HIGHLIGHTS OF THE WEEK

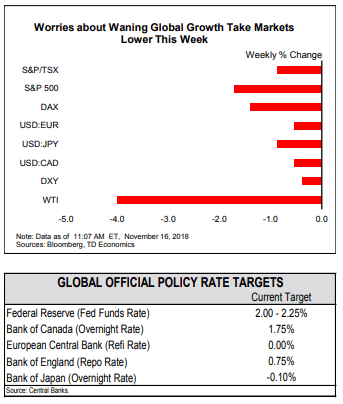

- Equity markets were volatile again this week as concerns over global growth remained top of mind for investors.

- Economic data continues to point to solid economic growth stateside, with little signs that global weakness has caught on domestically.

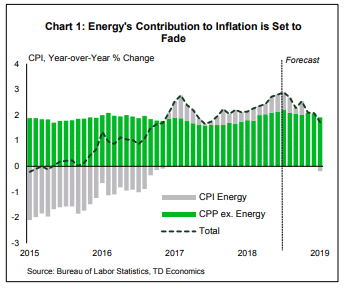

- Inflation data for October showed a relatively benign picture. While the headline rate rose to 2.5% (from 2.2%), core inflation edged lower on the month.

Growth is Solid, Inflation is Benign, Why Worry?

Financial market jitters are not a reflection of any newfound weakness in U.S. economic data, which continues to point to solid growth and limited inflation. This week, consumer price index (CPI) data for October showed headline inflation rise to 2.5%, mainly due to rising energy prices. Core inflation, on the other hand, edged down to 2.1% (from 2.2%). Over the past three months, core prices have risen an average of just 1.6% (annualized), suggesting little cause for alarm on the price front. What’s more, the recent pullback in the price of oil is likely to push headline inflation lower in the months ahead, with the Fed’s preferred metric – the personal consumption expenditure price index – likely to drift back below the 2% mark.

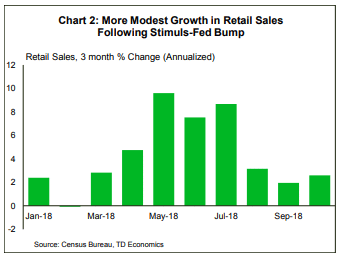

Other economic data confirmed the solid economic growth narrative. Retail sales rose a robust 0.8% in October, reversing a downwardly revised pullback in sales in September. The drop in September and rebound in October reflected hurricane-related disruptions. Overall, the retail sales data are consistent with real consumer spending advancing by around 2.5% in the fourth quarter. For all intents and purposes, this is a great number. Nonetheless, it does represent a deceleration from the heady 3.9% pace average over the second and third quarters of the year.

With real consumer spending likely to run in the mid-2% range, the overall economy is likely to follow suit. In this environment, the impact of tariffs is likely to be more noticeable. Already there are signs that businesses are attempting to get ahead of the scheduled increase in Chinese tariffs to 25% (from 10%) by stockpiling imports. This volatility makes reading the economic tea leaves and the job of the Fed in gauging the reaction of the economy to higher interest rates that much more difficult.

James Marple, Senior Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.