditions, and inflation near 2% as the most likely path ahead. We too expect economic momentum to improve in the spring, and remain modestly above trend through the remainder of 2019. As long as there are no curve balls, the Fed is likely to raise rates once more in the latter half of the year.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.