HIGHLIGHTS OF THE WEEK

- The S&P500 has seen its biggest five-day loss since February this week. Much like then, higher bond yields have led to a repricing of stocks.

- There are few signs the U.S. economy is cooling. September consumer price inflation data showed that inflation pressures remain quite contained.

- On net, this argues for a continued gradual pace of rate hikes by the Fed. A severe tightening in financial conditionswould put this at risk, but there is little evidence of that yet.

Stocks Adjust to Higher Yields

For its part, the U.S. economy continues to do well. Indeed, stocks have weakened in part because the economy is doing well. The Fed has clearly signaled they expect strong economic growth to continue, and expect to continue raising rates over the coming year. Bond markets are increasingly taking them at their word, and investors now require a higher yield to hold bonds. When analysts value equities, they discount the expected future cash flow or dividends, and with higher rates those discounted cash flows are looking less valuable, resulting in a repricing of stocks.

There are plenty of downside risks lurking around corners for the U.S. economy: negative impacts from increased tariffs; higher government deficits could lead to a further move up in Treasury yields; and the risk of a Fed policy error. But, at the moment it must be acknowledged that the U.S. economy is growing strongly, a healthy labor market is increasing the share of people with jobs, and wage gains are occurring. At the same time, inflation pressures remain very well behaved. That helps ensure the Fed can remain patient as it raises policy rates.

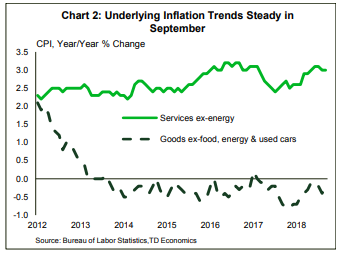

Meanwhile, services inflation has picked up from its 2017 soft patch, but it hasn’t really broken new ground. We continue to expect a tight labor market, and increased wage pressures to lead core inflation higher over the next year. But, September’s inflation numbers provide reassurance that an undesirable sharper upturn is not occurring. We expect the Fed to continue raising rates a quarter point at every other meeting over the next year. It would take a much more severe tightening in financial conditions than recently observed to put this pace at risk.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.