FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Equity markets stopped hemorrhaging and partially recovered from last week’s downturn. Domestic data was predominantly underwhelming, but did little to change the status quo of a solidly-growing U.S. economy.

- Retail sales, existing home sales and housing starts all fell in September, with figures likely swayed by Hurricane Florence. Core retail sales however, rose by 0.5%, which suggests that consumption grew at a healthy 3% (ann.) in Q3.

- The FOMC minutes reinforced the view for continued interest rates hikes. Still, downside risks are percolating (mostly external) and the path ahead will require careful navigation.

Plenty of Potholes Will Require Careful Navigation Ahead

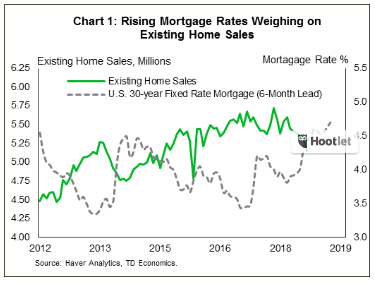

Despite a strong consumer backdrop, the housing market continues to struggle. Existing home sales fell 3.4% in September, marking the sixth straight monthly decline. Housing starts didn’t do any better, falling 5.3% to 1.20 million. Again, part of the weakness can be chalked up to weather-related disruptions, with both existing home sales and starts in the South recording the sharpest drops since late 2015. Going forward, tight inventories of homes for sale should help support moderate gains in new homebuilding. Still, limited supply will keep upward pressure on prices and weigh on demand, especially in the near-term. Rising interest rates, which appear to be behind some of the recent malaise, will be an added headwind (Chart 1).

While the data remain supportive of ongoing rate hikes, there is no shortage of potholes in the path ahead, particularly on the international front. Across the pond, Brexit remains a source of uncertainty, while recent developments in Italy have also become a major cause of concern. The EU Commission has determined that Italy’s draft budget is in serious breach of EU budget rules, and may reject it. The Rome-Brussels rift, which has sent Italian bond yields skyward (Chart 2), will bear close watching next week with Italy expected to reply to the commission by Monday. Chinese economic growth is slowing and policymakers there have a tough balancing act between deleveraging and maintaining adequate growth. A sour exchange between trade representatives of the EU and U.S. this week also reminds us that the Trans-Atlantic trade truce rests on feeble foundations. All told, plenty of risks remain and it won’t be an easy path to navigate.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.