HIGHLIGHTS OF THE WEEK

- Bond markets sold off sharply this week on remarks from monetary policymakers. Bond yields rose by 20 to 25 basis points in Germany and the UK, respectively. Yields on Treasuries also rose, but markedly less as U.S. data has underwhelmed.

- Momentum in personal spending dissipated slightly from the strong performance in the previous two months. Gains in real income surprised to the upside, and should underpin spending going forward.

- We look forward to next week’s employment report as a potential market mover. We expect a relatively robust print of 170 thousand jobs and unemployment to hold steady at 4.3%.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

Hawkish Central Bank Rhetoric Rattles Markets

Global markets were volatile in recent days. Bond markets sold off sharply since mid-week on remarks from monetary policymakers. Central bankers in the Eurozone and the UK have indicated that meaningful economic improvements should begin to warrant the removal of accommodative monetary policy measures. This hawkish sentiment saw bond yields rise by 20 to 25 basis points in Germany and the UK, respectively. Yields on Treasuries also rose, but markedly less as U.S. data has underwhelmed. The relatively softer U.S. data also led the dollar lower vis-à-vis the euro and the pound.

The lower U.S. dollar also helped to shore up oil prices that have been led higher recently by curtailed production related to maintenance of Alaskan sites and a storm in the Gulf of Mexico. Still, US stockpiles have remained high this summer, with oil prices likely to remain relatively anchored during the rest of the year.

Expectations of less-stimulative policy going forward have also led stock markets to retrench as investors across the Atlantic readied themselves for what may be end an era of cheap money. At the same time, comments by Fed Chair Janet Yellen on Tuesday indicated that the Fed is keeping a close eye on stock markets valuations, injecting further caution into U.S. equity markets.

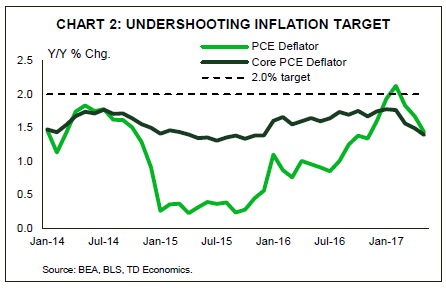

Still, the U.S. data came in relatively weak this week. While still supportive of growth in the second quarter, momentum in personal spending dissipated slightly from the strong performance in the previous two months. Gains in real income surprised to the upside, and should underpin spending going forward (Chart 1). But, this was partly related to the weakness in prices, which under-performed in May, corroborating anemic CPI growth on the month (Chart 2). There was also weakness in durable goods orders, which fell in May according to the advance estimate, suggesting weaker capital investment in the second quarter.

But, not all data were soft. Consumer confidence metrics rose according to both the Conference Board and University of Michigan surveys. Moreover, the goods trade balance narrowed slightly in May as automotive exports rebounded following two consecutive months of underperformance. With domestic US auto sales peaking last year, global demand will play an increasingly important role for growth in the sector. Exports should also get some support from a weaker greenback. We look forward to next week’s ISM manufacturing survey results to echo these positive developments, with readings poised to expand, mirroring upbeat regional surveys for June.

Katherine Judge, Economic Analyst

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.