Financial News Highlights

- The Federal Reserve hiked the policy rate 25 basis points this week, lifting it to a 16-year high of 5.00-5.25%. Changes in FOMC statement hinted at the potential for a pause, though Chair Powell stated that such a decision had not been made.

- The banking stress continues to fester, with this week marking the failure of another bank (First Republic).

- Though still slowing on a trend basis, hiring ticked up in April, with the economy adding 253k jobs. That was above market expectations for a gain of 180k, but downward revisions to the prior months tempered the optimism.

Fed Lifts Policy Rate to a 16-year High

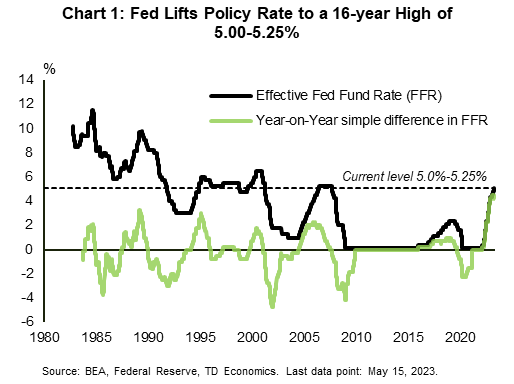

The Fed followed through with its highly anticipated decision to hike the policy rate by 25 basis points (bps) this week in financial news. This lifted the fed funds rate to 5.00-5.25% – the highest level in 16 years – in what has been a historically aggressive hiking cycle (Chart 1). Changes in the FOMC statement hinted at the potential for a pause, so this could very well be the last hike of this cycle. But, stating this explicitly would not serve the Fed well at this point. In the press conference, Chair Powell tried to keep his options open, stating bluntly that a decision on a pause had not been made.

The Fed followed through with its highly anticipated decision to hike the policy rate by 25 basis points (bps) this week in financial news. This lifted the fed funds rate to 5.00-5.25% – the highest level in 16 years – in what has been a historically aggressive hiking cycle (Chart 1). Changes in the FOMC statement hinted at the potential for a pause, so this could very well be the last hike of this cycle. But, stating this explicitly would not serve the Fed well at this point. In the press conference, Chair Powell tried to keep his options open, stating bluntly that a decision on a pause had not been made.

The Fed’s communication is at odds with market expectations. Markets are dismissing the possibility of further rate hikes and are instead signaling that after a brief pause the Fed will begin cutting rates. Market odds as tracked by the CME Group point to 75 bps in cuts over the last few months of the year. Asked about this divergence, Powell pushed back against the notion of soon-to-come cuts in financial news. In his words, the reasoning is that the Fed sees inflation coming down “not so quickly”, and that if that outlook proves to be broadly correct then “it would not be appropriate to cut rates”.

Fed Chair Powell noted that upcoming policy rate decisions would ultimately be data-dependent, mentioning the usual suspects (i.e., inflation and labor market metrics), while also putting a focus on credit conditions. Tighter credit conditions ultimately serve a similar purpose to rate hikes when it comes to cooling economic growth and inflation. This is something that the Fed considers in setting monetary policy, especially in light of the recent banking stress, with this week marking the failure of another regional bank. Powell had access to the Senior Loan Officer Opinion Survey (SLOOS), due to be released publicly on Monday, and noted that it would show a tightening in credit conditions among small and medium sized banks.

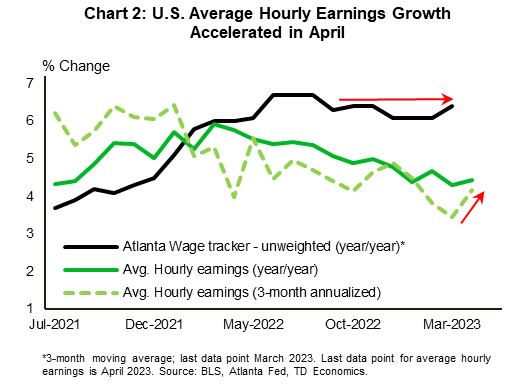

Factoring in the banking stress and tighter credit conditions suggests that the Fed has done enough, but labor market resilience continues. On the one hand, the pace of job creation continues to trend down on a three-month moving average basis. On the other hand, it’s hard to discount the strength in the April jobs report. The economy added 253k jobs last month – well above expectations for 180k. Gains were concentrated in service sectors (+197k). The labor force participation rate held flat at post-pandemic high of 62.6%, while the unemployment rate ticked down to 3.4%, matching January’s multi-decade low. Amidst the ongoing tightness in the labor market, growth in average hourly earnings accelerated both on a year-on-year and month-on-month basis, while other wage measures also point to some resilience (Chart 2).

Factoring in the banking stress and tighter credit conditions suggests that the Fed has done enough, but labor market resilience continues. On the one hand, the pace of job creation continues to trend down on a three-month moving average basis. On the other hand, it’s hard to discount the strength in the April jobs report. The economy added 253k jobs last month – well above expectations for 180k. Gains were concentrated in service sectors (+197k). The labor force participation rate held flat at post-pandemic high of 62.6%, while the unemployment rate ticked down to 3.4%, matching January’s multi-decade low. Amidst the ongoing tightness in the labor market, growth in average hourly earnings accelerated both on a year-on-year and month-on-month basis, while other wage measures also point to some resilience (Chart 2).

Should the strength seen in April extend in the months ahead, it could push the Fed to hike a bit more. However, other labor market indicators – such as job openings, which are trending down, and initial jobless claims, which continue to trend up – are not in tune with this view. All told, the upcoming data will continue to bear careful watching, with next week’s CPI report next under the magnifying glass.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.