HIGHLIGHTS OF THE WEEK

- The Fed carried out its well-telegraphed rate hike this week. Despite the Fed’s hawkish messaging in advance of the decision, its expectations for rate increases were unchanged, leading bond yields to dip.

- The Fed edged up its economic forecast for 2018, as did TD Economics in our latest forecast, released this week.

- Overseas, one populist threat to the Eurozone was vanquished this week as the populist right-wing party lost the Dutch election. However, the UK is days away from triggering the two-year Brexit negotiation process with the EU, so the risk of euro-driven market volatility remains.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

THE FED TAKES ANOTHER STEP ON THE RATE HIKE TIGHTROPE

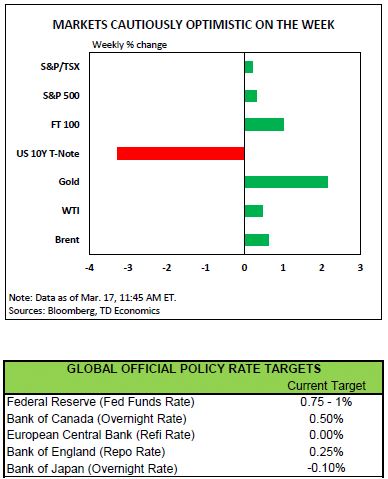

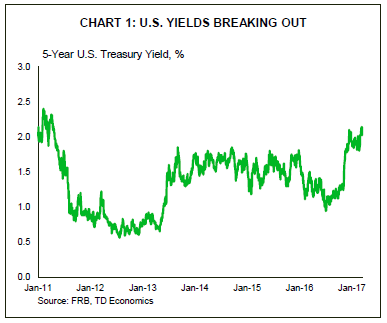

Markets were cautiously optimistic this week as the Fed carried out its well-telegraphed rate hike, and one populist threat to the euro zone was vanquished in the Dutch election. The Fed hiked the funds rate 25 basis points, to a range between 0.75% and 1.0%. Bonds rallied in the wake of the decision, since the hawkish rhetoric leading up to the decision was not born out in a more aggressive pace of rate hikes in the Fed’s “dot” plot. The Fed continues to expect to raise rates three times in total in 2017, unchanged from its December forecast. Even with a dip downwards in yields this week, the 5-Year Treasury yield remains close to a six-year high (see Chart).

During the press conference, Yellen characterized the economy as “progressing nicely”, and that the Fed views three hikes per year as a “gradual” pace in the current environment. While the median interest rate projection remained unchanged, the number of dots at the median rose (from six to nine). The Fed’s economic projections told a similar story, edging up by 0.1 percentage point its outlook for core inflation in 2017 and its outlook for economic growth in 2018. In other words, FOMC members are a bit more confident, but no more hawkish, than they were in December.

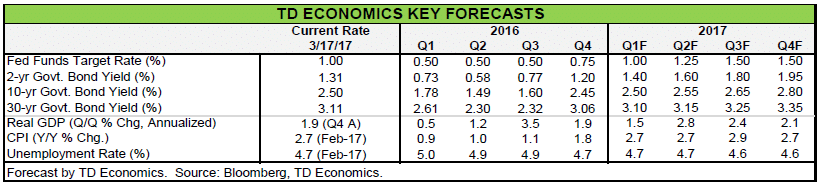

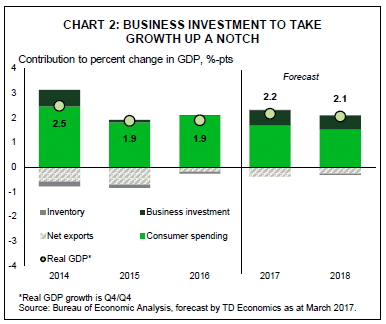

The Fed was not alone in nudging up its forecast. In our latest economic forecast released this week, we also bumped up our forecast for growth in 2018. The upgrade is largely owing to a more optimistic forecast for domestic demand, and business investment in particular. Measures of business sentiment have largely held on to their post-election jumps, and we expect that optimism will translate into increased spending over the next two years. Particularly now that the weakness in corporate profits appears to have turned around, and the worst is over in the oil patch.

As always, there are upside and downside risks to the outlook. The most notable upside risk stems from fiscal policy. We continue to believe it is too early to include any potential boost from the kinds of tax cuts or infrastructure spending that was promised during the campaign. As evidenced by the current debate on healthcare reform, it is going to take time for Republican members of Congress and the White House to reach an acceptable compromise on these key policy priorities. Therefore, we expect any fiscal boost to be a factor in the 2018 outlook and beyond, not this year.

Like the Fed, we also expect a gradual pace of rate hikes this year. Downside risks to the forecast have not entirely vanished. Concerns stemming from political uncertainty in Europe did clear one hurdle this week with the Dutch election result. But, France’s Presidential elections loom (on April 23rd and May 7), and the UK is on the cusp of triggering two years of Brexit negotiations with the EU. The potential for euro-driven market volatility to disturb markets’ current placid optimism is real. And on this side of the pond, the risk that the Trump administration moves from rhetoric to real protectionist measures on trade also looms.

Taking a step back to the here and now, the U.S. economy is doing well. The Fed must now walk a tightrope balancing the need to remove monetary stimulus against the risk of taking rates too high, which would dampen domestic growth too much or trigger risks abroad.

Leslie Preston, SeniorEconomist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.