Financial News Highlights

- The Federal Reserve’s policy statement took center stage this week in financial news. As expected, the Fed kept policy rates unchanged but preserved the option of hiking in the future.

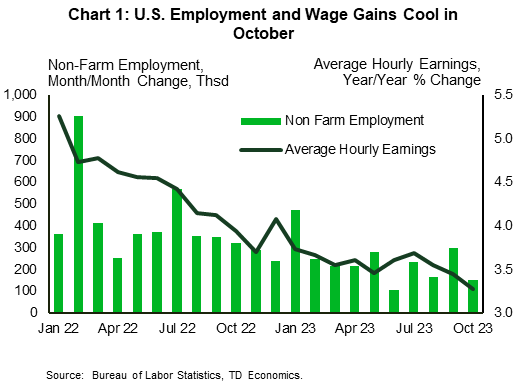

- Hiring in the U.S. slowed in October, with wage gains decelerating and the unemployment rate edging up.

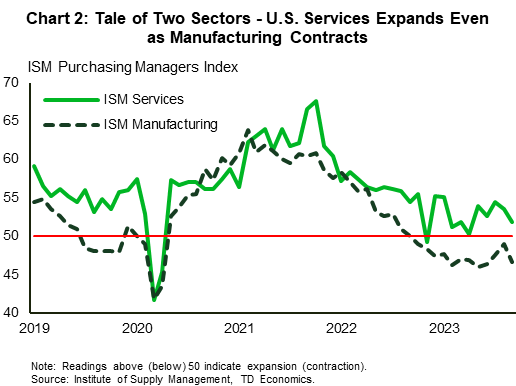

- Activity in the manufacturing sector continued to contract in October, in contrast to the continued expansion in the services sector (though at a slower rate).

The Fed’s Door is Still Open

The U.S. economic calendar was packed this week with a mix of key data, central bank meetings and even Treasury auction announcements. To start things off, the Treasury announced its financing requirements for the upcoming quarter. In the announcement, issuance is dominated by shorter dated securities (2-7 year), with planned 10-to-30-year range issuance less than most had expected. What’s more, Treasury’s projection that it will slow the recent flood of new long-dated debt, contributed to a rally in the bond market and a pullback in long-term yields.

The U.S. economic calendar was packed this week with a mix of key data, central bank meetings and even Treasury auction announcements. To start things off, the Treasury announced its financing requirements for the upcoming quarter. In the announcement, issuance is dominated by shorter dated securities (2-7 year), with planned 10-to-30-year range issuance less than most had expected. What’s more, Treasury’s projection that it will slow the recent flood of new long-dated debt, contributed to a rally in the bond market and a pullback in long-term yields.

The next key focus was the labor market, with varying reports giving snapshots of the state of this important sector. November’s nonfarm payrolls, the most important, showed that hiring in the U.S. economy has slowed. Additionally, the pace of wage growth has cooled (Chart 1) in financial news. The unemployment rate also edged up slightly, bucking expectations for no change. The job opening and labor turnover survey (JOLTS) was slightly backward looking, covering September, and showed an increase in job openings, which was offset by a rise in the number unemployed, leaving the ratio of the two largely unchanged at 1.5. The pace of hiring also eased and the quit rate levelled off at its pre-pandemic rate. The employment cost index on the other hand showed that wage gains ticked up in the third quarter, but compensation growth still slowed from 4.5% to 4.3% on a year-on-year basis. Overall, the labor market metrics are consistent with what the Fed wants to see – a market that is slowly cooling with likely further deceleration in wage pressures ahead.

As widely expected, the Federal Reserve held interest rates steady at 5.25%-5.50% on Wednesday. This is the first time in the current tightening cycle that the Fed has paused for two consecutive meetings. However, the central bank still left the door wide open to potentially raising rates in the future if needed to keep the disinflation momentum going. October’s cooling in the labor market combined with expectations that economic activity will pullback in Q4, suggests that they may not need to walk through it before the year is done, but only time (and the data) will tell.

One sector of the economy that is not fairing very well is the manufacturing sector. Activity in the sector, as measured by the ISM sentiment survey, continued to contract in October, falling to its lowest level since July, on broad-based weakness. The silver lining, however, is that a pullback in raw materials prices is easing cost pressures, which should help to mitigate price pressures for consumer goods. The services side of the economy fared a bit better, with the ISM services index expanding again in October, though at a slower pace (Chart 2). Twelve out of eighteen industries reported growth; however, the softer-than-expected reading suggests that the Fed’s hiking campaign is influencing the services sector as well.

One sector of the economy that is not fairing very well is the manufacturing sector. Activity in the sector, as measured by the ISM sentiment survey, continued to contract in October, falling to its lowest level since July, on broad-based weakness. The silver lining, however, is that a pullback in raw materials prices is easing cost pressures, which should help to mitigate price pressures for consumer goods. The services side of the economy fared a bit better, with the ISM services index expanding again in October, though at a slower pace (Chart 2). Twelve out of eighteen industries reported growth; however, the softer-than-expected reading suggests that the Fed’s hiking campaign is influencing the services sector as well.

The takeaway from the week is that if the disinflationary trend remains intact, the Fed’s December decision is a tougher call. There will be several economic releases over the next six weeks that will influence the Fed’s decision. But, so far, consumer spending momentum has remained stronger than expected, risking an uptick in inflation. This still suggests that the Fed’s work is likely not done.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.