FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- It was an exciting week in markets this week, with plenty of domestic and international first-tier data, central bank communication, and the inaugural presidential address to Congress.

- International data has continued to paint a relatively bright picture of the world economy with inflation picking up in the Eurozone, Japan, and the U.K. The positive sentiment was further buoyed by strong PMI data across the globe, suggestive of a strong start to 2017.

- U.S. data was even more encouraging. Apart from some weakness in real spending and construction in January, which came on the back of a strong fourth-quarter, data on from purchasing managers pointed to building strength, with solid momentum in early-2017 also exhibited by regional business surveys, price metrics, and labor market indicators.

- In light of the strong data flow and increasingly hawkish rhetoric out of the Fed, we believe the FOMC will likely raise rates at its next meeting in mid-March, barring any downside surprises, with markets increasingly turning their focus from “when” to “how quickly” any potential hikes may come.

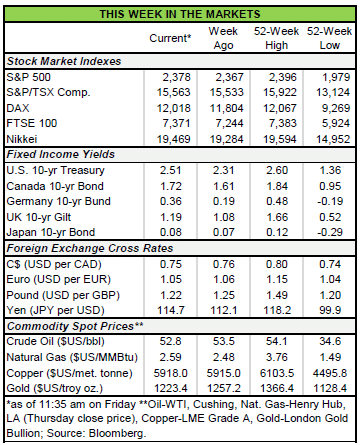

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

Fed Primes Markets for March Hike, Aiming for Hat-Trick in 2017

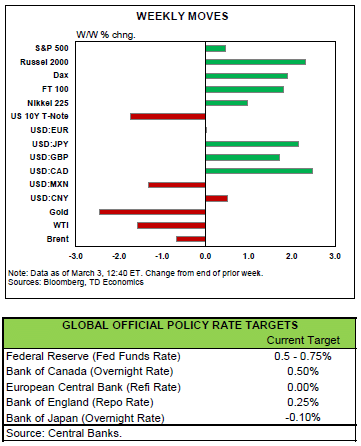

It was an exciting week in markets this week. Alongside a much awaited tech IPO, there were plenty of first-tier data (both domestic and international), central bank speeches, and the inaugural presidential address to Congress. International data came in broadly constructive, while U.S. data came in even more robust. Alongside indications of rapid deregulation by the executive branch, and relatively hawkish remarks from FOMC members across the spectrum, this placed upward pressure on yields and pushed the odds of the March hike from just 1/3rd last week to near-certainty as of the time of writing. Markets now expect between 50 and 75 basis points of tightening this year. The more aggressive take on Fed policy has seen the U.S. dollar rally by nearly 1% across the common-traded basket. The higher dollar was not helpful to oil prices, which were already under pressure from building U.S. inventories. Still, sentiment was running high since mid-week, with U.S. equity indices setting new records and the Dow surging north of 21,000.

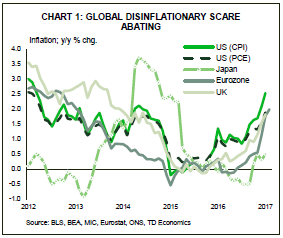

International data has continued to paint a relatively bright picture of the world economy. Inflation picked-up to a four-year high in Japan and has been accelerating in Europe and the U.K. (see Chart 1). While much of the headline print is related to rising oil prices, it nonetheless has pushed deflationary fears from investors’ minds. The price data was not alone in boosting sentiment, with the purchasing manager indices across the main global economies showing signs of health. Eurozone PMIs held near just north of the mid-50s mark, suggesting GDP growth of around 2% in the common-currency area, with the U.K. PMI holding near that mark also. Chinese PMIs, while lower, were healthier

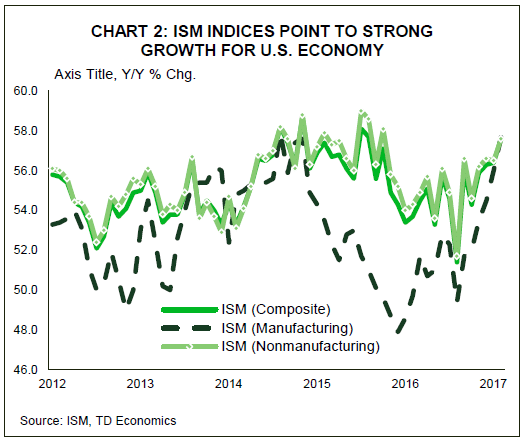

U.S. data was arguably even more constructive. While real consumption and construction disappointed in January, the monthly print at the start of the year, when seasonal factors are the highest, is notoriously volatile and has been misleading in previous years. Moreover, it comes atop of a strongly revised PCE print in the fourth quarter of 2016 – when consumers increased spending by a healthy 3% according to the second estimate of GDP. Other indicators, including ISM indices from both the manufacturing and nonmanufacturing sectors suggest the economy is progressing at a very healthy pace. Such sentiment is corroborated

by regional business surveys, durable goods orders data, and price metrics – with core PCE inflation rising by a decade-high 0.3% on the month.

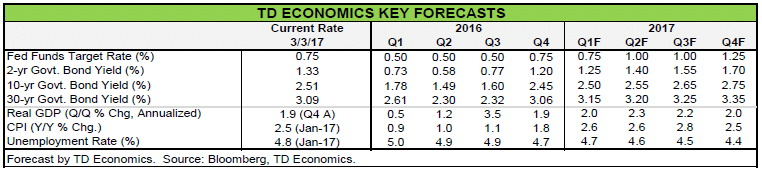

While core PCE inflation – the Fed’s favored measure of price pressures – remains shy of the FOMC’s target at just 1.7% on a year-on-year basis, there is little question that the movement up has been swift. Given the wage pressures that have manifested in recent months, and are likely to continue to rise given the ever tightening labor market (initial claims fell to a 44-year low) and the lagged spillover from oil prices, it is likely that the measure will approach the 2% target as the year progresses. With this in mind, a more favorable international backdrop, and markets that are effectively giving the Fed a clear opportunity to hike in March, we believe the FOMC will take the opportunity – particularly given its proclivity to move earlier, but more gradually.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.