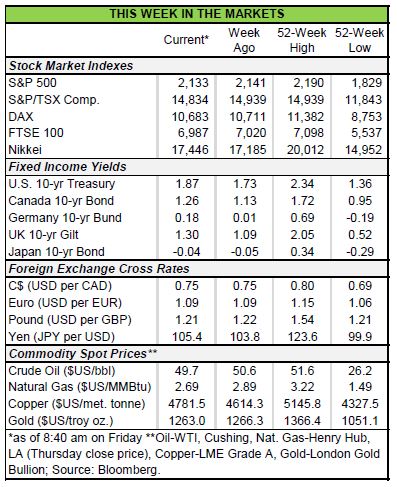

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The odds of a rate increase in December have continued to climb higher this week, rising to about 75%

from 67.5% a week ago and 54% last month. - Expectations were buoyed by hawkish Fedspeak and solid domestic data. Following declines in the prior

month, sales of new single-family homes and pending home sales both surprised to the upside in September.

Housing prices also continued to grow briskly in August, advancing by 5.3% y/y. - U.S. GDP was the key data release of the week. Based on the advance estimate, the U.S. economic

momentum accelerated markedly in Q3, with GDP rising by a healthy 2.9% (SAAR). - With near-term market expectations for monetary policy converging to those of the Fed and the economic

data remaining supportive, the FOMC will likely use next week’s statement to communicate its intentions

to raise rate in December.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

MARKETS AND FED NO LONGER AT ODDS

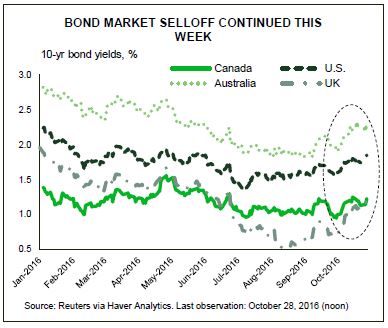

U.S. monetary policy was top of mind for investors this week in anticipation of next week’s FOMC meeting. Buoyed by hawkish Fedspeak and solid domestic data, the odds of a rate increase in December have climbed to 75% this morning – well above the near-even odds just a few weeks ago. Rising expectations that the Fed will move off the sidelines this year continued to support the U.S. dollar, which is trading near its highest level since January. Meanwhile, bonds continued to sell off, pushing yields higher, with yields on the 10-year Treasury note rising by 11 basis points this week.

Investors were treated to several Fed speeches early this week, ahead of the blackout period that began on Wednesday afternoon. Fed officials largely maintained the slightly hawkish bias, with Charles Evans (Chicago) noting that he expected the Fed to hike three times by the end of next year. St. Louis Fed President, James Bullard, also indicated that December was the “most likely” option for a rate increase.

In additional to this upbeat rhetoric, domestic data also remained encouraging this week. Following declines in the prior month, sales of new single-family homes and the index of pending home sales both surprised to the upside in September. While sales of new homes can be volatile on a month-to-month basis, they have been on an upward trend this year and 30% higher than last year. The newly-built market has been benefiting from the limited inventory of existing houses, prompting potential home buyers to visit homebuilder showrooms. A limited inventory of houses on the market has also kept the pressure on existing home prices. They continued to grow briskly in August, advancing by 5.3% y/y – a slight acceleration from 5.1% y/y pace seen a month prior. Home prices are now within a hair of a full recovery and are helping rebuild household wealth – having accounted for nearly half of the total increase in household assets over the past year.

While the gains in the above indicators were encouraging, the most eagerly awaited data release this week was the first look at third quarter U.S. GDP. The headline print did not disappoint. Following the sluggish near-1% growth that prevailed in the first half of the year, the U.S. economic momentum accelerated markedly in the third quarter with GDP rising by a healthy 2.9% (SAAR), beating the median consensus estimate of 2.6%. Consumer spending also remained resilient. While decelerating to 2.1%, the slowdown comes atop of an unsustainably strong 4.3% gain the prior quarter. The headline GDP print was also boosted by a positive contribution from non-residential investment, inventories, and international trade – all of which weighed on growth over prior quarters. We expect both non-residential and inventory investment to remain supportive in the coming quarters, underpinned by reduced drag from the oil sector and the rebuilding of inventories that were previously drawn down. Residential investment, which has disappointed in recent quarters, is also expected to turn from a headwind to a tailwind as rising prices and a limited inventory of houses on the market boosts construction. Meanwhile, the strength in net exports – which added an outsized 0.8pp to the headline number – is unlikely to persist. The gain in exports was driven by a large one-time boost from soybean exports. Moreover, U.S. economic outperformance and diverging monetary policy continue to pressure the dollar higher (for more detail see our recent Dollars & Sense).

All in all, with near-term market expectations for monetary policy converging to those of the Federal Reserve and the economic data remaining supportive, the door for a rate hike this year remains wide open. While a move next week remains a distant possibility, given the proximity to the presidential election, the Fed will likely use next week’s statement to communicate its intentions to seal the deal in December.

Ksenia Bushmeneva, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.