FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- One year after the start of global lockdowns, it is starting to feel like the end is finally approaching. The new fiscal package signed into the law will continue to support a stronger economic recovery and the financial resilience of American households.

- The Consumer Price Index (CPI) came in on market expectations, while core CPI edged lower in February, giving inflation anxiety a short break.

- The 10-year U.S. Treasury yield is on the upward trend again, but the Fed’s primary concern remains a sustained labor recovery. With the virus still spreading, the recovery remains fragile and unequal, requiring policy to remain accommodative.

A Year of COVID

This week marks one year since the start of global lockdowns and economic disruptions due to the coronavirus pandemic. And while no one can say that the crisis is over, it is starting to feel like the end is finally approaching. Thanks to unprecedented policy support, the economic slump has been short-lived, and prospects for recovery look much brighter than initially predicted. We expect that the American Rescue Plan, signed into effect on Thursday, will lift economic growth to roughly 6% this year, the highest rate since 1984.

The new fiscal package is huge. It provides a fresh round of $1,400 checks starting as early as this weekend, extends unemployment benefits of $300 per week until September, increases the child tax credit (and makes it fully refundable), provides aid to states and local governments, supports schools and expands vaccination efforts.

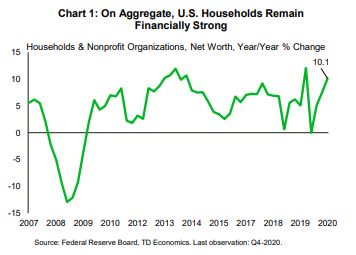

Substantial income supports have enabled Americans to maintain strong balance sheets through this crisis. According to the Fed’s data released yesterday, U.S. households’ and non -profit organizations’ net worth reached a record high of $130 trillion, growing 10% in the last quarter of 2020. (Chart 1). Nevertheless, income and wealth disparities, exacerbated by the crisis, continue to pose risks to the recovery.

On the economic front, data was scarce this week. A highly anticipated Consumer Price Index (CPI) report came in on market expectations. Gasoline and food prices continued to rise, driving the headline index 1.7% higher over the past year. Still, core inflation (excluding these volatile categories) remained soft, rising by 0.1% on the month and edging lower on the year-on-year basis to 1.3% from 1.4% in January.

Still, a closer look at the core prices reveals a shift in recent trends. Supported by the housing component of the index, the decline in core services prices was halted at 1.3% year-on-year (Chart 2) in February. Indeed, strong demand for housing has lifted home prices by at least 10% since 2019, even as rents in major urban centers have gone in the opposite direction. Goods’ price growth, on the other hand, softened in February reflecting a pull-back in used car prices, one of the biggest price outperformers of the pandemic.

The news of muted price growth gave the market’s inflation anxiety a short break. The 10-year U.S. Treasury yield subsided from its last week’s peak of 1.60% to just under 1.50%, before bouncing back to almost 1.62% at the time of writing. Despite solid demand in this weeks’ three U.S. Treasury auctions, investors are increasingly betting on higher inflation. As we wrote recently, the Fed will be mindful of mounting price pressures, but its new framework gives it more wiggle room for letting inflation move above 2%.

The Fed’s primary concern remains a sustained labor recovery. With the strongest economic growth in recent history, this should be achieved over the next two years. In the meantime, with the virus still spreading, the recovery remains fragile and unequal, requiring policy to remain accommodative.

Maria Solovieva, CFA, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.