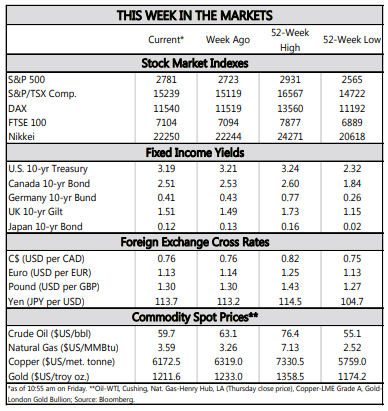

HIGHLIGHTS OF THE WEEK

- Between the midterm elections and a Fed rate decision there was plenty of news this week. But after the dust settled there was very little new information.

- In the midterm elections, Democrats gained a majority in the House of Representatives, and Republicans tightened their grip on the Senate. A divided Congress through 2020 will temper parts of Trump’s agenda, and could make some upcoming fiscal tests more challenging.

- As expected, the Federal Reserve left rates unchanged, with a largely unchanged statement. Recent economic data suggest the next hike is coming in December.

Plenty of News, But Not Much New

Congress is now gridlocked through 2020, which raises risks on a variety of fronts. A few tests loom on the near-term horizon. Currently 25% of discretionary spending for the 2019 fiscal year is under a temporary funding agreement until December 7th. The current Congress will likely kick the can into early 2019, which sets up a potential funding battle and the risk of a partial government shutdown in the New Year. Government shutdowns are a risk with a divided government, but typically these do not have a meaningful impact on economic activity (as they have not proved long lasting).

As President, Trump has the authority to push ahead with his trade agenda. He may even get some support from the Democratic House for a harder stance on China. As such, the increase in Chinese import tariffs to 25% from 10% on $200bn of goods on January 1st is more likely than not, presenting a downside risk to our forecast.

Finally, there was little new from the Fed. The statement’s characterization of the economy was broadly unchanged. The slight updates that were made merely reflect the latest data, and are not major new developments. Most importantly, the Fed said it “expects that further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity…” and that “risks to the economic outlook appear roughly balanced”. The recent economic data certainly point to a rate hike at the December meeting.

Most recently, October’s Producer Price Index showed that inflationary pressures are alive well further up the supply chain. And while consumer price inflation hasn’t heated up in recent months, price hikes are likely coming in many sectors as margins are increasingly squeezed.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.