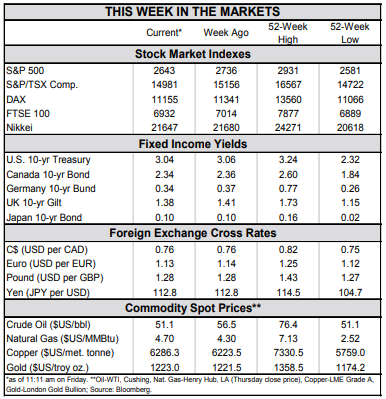

HIGHLIGHTS OF THE WEEK

- Equity market volatility persisted this week as the main indexes were dragged down by tech and energy stocks. The latter resumed their slide as oil prices fell to their lowest levels in more than a year.

- Housing data was mildly positive, but continued to drive in the point that the sector remains a sore spot. Both existing home sales and housing starts rose around 1.5% month on month in October. But, sales are still down some 5% year on year, weighing on builder confidence.

- Presidents Trump and Xi will meet at the G20 summit next week in Buenos Aires. Any conciliation would be a plus for financial markets. Here’s hoping that the atmosphere and outcome are as pleasant as the host city’s name.

Despite Sour Week, There Is Still Plenty to Be Thankful for

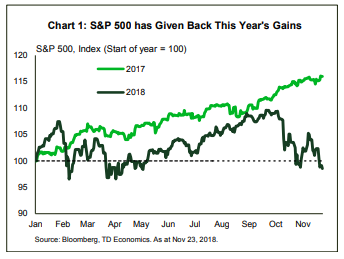

Despite the carnage in equity markets, there is still plenty to be thankful for. The U.S. economy remains the growth-leader among the G7 and appears likely to retain its lead over the next year. Its labor market echoes this strength, with more job openings than there are unemployed Americans. This backdrop has allowed the Fed to raise interest rates at a faster pace than its peers and also gives it the flexibility to respond to any future hiccups in growth.

With interest rates rising, resale activity is likely to remain soft. Still, a strong labor market and a more gradual increase in mortgage rates going forward should limit the downside. Median home price growth has moderated to 3.8% year on year, which alongside rising wage growth, will limit the hit to affordability as mortgage rates rise. An improvement in the number of homes for sale in recent months also marks a positive step. Still, inventory levels are historically low and this imbalance should ultimately help housing starts retain their mild upward trajectory over the medium term.

Aside from the housing market, developments on the trade front bear close watching. Next week’s G20 summit appears an ideal setting for President Trump to announce a deal with his Chinese counterpart. Without progress, tariff rates are likely to increase in January, which could further undermine market confidence. As Trump and Xi tango in Buenos Aires next week, here’s hoping that the atmosphere and outcome are as pleasant as the host city’s name. Should trade tensions continue to fester, and confidence take a further hit, the Fed’s preferred path of rate hikes will come into question.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.