HIGHLIGHTS OF THE WEEK

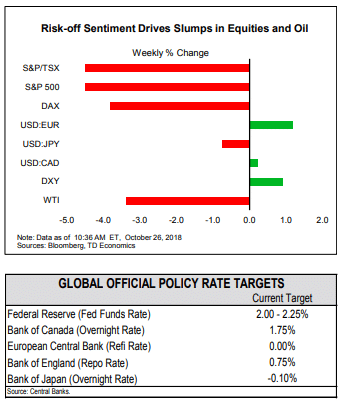

- It was a sea of red in equity markets this week as risk off sentiment set in. As it stands, downturn in October has erased all the stock market gains from the start of the year.

- International developments didn’t help to lift investors’ spirits. The U.S. – China trade negotiations appear to have hit a stalemate, and the European Commission has rejected Italy’s government budget.

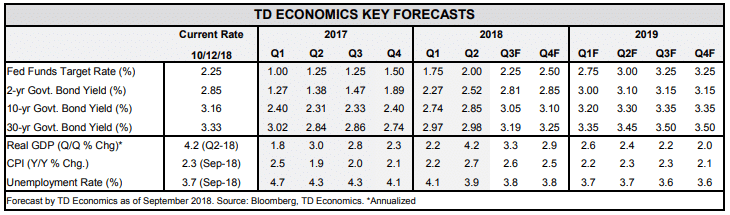

- Domestically, the advance estimate of Q3 GDP was the only major data release this week. After an impressive Q2, the U.S. economy has downshifted slightly in Q3, but at 3.5% (annualized), growth has nonetheless remained very hot and well above potential, giving the Fed ammunition for another rate hike in December.

Economy is Hot, but Markets Worried About the Future

International developments didn’t help to lift investors’ spirits. It seems that the U.S. – China trade negotiations have hit a stalemate. This threatens to undermine a scheduled meeting between the two presidents in November, and raises the probability of further tariffs. Also, in an unprecedented (even if widely expected) step, the European Commission has rejected Italy’s budget.

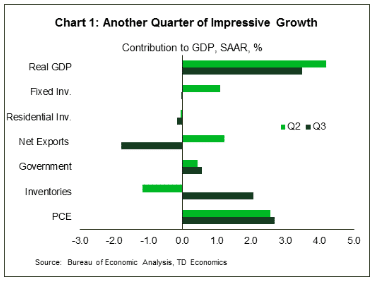

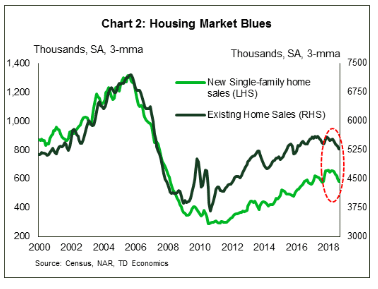

Even as consumers are hitting malls in masses, the housing market remains unloved due to deteriorating affordability and lack of supply. Sales of new and existing homes are down by 11% and 6%, respectively, since December (Chart 2). With both homebuilders and prospective buyers facing a number of hurdles, residential investment has been contracting for three consecutive quarters.

Business investment was another fly in an ointment in today’s GDP report. After setting a blistering pace in the first half of the year, spending took a breather in the third quarter, up only 0.8%. While one quarter does not make a trend, given the tensions on trade front this is where the risks lie going forward. Tariffs have already dented business confidence and could lead to further delays in investment in the coming quarters. If investment spending continues to be soft, dampening economic growth, the Fed would likely temper the pace of rate hikes.

All in all, with trade risks percolating and the boost from fiscal stimulus expected to fade, performance over the last two quarters likely represents the high water mark for the U.S. economy. So far though, despite President Trump taking yet another jab at the Fed this week, it certainly looks like current economic fundamentals warrant another interest rate hike in December, bringing the upper end of the target range to 2.5%.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.