FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Most Federal Open Market Committee members see no interest rate hikes until at least 2024 despite a sharp upgrade to the growth outlook.

- Retail sales weakened on the back of frigid temperatures, but additional support to households through the American Rescue Plan is likely to support retail activity in the coming months.

- Housing starts fell for the second straight month in February, but homebuilding activity is expected to remain elevated in the near-term.

Spring is Just Around the Corner

On the monetary policy front, the Federal Reserve sharply upgraded its growth outlook. The median projection among FOMC members is for the economy to expand 6.5% (from 4.2%) this year due to stimulus and vaccine rollout. Still, the Fed maintained its current monetary policy stance. This includes keeping the federal funds rate at the current 0% to 0.25% range and a commitment to purchase at least $80 billion Treasuries and $40 billion mortgage backed securities per month. The Fed’s projections also showed the majority of members do not expect to raise the federal funds rate until at least 2024.

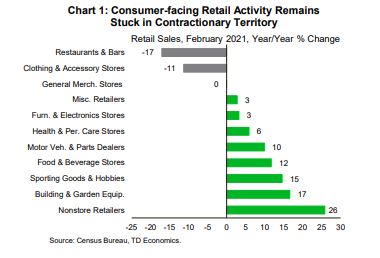

In terms of economic data, retail sales declined by 3.0% month-on-month in February (Chart 1). This was worse than the consensus estimate for a 0.5% drop. The decline comes on the back of unseasonably cold weather that shut down many of the southern states. It also comes on the heels of a strong and upwardly revised reading in January. The good news is that spring is just around the corner and optimism is growing. The timing of the $1.9 trillion American Rescue Plan couldn’t be any better. It comes at a time when cases are declining and lockdowns are being eased. This will make spending easier, allowing retail sales to recover in the coming months.

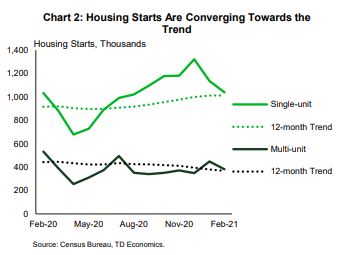

Turning to the real estate sector, housing starts fell by around 10% in February, declining for the second straight month (Chart 2). Housing starts dropped to 1.42 million units (annualized) from 1.58 million in the previous month. The fall in housing starts and building permits was seen across both single-family and multi-family segments. The decline was also seen across most regions but was concentrated in the Northeast, which saw a staggering 40% drop. Despite the slow start to the new year, we expect homebuilding activity to remain elevated near current levels. This is thanks to a low inventory environment and the fact that housing demand will improve as the labor market heals.

Meanwhile, new COVID-19 cases continue to fall. And the vaccine rollout is only getting faster. So far more than a 115 million doses have been administered, a 14% increase compared to last week. States are easing restrictions and air travel is picking up. There is plenty of reason to be optimistic, but states need to tread carefully. As long as the virus is still with us, reopening economies too quickly could still lead to a surge in cases.

Sohaib Shahid, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.