HIGHLIGHTS OF THE WEEK

- The U.S. labor market continues to impress – churning out jobs like nobody’s business (+250k), keeping the unemployment rate near record lows (3.7%), drawing people into the labor force (participation rate up +0.2 percentage points), and pushing up wages to boot (3.1% year-on-year – the highest since 2009)

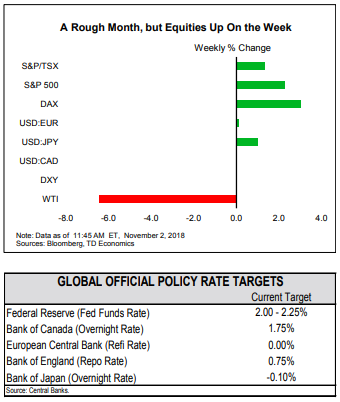

- The fly in the ointment? A fierce sell off in equity markets in October, putting in question the more than nine-year-old stock bull market. Major stock indices closed the month down, eking out only marginal gains year-to-date.

- Trade tension with China is one catalyst for market jitters. A phone call between Presidents Xi and Trump this week signals progress, but the jury is still out on whether a broader trade war can be avoided.

Economy is Hot, but Markets Worried About the Future

The tight labor market is indeed forcing many to compete for workers by boosting paychecks. Both the employment cost index, which captures wages and benefits, as well as average hourly earnings show upticks in workers’ compensation. Wages broke through the 3% growth ceiling that has stood for nearly a decade, coming in at 3.1% y/y. Wages haven’t exceeded 3% growth since April 2009 (Chart 1).

Going in the opposite direction, home-price gains decelerated for the fifth consecutive month in August. The S&P Case-Shiller Home Price Index grew 5.8% y/y, falling below 6% for the first time in a year. After more than five years of solid home price growth, this is the latest indication of a slowdown in the housing market, which is likely to persist as interest rates edge higher. Despite slowing, house price inflation remains well above wage growth, contributing to the affordability crunch prospective buyers have grappled with of late (Chart 2).

Rounding out the week were data on ISM manufacturing and personal income and spending. Manufacturing activity eased in October, though it remained in growth territory as manufacturers continued to struggle with capacity constraints and tariff pressures. Though consumer spending momentum remained strong through the end of Q3 and should result in a solid Q4 handoff, the stimulus from tax cuts likely plateaued in Q3 and could be a harbinger of slower consumer spending. Year-on-year, core PCE inflation remained at 2.0% for a fifth straight month.

One potential development that could raise inflation (and further reduce the stimulative impact of tax cuts) are higher tariffs. On that front, tensions with China continue to simmer. This week, the Commerce Department barred U.S. companies from engaging in business with a state-owned Chinese chip maker after it was accused of stealing trade secrets from an American firm. The news left China’s chip industry on edge, feeling vulnerable to the escalating China-U.S. trade standoff. Subsequently, a spark of hope emerged Thursday when President Trump signaled progress on trade talks. This followed a phone call, initiated by the White House, to President Xi. The two countries are now more likely to resume talks at the G-20 summit in Buenos Aires later this month. As things stand, however, the jury is still out on whether there will be a cease fire in the trade fight following the summit.

All told, the U.S. economy is currently enjoying the sweet-spot of low inflation and unemployment. Only time will tell for how long.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.