HIGHLIGHTS OF THE WEEK

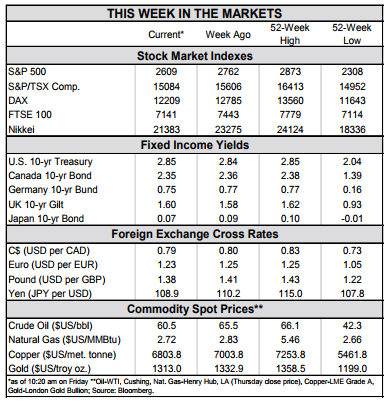

- Major U.S. stock indices entered correction territory on Thursday but remain elevated relative to where they were a year ago. The sell-off was spurred by fears of higher interest rates, as the 10-year government bond yield hit a four-year high.

- The $300 billion increase in the spending cap over two years, laid out in the federal budget deal, could add to inflationary pressures at a time when the economy is already operating at close to full capacity, pressuring yields up further.

- Next week, investors will turn their attention to hard data, with advanced January retail sales providing an indication of whether or not first quarter growth will be affected by the residual seasonality.

Stocks Correct but Fundamentals Remain Solid

What’s important to note is that this sell-off was not triggered by weak economic data either for the U.S. or global economy. Indeed, we learned this week that the ISM non-manufacturing index showed an improvement in the services sector at the start of 2018, with rising price pressures mirroring its manufacturing counterpart (Chart 1).

As market volatility surged, Fed speakers this week appeared unconcerned about financial market developments, instead choosing to reinforce their positive economic outlook. FOMC members had previously noted that equities were overvalued and therefore showed no sign of concern over the widespread sell-off. Voting members Dudley and Williams noted in speeches that wage inflation had picked up as expected and that markets are now adjusting to global monetary policy accommodation removal. This may help calm investor fears of faster rate hikes than previously expected, with the first of three hikes this year expected in March.

Next week, investors will turn their attention to hard data. Of particular interest will be advanced January retail sales data that should provide an indication of whether or not first quarter growth will be affected by the residual seasonality that has led to first quarter weakness in three of the previous four years. Although tax cuts have only started to boost pay checks in February, we anticipate that household spending has continued to be propped up by jobs and wage gains and will contribute strongly to economic activity again in the first quarter.

Katherine Judge, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.