Financial News Highlights

- Negotiators appeared close to a deal to raise the debt ceiling and set spending levels. However, the deal does not address Washington’s medium-term fiscal challenges, which were part of the reason Fitch put the U.S. on a negative watch.

- Consumers continued to spend at a healthy clip in April, contributing to sustained inflation pressures. We continue to expect spending to cool as the year goes on, helping to ease inflation, eventually.

- In the meantime, the Fed is in a tough spot. It will need courage to pause and wait for the full impact of its past tightening to show up.

“Discretion” Is the Better Part of Valor in Washington

Thankfully, negotiators appeared close to a deal to raise the debt ceiling as of Friday morning in financial news. It looks like the two-year deal would cap discretionary spending and raise the debt ceiling through the 2024 election, avoiding the worst-case scenarios. However, ratings agency Fitch had cited the “failure of the U.S. authorities to meaningfully tackle medium-term fiscal challenges” as a reason for putting the U.S. on a negative watch, and this deal does not change that.

Thankfully, negotiators appeared close to a deal to raise the debt ceiling as of Friday morning in financial news. It looks like the two-year deal would cap discretionary spending and raise the debt ceiling through the 2024 election, avoiding the worst-case scenarios. However, ratings agency Fitch had cited the “failure of the U.S. authorities to meaningfully tackle medium-term fiscal challenges” as a reason for putting the U.S. on a negative watch, and this deal does not change that.

Congress has taken the Shakespearean proverb “discretion is the better part of valor” literally. The Bard’s original intention was a criticism of a lack of honour and courage in focusing on discretion. The debt ceiling deal only tinkers around the edges of the larger issue of a structural deficit on the order of 6% of GDP.

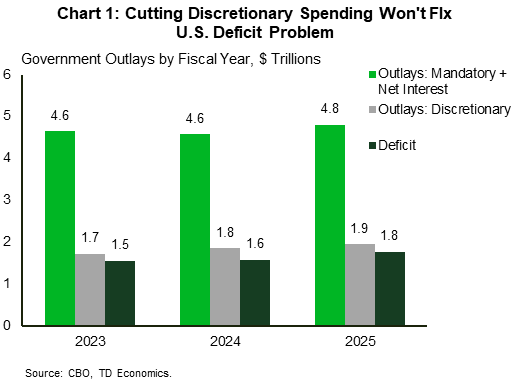

Discretionary spending accounts for only 27% of total federal government outlays, and the federal deficit is estimated to be $1.5 trillion in 2023. As shown in Chart 1, Congress would need to cut discretionary spending nearly to zero to balance the books if they only address discretionary spending. To seriously address the deficit, it needs to take the more courageous steps and look at mandatory spending – namely entitlements like social security and Medicare. Or, it needs to find a way to grow revenues at the same pace as population aging. Alas, courage seems in short supply in Congress these days.

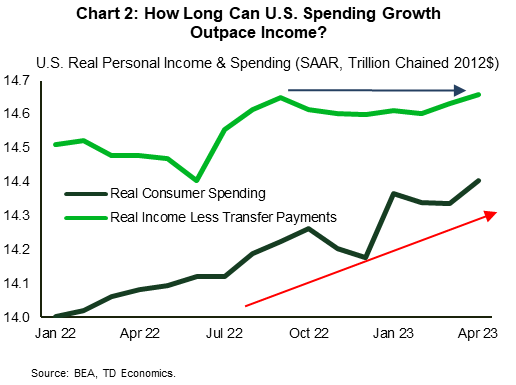

Speaking of discretion in spending, real consumer spending was up a healthy 0.5% month-on-month in April in financial news. Spending was driven by robust gains in outlays on both goods and services. Monthly spending data has been very choppy over the past six months but comparing it to real income less transfer payments (which is a key recession indicator used by the NBER), you see that the upward trend in spending is outpacing real income growth (Chart 2).

Thanks to a strong labor market, real income gains have held up. Added to the cushion of excess savings built up during the pandemic, the consumer has been able to keep spending in the face of very high inflation, in turn contributing to demand-driven inflation pressures. Chart 2 suggests that spending is set to slow – even if the labor market doesn’t cool. About 60% of the excess savings cushion has been spent, and spending cannot outgrow income indefinitely before consumers will need to tighten their belts.

Thanks to a strong labor market, real income gains have held up. Added to the cushion of excess savings built up during the pandemic, the consumer has been able to keep spending in the face of very high inflation, in turn contributing to demand-driven inflation pressures. Chart 2 suggests that spending is set to slow – even if the labor market doesn’t cool. About 60% of the excess savings cushion has been spent, and spending cannot outgrow income indefinitely before consumers will need to tighten their belts.

We expect that belt tightening to be in greater evidence as the year goes on. After consumer spending grew by 3.8% annualized in Q1, it is tracking a more modest 2% in Q2. We expect it to fall below 1% in the second half of the year, which will help to dampen inflationary pressures. Until then, the Fed is on the horns of a dilemma.

Its preferred inflation gauge, the core PCE deflator, remained around where it has been all year at 4.7% year/year in April. Markets are judging this could mean the Fed should push a bit harder on rates, with market odds tilting slightly in favor of another hike in June. We believe that the Fed will need to hold its courage and pause and assess the impact of the significant monetary policy tightening that has not yet had its full impact on economic growth.

Leslie Preston, Managing Director & Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.