HIGHLIGHTS OF THE WEEK

- Equity markets started off the week on a positive note. But the advance proved transitory as oil prices slid into bear territory, sending energy stocks and the main indices lower.

- With little in the way of economic data, Fed speeches took center stage. While echoing support for last week’s decision, some Fed speakers appeared to take on a more dovish tone, with Harker and Evans putting an emphasis on waiting for further proof to hike again.

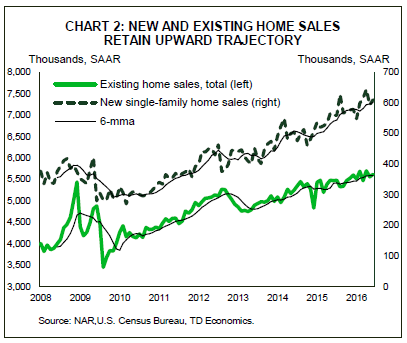

- The only significant economic data releases this week pertained to housing activity. Existing home sales surprised on the upside. Meanwhile,sales in the smaller and more volatile new home market, also rebounded in May.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

FED SPEECHES TAKE CENTER STAGE

Markets started off the week on a positive note. Tech stocks bounced back on Monday as industry leaders met with President Trump at the first gathering of the American Technology Council. Meanwhile, financials were buoyed by comments from FOMC voting member Dudley that didn’t seem too concerned with the slowdown in inflation. Sentiment was also supported by Macron’s majority-win of the French parliamentary elections.

Unfortunately, the advance proved transitory. Oil prices slid into bear territory on account of rising production among the U.S., Libya and Nigeria and doubts as to whether recent OPEC cuts would be sufficient to manage the supply glut. This sent energy stocks and the main indices lower and enabled a move toward safe heaven assets (Chart 1).

With little in the way of economic data, Fed speeches took center stage. Given that last week’s decision to hike was not unanimous and the fact that inflation has drifted lower, FOMC members appeared to be on the defensive. Vice-Chair Fischer pointed to “high and rising” home prices as one of the hazards of keeping rates low for long. While echoing support for last week’s decision, other Fed speakers appeared to take on a more dovish tone, with Harker and Evans putting an emphasis on waiting for further proof to hike again. Bullard (non-voter) suggested that the expectation for rates rise to 3% over the next two and a half years is “unnecessarily aggressive.”

Still, the Fed is sticking to its guns in expecting another rate hike by the end of this year, betting that the factors weighing on price growth will prove temporary and that a tight labor market will pull up wages and buoy inflation. They may also get some help from a lower U.S. dollar, which is well off its peak level set earlier this year and is on track to end lower again the week. A lower dollar should help put upward pressure on goods prices, which have been consistently negative over the past year.

Rising interest rates, combined with robust price growth on the bigger resale segment are expected weigh on affordability. Still, households are likely to withstand the incremental increases in borrowing costs thanks to a solid labor market that is poised to deliver continued job and income gains. An improvement in the homeownership rate is also expected to provide a gentle tailwind as outlined in our recent report, with resales expected to advance by 3.4% this year and 2.6% in 2018 to nearly 5.8 million by the end of the forecast horizon. Price growth should remain strong this year, holding near 6%. But a rebound in for-sale inventory, which is expected to be more of a factor next year, will help keep price growth in check at around 4% in 2018.

Admir Kolaj, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.