FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The Fed raised the monetary policy rate by 50 basis points for the first time since 2000 and signaled more hikes of the same magnitude are in the works.

- The economy added more jobs than expected in April, but the labor market remains tight with the number of workers looking for jobs retreating.

- Supply constraints continue to create a mismatch between demand and supply. Should supply fail to improve, inflation will remain high, making the Fed’s job more difficult.

U.S. -Tight Corners of the Economy

This was a big week for the U.S. economy with a Federal Reserve interest rate decision and early macroeconomic indicators for the month of April in financial news. As widely anticipated, the Fed raised the monetary policy rate by 50 basis points for the first time since 2000. More tightening is in the works: we anticipate the central bank will hike the fed funds rate in two more 50 basis point moves at its next two meetings. A that point, we expect it to return to more gradual quarter-point adjustments (see Dollars & Sense). Chair Powell’s push back against the possibility of a larger hike was first accepted as bullish by the equity market, but the sentiment reversed quickly pushing the equity market a quarter of a percent lower and bond yields 15 bps higher for the week (at the time of writing).

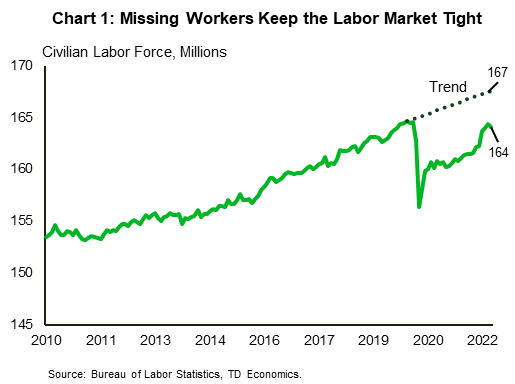

This morning’s jobs report surprised with 428k jobs added in February, according to the payrolls survey, well above 380k anticipated by forecasters. The unemployment rate, which is measured by the household survey held steady 3.6%. The labor force – a measure of people working or actively looking for work – dropped unexpectedly, pushing the participation rate down to 62.2%. As a result, an already sizeable shortfall relative to the pre-pandemic trend, expanded even further (Chart 1). Without progress on this front, the labor market will remain very tight, providing little relief for businesses already struggling to attract workers.

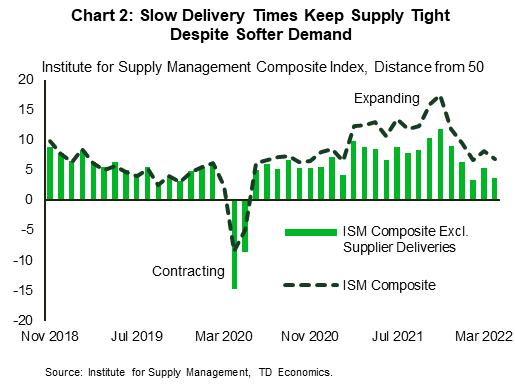

Meanwhile, leading business indicators – the ISM purchasing managers indexes – came in weaker than expected by the consensus, while remaining in the expansionary territory. The manufacturing sector decelerated for the second month in a row. All major subcomponents but the supplier deliveries index declined, with the largest drop in the employment index. Softness in demand is consistent with our expectation that consumers start to cut back on manufactured products in favor of services. In this context, a deceleration in the services sector was somewhat disappointing. The underlying details suggest that current business activity accelerated, but new orders and new export orders slipped. Another drag was the employment sub-index, which dropped back into the contractionary territory, likely due to “hypercompetitive” demand for workers, as suggested by one of the purchasing managers.

Importantly, supply constraints and challenges in logistics continue to create a mismatch between demand and supply in both sectors of the economy. Comparing to history, the supplier delivery index has been unusually strong since March of 2021, creating a wedge between this sub-component the rest of the index’s drivers (Chart 2). Another way to think about it is that delivery times remain atypically slow relative to softer demand.

Should supply fail to improve in lock steps with demand softening, inflation is likely to remain elevated in financial news. This will make it more difficult for the Fed to soften growth without crushing the economy into a recession. The good news is that the strength of consumer finances points to a softening in spending, rather than an outright retreat (see report). This should help the Fed navigate the economy out of its tight spot.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.