HIGHLIGHTS OF THE WEEK

- Markets continued to price in lofty odds for a Fed hike next week, putting further upward pressure on the 2 year treasury yield – which remained near a nine-year high. The U.S. dollar also remained relatively well supported up 0.2% on the week. Meanwhile, equity markets took somewhat of a breather, but the S&P500 only ended the week 0.5% lower.

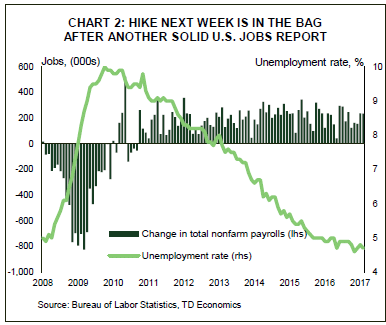

- There were few domestic data to sift through this week, until today’s highly-anticipated jobs report. The labor market added 235k jobs on the month, with some upward revisions to the prior month. Alongside a decline in the jobless rate, these developments have further cemented the case for a rate hike next week.

- With a March hike highly-expected at this point, markets are turning attention to what is in pipeline from the Fed. Three hikes this year, alongside global central banks that remain in highly-accommodative mode should continue to support the U.S. dollar and act as a weight on economic growth. Nonetheless, we expect economic growth to remain resilient supported by continued domestic strength.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

MARCH FED HIKE ALMOST CERTAIN ON STRONG JOBS REPORT

Following last week’s relatively hawkish comments from a number of FOMC members, market participants were waiting to see if domestic data out this week would corroborate the notion that the economy is strong enough to withstand a rate hike. Markets continued to price in a hike this week, with the 2 year treasury yield continuing to face upward pressure as a result, moving up another 7bps by the end of it, at the time of writing. The more aggressive take on Fed policy has provided some support to the dollar, but the strength was offset by less-dovish rhetoric from the ECB, with the DXY just 0.2% higher at the end of the week.

Globally, the ECB’s monetary policy decision on Thursday was in focus. While Draghi hinted at a scenario where the ECB could hike rates while QE is ongoing, it is likely that the central bank will still remain on hold for quite some time. In the context of a Fed that is moving toward a faster tightening cycle when compared to the one and done pace over the last two years, dollar strength will continue to remain an ongoing theme exacerbated by this apparent divergence in monetary policy.

Meanwhile, equity markets seemed to take somewhat of a breather. The S&P 500 closed down on three of the five trading sessions, but ended the week only 0.5% lower, at the time of writing. Higher interest rates and some strength in the USD, was partly to blame, as was the slide in oil prices. Moreover, some of the sell-off was likely related to profit taking as investors cashed in after a long winning streak.

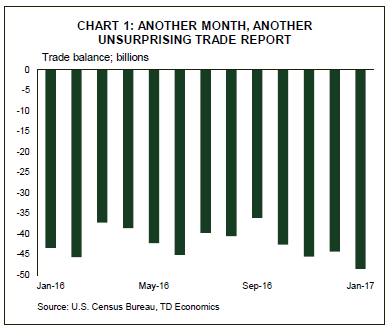

Apart from today’s employment report, there was a scarcity of first-tier domestic data this week. Tuesday’s January international trade report (Chart 1) was concerning, but the increase seen in the trade deficit to $48.5 billion was largely expected and came on the back of a strong rise in imports. It has been widely accepted that drag from net-trade will likely continue as a strengthening U.S. dollar makes imports relatively more affordable and exports more expensive. So, while disappointing given that it places a drag on overall economic growth, it only reinforced the notion that the U.S. consumer remains in good shape.

Still, while the magnitude of the positive surprise in ADP employment, which reported in the middle of the week, provided markets with a bit of a teaser, it was Friday’s payrolls report that stole the show (Chart 2). Non-farm payrolls rose by 235k in February, or well ahead of the 200k expected by the street. Upward revisions also added 9k positions and the unemployment rate ticked down by 0.1% to 4.7%. At this point these developments have cemented the case for a rate hike next week. Wage growth disappointed somewhat, but given the upside revision, accelerated nonetheless from 2.6% to 2.8% in February.

Despite the stronger dollar acting as a weight, we expect economic growth will remain resilient. Irrespective of fiscal stimulus, the economy appears to be at a point where it can handle a few hikes per year, with much of the strength hinging on the strength of the U.S. consumer. This is particularly the case if the data continues to come in robust, with wage and income gains boosting disposable incomes. Ultimately, we expect the Fed to raise rates next week, with two more hikes likely later this year should the economic outlook evolve as expected.

Neil Shankar, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.