FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A light week on economic data was filled with Fed speeches and a trickle of news flow on the upcoming meeting between Presidents Trump and Xi. We do not expect to see a major breakthrough this weekend, but rather an agreement to continue talking (forestalling at least for now the threat of additional tariffs).

- Chair Powell reiterated comments in his press conference last week that crosscurrents to the economic outlook had arisen relatively swiftly over the past month, leading the Fed to shift toward an increased willingness to cut rates.

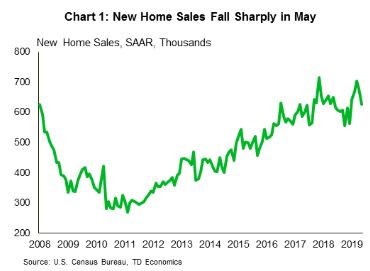

- Economic data was mixed, with home sales and confidence falling, but consumer spending rising. With revisions, second quarter personal consumption is likely to top 3% annualized, enough to push economic growth to the 2% mark.

Presidents Xi and Trump Meet As Crosscurrents Blow

Following the FOMC meeting last week, Fed speakers were out in full force explaining and defending the committee’s shift from patience to willingness to do more. Most notably, Chairman Powell reiterated that significant crosscurrents had hit the U.S. outlook in the period between the FOMC’s May and June decision. Among these, deteriorating business sentiment and slowing global growth rang the loudest.

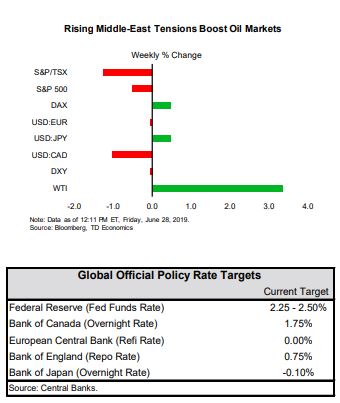

Powell did not mention it explicitly, but the breakdown in trade negotiations between China and the U.S. was a key driver of the change in tack. That puts the focus squarely on the leaders of the two countries as they meet in Japan this weekend. Prior to the meeting, optimism that the two sides were getting close to a deal were stoked by Treasury Secretary, Steve Mnuchin, who said they were 90% of the way there. But, just as soon as he said this, doubt was cast by President Trump’s own interview that dangled the possibility of additional tariffs. At the same time, reports that China would come to the meeting with preconditions of its own, including the removal of all existing tariffs and restrictions imposed on Huawei, reined in optimism that a significant breakthrough is imminent. All in all, we expect little to come out of the meeting except an agreement to keep on talking.

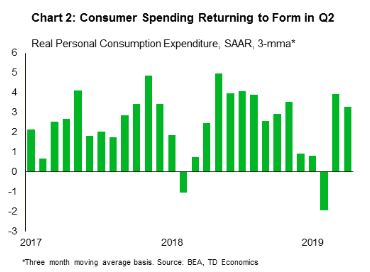

On the bright side, consumer spending is still holding up. Real personal consumption rose by 0.2% in May, and was revised up to 0.2% growth in April from a previously flat reading. With two of three months of the second quarter now recorded, spending growth looks to advance by well over 3% (annualized – Chart 2). Even with some weakness in investment and trade, second quarter economic growth appears likely to come in near the 2% mark.

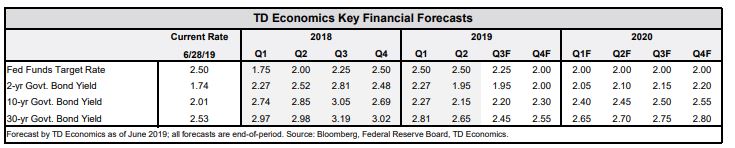

Evidence that economic growth is holding up suggests that even as the Fed considers insurance cuts, it need not have to bring out the bazooka. While a 25-basis point cut in July seems increasingly likely, the Fed should be able to afford to save at least some of its bullets and refrain from a larger 50-basis point cut, as futures markets have begun to price. Still, we would hold off betting the farm on it until after next week’s June payroll report.

James Marple, Senior Economist | 416-982-2557

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.