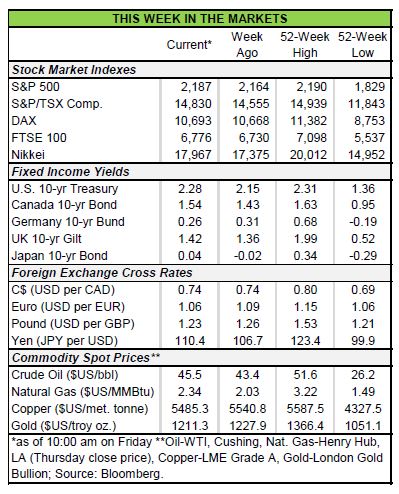

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The Trumpflation trade continued this week with emerging markets and bonds selling off, as money piled

into U.S. equities. - The U.S. dollar remained well supported this week, with domestic economic data telegraphing strength

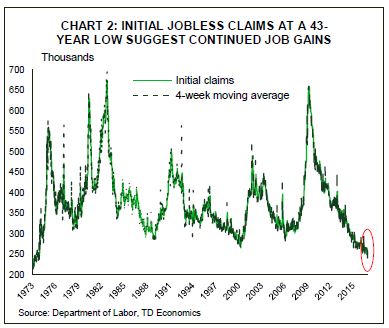

while comments by Fed officials suggested a rate hike looks imminent. - Highlights of the data-heavy week included housing starts rising to a nine-year high, initial jobless claims

falling to a 43-year low and retail sales notching up the strongest two months in just as many years. - Core inflation moderated to 2.1% in October from 2.2% in September, while headline ticked up to 1.6%

as past drag from energy prices continued to dissipate.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

DECEMBER RATE HIKE LOOKS TO BE IN THE BAG

The reflation (or Trumpflation) trade continued unabated this week. Investors continued to pull money out of emerging markets, which were expected to fare poorly in light of the President-elect’s anticipated trade policies. Treasuries too continued sell-off on rising inflation expectations as investors positioned themselves for pro-growth policies in the U.S. as well as anticipation of higher supply of debt related to unfunded fiscal stimulus. The 10-year Treasury bond yielded nearly 2.3% this morning, while the 30-year bond yield neared 3% – 40 basis points from pre-election levels.

Emerging market currencies have taken the brunt of the sell-off. The Mexican peso is down more than 20% from last year with half of the decline taking place since the election. Fears of rising inflation led the Bank of Mexico to raise rates by 50 basis points yesterday – its fourth move this year – to the highest level since 2009. Still, the Bank expects that inflation will notch above its 3% target next year while growth could slow given the “the new international environment.”

The Chinese currency also remained under pressure in recent days as capital outflows intensified. The People’s Bank of China allowed the yuan to depreciate by way of its daily fix by nearly 2% to the U.S. dollar from early-November –a record eleven consecutive days of declines. The weaker renminbi-dollar fix prevented the yuan from appreciating vis-à-vis its other trading partners, and potentially denting already slowing growth.

The U.S. dollar strength, which, last week was more related to anticipated changes in policy, was this week, supported by strong domestic economic data and Fed comments. On the data front, homebuilding activity surged to a nine-year high, and while partly related to Hurricane-related weakness in the prior month, it nonetheless painted a picture of strengthening residential

Despite core inflation moderating to 2.1% in October from 2.2% the previous month, the headline measure ticked up to 1.6% as drag from energy prices dissipates. While this remains below the Fed’s 2% target, the Fed appears increasingly comfortable that it will rise to target over the medium term. The Fed also is appears hesitant to further delay the rate hike, with Chair Yellen suggesting in her Congressional Testimony this week that such a move risks having to raise it faster thereafter and encouraging excessive risk taking. A December hike appears to be in the bag.

Michael Dolega, Director & Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.