Financial News Highlights

- The 10-year Treasury yield briefly surpassed 5% earlier this week in financial news. Though yields have since retraced, the 10-year looks to end the week at a still elevated 4.85%.

- The advance estimate of GDP showed the economy registered its strongest gain in nearly two years in the third quarter, with most major areas of spending recording gains.

- The FOMC is expected to hold rates steady next week, but the uptick in September inflation along with any signs of continued labor market strength in next week’s data will tilt the scales in favor of another rate hike later this year.

Economic Resilience on Full Display in Third Quarter

Longer-term Treasury yields continued to creep higher through the early portion of the week, as the looming threat of a mid-November government shutdown, increased Treasury issuance, and heightened geopolitical tensions remain key drivers pressuring the term-premia higher. After briefly surpassing 5% earlier this week, the 10-Year Treasury yield has since pared its gains and currently sits at a still elevated 4.85%. Meanwhile, equities edged lower for the second straight week – down 2% at the time of writing – but remain 8% higher on the year.

Longer-term Treasury yields continued to creep higher through the early portion of the week, as the looming threat of a mid-November government shutdown, increased Treasury issuance, and heightened geopolitical tensions remain key drivers pressuring the term-premia higher. After briefly surpassing 5% earlier this week, the 10-Year Treasury yield has since pared its gains and currently sits at a still elevated 4.85%. Meanwhile, equities edged lower for the second straight week – down 2% at the time of writing – but remain 8% higher on the year.

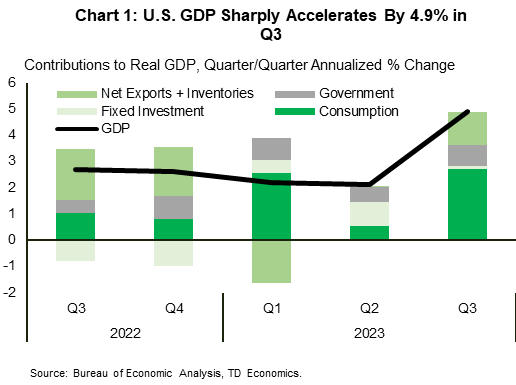

Turning to the economic data calendar, the Bureau of Economic Analysis (BEA) released its advance estimate of third quarter real GDP. The report showed economic activity accelerating at more than double the rate of expansion seen in Q2. The ongoing theme of economic resilience was on full display last quarter, with most major areas of spending recording gains in financial news. The strength in consumer spending was particularly eye-catching, jumping up 4.0% (Chart 1). The summer shopping spree was fueled by a resilient labor market and a further drawdown of the excess savings accumulated during the pandemic. Moreover, because many homeowners locked-in mortgages at ultra-low rates in 2020/21, the passthrough of higher interest rates to the consumer has been more muted relative to past tightening cycles.

Perhaps more concerning for policymakers is that spending momentum heated up at the end of the third quarter. September’s gain was the second strongest over the past eight months, and suggests consumers didn’t hold back last month, despite the looming headwind of student loan repayments restarting in October. At this point, we see Q3’s blowout numbers as the ‘last hurrah’ and expect a more tepid pace of consumer spending (1.5-2%) for Q4, before slipping sub-1% through the first half of next year.

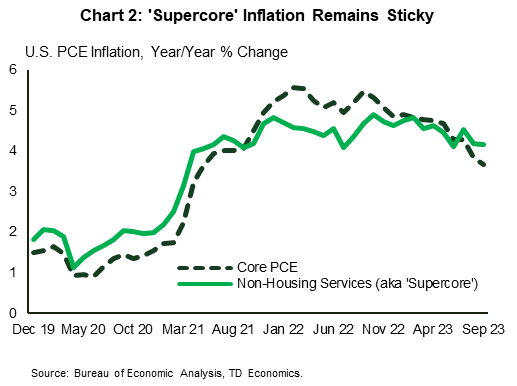

Should the consumer prove more resilient, that will spell trouble on the inflation front. In fact, core PCE inflation data for September has already telegraphed some evidence of progress stalling. Price growth picked up to 0.3% m/m (up from the 0.17% m/m gains averaged over the three prior months), with notable strength in Powell’s ‘supercore’ measure, which has barely budged from last year’s highs (Chart 2).

Should the consumer prove more resilient, that will spell trouble on the inflation front. In fact, core PCE inflation data for September has already telegraphed some evidence of progress stalling. Price growth picked up to 0.3% m/m (up from the 0.17% m/m gains averaged over the three prior months), with notable strength in Powell’s ‘supercore’ measure, which has barely budged from last year’s highs (Chart 2).

From the Fed’s perspective, nothing out this week will influence next week’s interest rate decision. At this point, markets are fully priced for the FOMC to hold rates steady, and only attach a 20% probability to another rate hike in December. However, that could quickly change over the next week should the FOMC statement and/or Powell’s press conference strike a more hawkish tone. Next week’s Employment Cost Index release for the third quarter is also important given it contains a measure of wage inflation that the Fed watches closely. As well, October’s employment figures out Friday will be closely scrutinized as usual. Unless these reports show a definitive sign that the labor market is cooling, which looks unlikely given the recent strength in higher frequency indictors including jobless claims and Indeed job posting data, another rate hike come December seems inevitable.

Thomas Feltmate, Director | 416- 944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.