FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

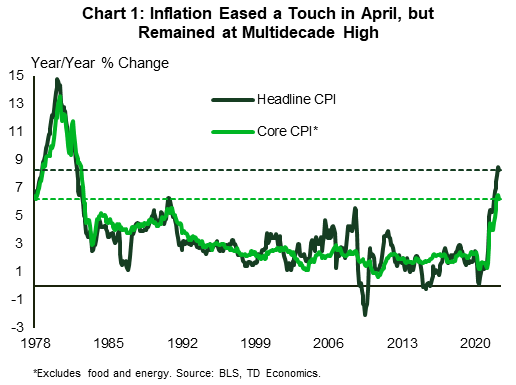

- The consumer price index (CPI) report showed that both overall and core price pressures eased a touch in year-over-year terms in April. Overall inflation fell to 8.3% y/y from 8.5% in the month prior, while core inflation fell to 6.2% from 6.5%.

- The producer price index (PPI) report echoed a similar message, with producer prices decelerating modestly in April to 11% y/y, but remaining near March’s record high of 11.5%.

- Signs of a slight tick down in inflation will do little to dissuade the Fed from removing monetary stimulus expeditiously. Despite staging a notable recovery on Friday, the S&P 500 looks to end the week down over 2%

U.S. -Slight Pullback in Inflation Won’t Change Fed’s Mind

The second week of May carried a light economic calendar, with primary data releases continuing to center on inflation in financial news. The consumer price index (CPI) report showed that inflationary pressures eased a bit in April, falling to 8.3% year-on-year (y/y) – down from 8.5% in March (Chart 1). Base effects are likely to have played a favorable role, as price pressures stemming from supply chain disruptions began to manifest in March and April of last year.

Beneath the headline, food inflation accelerated both in yearly and monthly terms, whereas energy prices eased a touch. Both, however, remain elevated at 9.4% y/y and 30.3% y/y, respectively. Excluding these two volatile categories, core prices also decelerated modestly, falling to 6.2% y/y from 6.5% y/y in March. However, several important categories bucked the trend. On the goods side, new vehicle prices were higher, while medical care, transportation, and shelter were all meaningful contributors on the services side. The transportation category was buoyed from airfares, which continued to rise sharply (18.6% m/m). Meanwhile, market-based measures of strong home price and rent growth suggest that the weighty shelter component has more upside ahead. This, together with the fact that gas prices have resumed their upward climb this month, and that we’re likely to see further upward pressure in food prices from the war in Ukraine, muddy the CPI report’s headline message that inflation may have peaked, making it prudent to wait for further confirmation to this notion in financial news.

The producer price index (PPI) report echoed a similar message to last month’s CPI numbers. Producer prices were up 11% from a year ago in April, marking an easing from an upwardly revised 11.5% y/y in March. Core PPI also eased a touch. That being said, April’s PPI showings, which are not far off from the March record highs, indicate that inflationary pressures continue to build in the production pipeline.

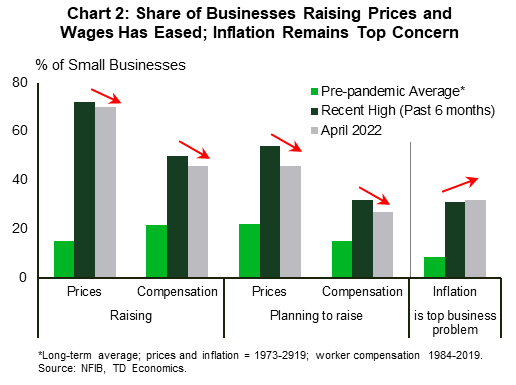

The small business report from the NFIB provided more of the same. In Chart 2 we can see that while the share of businesses raising (and planning to raise) average selling prices and worker compensation have eased from recent highs, they remain well above historical norms. On the other hand, the share of businesses identifying inflation as their top business problem reached a new post-1980 high in April. Another striking feature of the report is the fact that the share of small businesses expecting an improvement in the economy in the months ahead fell to a yet new record low (-50%).

Doubtful expectations about a further improvement in the economy have some basis. Signs of a slight moderation in inflation will do little to dissuade the Fed from removing monetary stimulus expeditiously, which in turn will weigh on economic momentum. In tune with this notion, risk assets continued their downward slide this week. Despite a notable bounce back Friday, the S&P 500 is down 2.6% from last week’s close and roughly 16% from peak. Of course, as Fed Chair Powell noted this week, there’s no guarantee that the Fed will see smooth sailing in its goal to engineer a soft-landing. In a speech Thursday, Chair Powell, who was recently confirmed for a second term, noted that getting inflation back to 2% will cause “some pain”. For now, however, we’re still full ship ahead with another 50-basis point hike in June.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.