FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Trade tensions continued to dominate economic headlines, with U.S.-Mexico taking center stage. It remains unclear if a deal can be reached by Monday. The US-China spat also resurfaced, with signs that it is spreading beyond goods trade.

- Fed Chair Powell noted that the Fed was monitoring trade developments closely, and was ready to “act as appropriate to sustain the expansion”. This appeared to soothe equity markets, which rebounded to a three-week high.

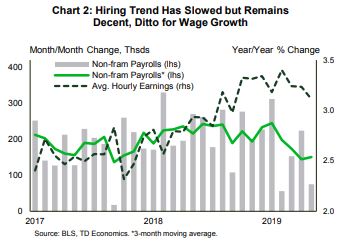

- The May jobs report disappointed expectations, with payrolls up only 75k. Looking through the recent volatility, the hiring trend has slowed but remains decent, averaging 151k in the last three months. The unemployment rate held steady at 3.6% and wage growth, while slowing a touch, held above 3% y/y.

Tariff Threats Muddy the Economic Waters

Trade tensions continued to dominate economic headlines this week, with the U.S.-Mexico quarrel taking center stage. Mexico sent a senior delegation to D.C. to try to address President Trump’s concerns regarding illegal migration, and to defuse the impending tariff threat. While some progress has been made, as at the time of writing, it is unclear if a deal can be reached by Monday’s deadline.

The uncertainty generated by these events has kept the Fed on high alert. Among several Fed speeches this week, Fed Chair Powell noted that the Fed was monitoring trade developments closely, and was ready to “act as appropriate to sustain the expansion.” Chair Powell’s emphasis on the Fed’s flexibility appeared to soothe equity markets, which rebounded to a three-week high.

With the broad economic backdrop still decent, trade and global growth remain the ultimate wildcard. Mexico is the second biggest source of goods entering the U.S. after China. As such, the impending 5% tariff will be problematic, particularly for products that cross the border multiple times (i.e. auto parts). Prospects for an increase in the tariff rate to 25% are more daunting, with supply chain disruptions, reduced market access and the hit to confidence all more acute. A simultaneous escalation in tensions with Mexico and China would accentuate these risks further. In the event that tensions escalate in this fashion, the Fed will have little choice but to act.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.