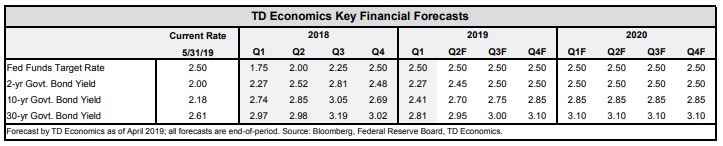

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S.-China trade tensions continued to dominate headlines as both countries dig in for another round of negotiations under more strained circumstances. U.S. tariffs against Mexico appear to also be in the works.

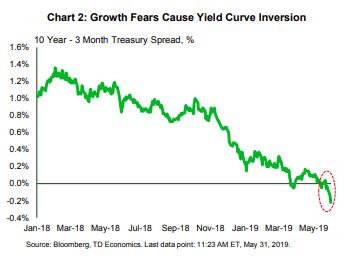

- As trade tensions flare, investors have run for cover, driving up bond prices and sending the yield curve into inversion territory.

- U.S. Q1 growth was revised marginally lower (3.1% vs. 3.2%), and Q2 is projected to be lower still (below 2%). Inflation however managed to edge marginally higher with core PCE at 1.6% year-on-year in April.

Trade Tensions Still in the Spotlight

In other trade news, just as the U.S. and Mexico took steps this week to ratify the USMCA, President Trump threatened to impose a 5% tariff on all Mexican imports starting July 10th. The President wants Mexico to do more to deter illegal migration from Central America. These tariffs, alongside prolonged Chinese negotiations, complicate trade relations even further. The heightened bout of uncertainty is likely to dent already shaky business confidence.

China has responded to U.S. rhetoric with both direct and indirect threats. The country suggested that they too may influence global supply chains through their dominance of “rare earth” exports – a group of 17 minerals used in the production of most modern electronic devices. A ban on exports to the U.S. could disrupt production and affect prices of many products ranging from smartphones to satellites. There are also indications that China may have once again halted purchases of U.S. soybeans after previously resuming purchases as a sign of goodwill during negotiations.

Meanwhile, on the domestic data front, home price appreciation continues to moderate. Data for March showed that home prices grew 3.7% year-on-year, lower than the 3.9% recorded in February (Chart 1). Price growth has been decelerating since April last year, suggesting that even with lower mortgage rates and rising wages, past price growth may have stretched affordability for many potential buyers.

With concerns of lower growth and heightened trade tensions, investors pushed the yield on 10-yr Treasury notes to the lowest close since September 2017 this week. This caused the yield curve to invert as it dipped below the three-month note (Chart 2). While inversions tend to precede recessions, the phenomenon would need to be sustained and observed among other maturities before the indicator signals an imminent risk and materially affect decisions at the Fed. All said, the reignited trade tensions have skewed the risks to both U.S. and global growth further to the downside – a development which will no doubt receive close monitoring by central bank officials.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.