Financial News Highlights

- Financial markets remained eerily positive this week, despite the debt ceiling X-date looming with no bipartisan deal in sight.

- Retail sales data for April showed the continued resilience of the U.S. consumer, while housing starts are looking to have reached a bottom after having fallen 24% last year. Home sales were lower in April, and likely have a bit further to fall.

- Fed speakers diverged this week on the near-term trajectory of the fed funds rate. Financial markets are still pricing 50 bps of rate cuts by year-end.

Optimistic Markets Cheer the Small Wins

Risk sentiment remained eerily positive across global financial markets this week, despite the clock ticking down on the debt ceiling X-date (see report) in financial news. But instead of losing the forest for the trees, investors seemed to cheer the incremental progress made this week. President Biden and Speaker McCarthy, and their negotiators, met on Tuesday for a closed-door meeting, where there appears to be some common ground on several items including clawing back unspent pandemic relief funds, speeding up permitting of domestic energy projects, and applying stricter work requirements for some social safety net programs. However, the two parties remain deeply divided on the size of broader spending cuts. At the time of writing, equity markets are looking to end the week up 2%, while the 10-year Treasury is up 25 bps to 3.71%.

Risk sentiment remained eerily positive across global financial markets this week, despite the clock ticking down on the debt ceiling X-date (see report) in financial news. But instead of losing the forest for the trees, investors seemed to cheer the incremental progress made this week. President Biden and Speaker McCarthy, and their negotiators, met on Tuesday for a closed-door meeting, where there appears to be some common ground on several items including clawing back unspent pandemic relief funds, speeding up permitting of domestic energy projects, and applying stricter work requirements for some social safety net programs. However, the two parties remain deeply divided on the size of broader spending cuts. At the time of writing, equity markets are looking to end the week up 2%, while the 10-year Treasury is up 25 bps to 3.71%.

Turning to the economic data, retail sales data painted a picture of a still resilient consumer in April. Although headline retail sales (+0.4% m/m) came in below expectations (+0.8% m/m), this was partially the result of a pullback in gasoline sales – largely a price- driven decline. The headline was also weighed down by weaker growth in motor vehicle sales, despite wholesale auto sales showing a healthy gain last month in financial news. After removing the volatile items, the control group – a more precise measure of consumer spending – rose by a healthy 0.7% m/m. This suggests continued momentum for Q2 consumer spending, with our current tracking around 1%-1.5%.

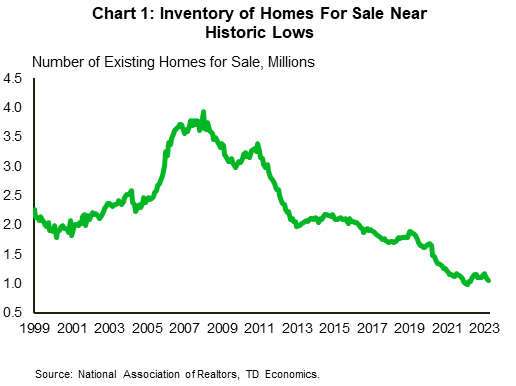

Data out this week on the housing market showed existing home sales fell by 3.4% m/m to 4.28 million units in April. The pullback comes after sales had shown signs of life earlier this year. However, much of that activity was the result of a pullback in mortgage rates that had occurred between October-January. Since then, mortgage rates have again turned higher, and at 7.1%, are not far off last year’s highs. Not only has this kept new homebuyers on the sidelines, but it has also discouraged move-up buyers from listing properties, which has kept inventory levels near historic lows (Chart 1).

Data out this week on the housing market showed existing home sales fell by 3.4% m/m to 4.28 million units in April. The pullback comes after sales had shown signs of life earlier this year. However, much of that activity was the result of a pullback in mortgage rates that had occurred between October-January. Since then, mortgage rates have again turned higher, and at 7.1%, are not far off last year’s highs. Not only has this kept new homebuyers on the sidelines, but it has also discouraged move-up buyers from listing properties, which has kept inventory levels near historic lows (Chart 1).

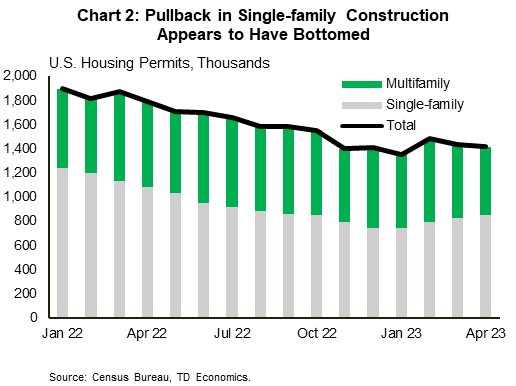

While home sales likely have a bit more room to fall, housing starts may have already reached a bottom. Residential construction rose 2.2% m/m to 1.4 million in April, with gains seen across both the multifamily (+3.2% m/m) and single-family (+1.6% m/m) segments. Permitting activity points to an uptick in construction in the single-family segment over the coming months, though this will likely be offset by some pullback in multifamily, which has yet to feel any correction through this tightening cycle (Chart 2).

Several Fed speakers this week showed a growing divergence among committee members on the near-term trajectory of the fed funds rate. While a few officials endorsed another rate hike, others are favoring a pause given the recent banking turmoil and the uncertainness it poses to the economic outlook. However, all officials still support rates remaining elevated through this year, which remains at odds with market pricing where 50 bps of cuts are still expected by year-end.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.