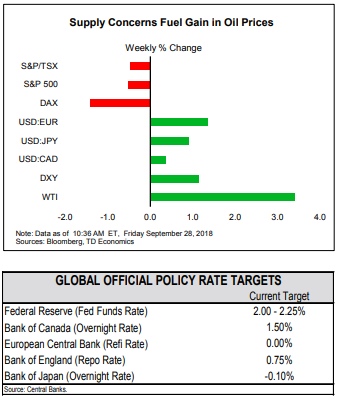

HIGHLIGHTS OF THE WEEK

- Fed hiked rates by 25 bps this week as widely expected. But, the communiqué dropped the reference to policy remaining “accommodative”. Interpretations regarding this change led to volatility in bond yields and equities.

- The debate on textual changes in the Fed statement detracts from the main point: the Fed remains committed to additional tightening – a message echoed by a broadly-unchanged rising interest rate path in the Fed dot plot.

- Despite not being all positive, economic data reaffirmed the notion that the U.S. economy remains on solid footing. Of note, real personal spending rose 0.2% in August, keeping our tracking for Q3 consumption above 3% (ann.).

Don’t Let Textual Changes Get in the Way of Rate Hikes

Market focus however, gravitated more toward what was not in the Fed statement, rather than what was in it. The communiqué dropped the reference to policy remaining “accommodative”. This received a dovish interpretation initially under the premise that the Fed may be getting close to the end of the hiking cycle, leading to volatility in bond yields and equities.

The debate around textual changes in the Fed communiqué appears to detract from the main point – the Fed remains committed to further gradual tightening given its conviction for well-anchored inflation expectations and a positive view of the economy. Economic data in the week remained broadly in line with this narrative. The Fed’s preferred measure of inflation held right on target for the fourth straight month in August. Meanwhile, real personal spending was up 0.2% in the same month. While this marks a slight moderation in the monthly pace of spending, it’s sufficient to keep our tracking for third quarter consumption growth north of 3% annualized. A solid rise in wholesale and retail inventories added to the positive tally.

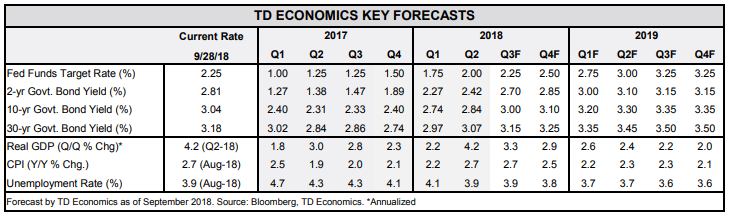

Putting all the pieces together, the economy is still on solid footing, with over 3% growth expected in the third quarter. With price pressures holding near target, this should indeed be sufficient for one more hike before the end of the year. Beyond this point, however, there is significantly more uncertainty, as trade disputes pose significant downside risk to the economic outlook.

The U.S.-China trade conflict saga continued to play out in the background, given other more salacious domestic political developments. China scrapped talks with the U.S. as tariffs on $200 bn of Chinese goods came into effect. Meanwhile, President Trump accused China of attempting to interfere in the upcoming midterm elections, given his stance on trade. With the two economic heavy-weights on a hard-to-avoid collision course, we see this dispute as a key risk to growth. Tariffs in effect and those threatened could knock off up to 1 p.p. from U.S. and 0.3 p.p. from global economic growth (see here).

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.