FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A potential trade war between U.S. and Mexico was averted, but global trade uncertainty remains.

- Despite markets pricing in rate cuts, domestic indicators suggest that the U.S. economy is on decent footing. Inflation remains stubbornly low, however.

- The Fed rate decision next week is clouded by conflicting signals, but we believe it will likely feature an easing bias.

Conflicting Signals Cloud Fed Rate Decision

This week was a perfect example of the conflicting signals faced by the economy. We began the week with a quick extinguishing of a possible trade war with Mexico, but trade uncertainty still looms large. Indeed, the trade conflict between the U.S. and China is not subsiding. Earlier this week, President Trump warned that if President Xi did not meet with him at the upcoming G20 summit, he would immediately slap 25% tariffs on the remaining un-tariffed $300 billion of Chinese imports.

Markets are pricing in the risks emanating from the trade conflicts, resulting in a continued inversion of the yield curve (3-month to 10-year), and an expectation of at least two Fed rate cuts by the end of the year.

However, trade uncertainty does not yet seem to be weighing on business optimism. The NFIB small businesses optimism index improved for the fourth consecutive month as businesses anticipated an improvement in economic conditions and more capital expenditure in months to come.

Moreover, U.S. consumers displayed their strength again, with solid retail sales growth in May alongside a significant upward revision to April data (Chart 1). Consumption growth may now exceed the 3% (annualized) mark in Q2.

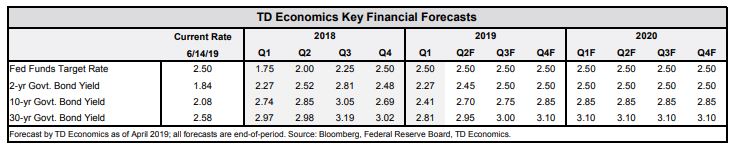

The Fed will no doubt take notice of the weakness in inflation in the FOMC meeting next week. But they will also have to consider all other developments as well. Despite rising downside risks, the domestic economy appears to be chugging along. All told, we expect the Fed to convey an easing bias, but not move on rates at next week’s meeting.

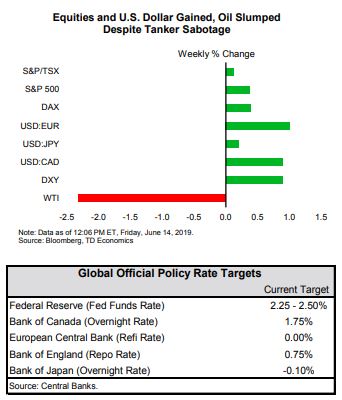

We also saw a rise in global political risks rise this week as two oil tankers were attacked in the Gulf of Oman. After falling through much of the week on the back of concerns about global growth, Brent oil prices jumped by around 5% on Thursday (with a similar move in the WTI contract), not quite enough to offset losses earlier in the week (Chart 2). With the relationship between the U.S. and Iran increasingly strained, oil markets may get caught in the middle.

Sri Thanabalasingam, Economist | 416-413-3117

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.