FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- News of a trade truce between the U.S. and China buoyed equity markets at the start of the week. The ceasefire put additional tariffs on hold, and there were some modest concessions on both sides.

- On the economic front, messages were decidedly mixed this week. The ISM manufacturing and non-manufacturing indexes moved lower in June, while the payroll report showed a reacceleration in hiring with 224k jobs created last month.

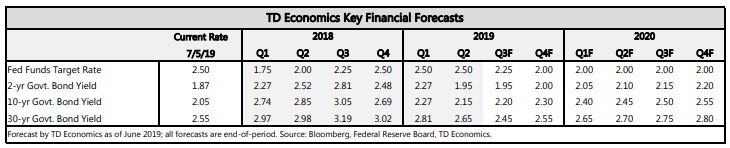

- Given the balance of risks, there is still a solid case for a 25- basis point “insurance” cut when the Fed meets later this month. But, insurance is likely to mean one or two rate cuts this year and not four or five as markets are pricing.

Markets Celebrate The U.S.-China Trade Truce

On the economic front, messages in this week’s data releases were decidedly mixed. The ISM manufacturing and non-manufacturing indexes moved lower in June and are significantly below year-ago levels. Still, both remain in expansionary territory, implying slower, but not negative economic growth (Chart 1). More concerning is that the greatest weakness was in the forward-looking indicators. The new orders subcomponent narrowly avoided contraction in June, while pending orders have already slipped below the 50-point threshold.

It is not surprising that activity is slowing from its 3%-plus, stimulus-fueled pace of a year ago, but it makes reading the economic tea leaves more difficult. It is hard to know in real time if the economy is returning to a healthy trend-like pace or pushing past it into a slump. Tariffs and trade uncertainty further cloud the mix, and signs globally point to a less benign slowdown.

The best evidence that the American economy is headed for a soft landing is the continued resilience in the labor market. That had been brought into question with the May payroll report (job growth slowed to just 72k), but doubts were assuaged with this week’s report showing a reacceleration to 224k in June. The only fly in the ointment was that there were no signs of faster wage growth. Instead average hourly wage growth remained unchanged at 3.1% for the third consecutive month.

Given the balance of risks, there is still a solid case for a 25- basis point “insurance” cut when the Fed meets later this month. But, as long as signs point to continued, albeit slower, economic growth, insurance is likely to mean one or two rate cuts and not four or five as financial markets are currently pricing. Fed speeches over the next two weeks will be key in communicating this to the public and financial market participants.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.