Financial News for the Week of June 17th, 2026

Financial News Highlights

- Tensions in the Middle East continued to escalate this week, pushing WTI prices back above $80 per-barrel.

- Inflation pressures cooled more than expected in June. Though the recent U-turn in oil prices raises concerns over the durability of the disinflationary dynamics.

- Retail sales remained decently strong in June, suggesting consumer spending regained some momentum in Q2 after stalling in Q1.

Cooler Inflation Quiets Calls for a July Hike

Despite a relatively busy week on the economic data calendar, market attention remained focused on renewed tensions in the Middle East. Earlier in the week, Iranian forces attacked multiple oil vessels transiting the Strait of Hormuz, prompting the U.S. to resume strikes on various military targets across Iran and reimpose its naval blockade. Tanker traffic through the vital passageway has again come to a halt, pushing WTI prices back above $80 per barrel.

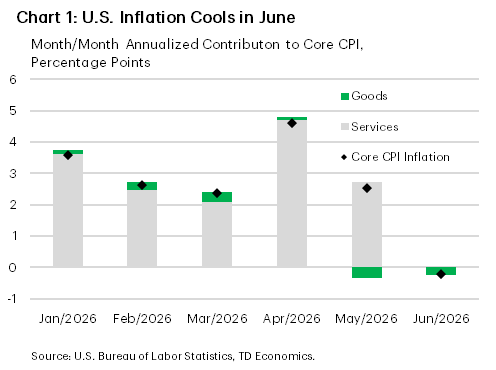

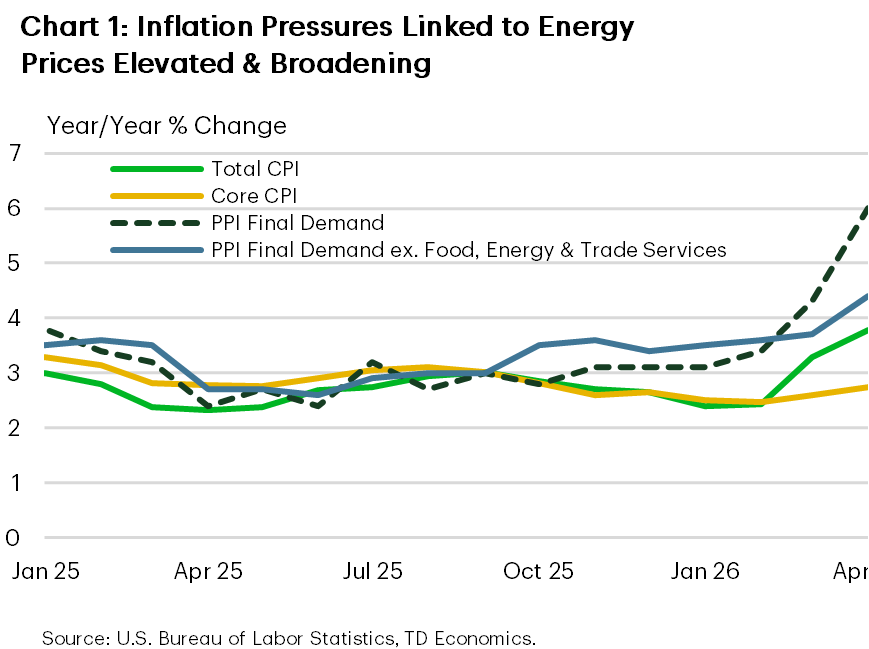

The renewed upward pressure on oil prices helped to temper the market response to an otherwise very encouraging inflation report. Headline CPI declined by 0.4% m/m in June – it’s first pullback since June 2024 and largest since April 2020 – pushing the 12-month change down to 3.5% (see commentary). A sharp drop in gasoline prices was largely responsible for last month’s decline, though even after removing these effects there were plenty of positive developments. Core inflation was flat for the month, as both goods and services were little changed (Chart 1). Importantly, many of the categories where tariffs had been adding to price pressures over the past year, including appliances, medical goods and apparel were all lower on the month – suggesting the worst of the tariff passthrough is now in the rearview mirror. Also encouraging was the fact that there was little evidence of higher energy prices bleeding into core inflation.

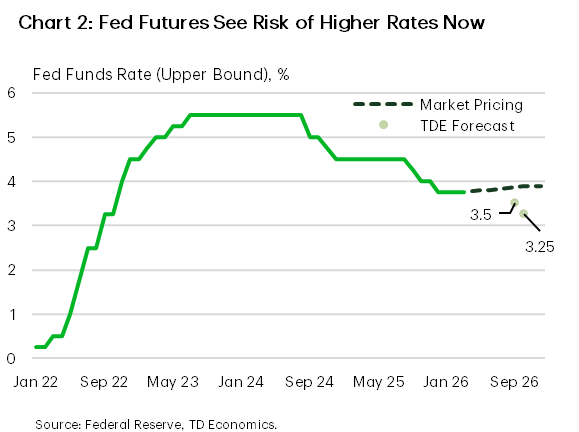

The disinflationary dynamics were further reinforced by a soft producer price index reading, which helped to remove speculation of a Fed rate hike later this month. That said, Fed futures are still priced for a little more than one rate hike by year-end, as the U-turn in oil prices is already raising concerns on the durability of the disinflationary dynamics.

Retail sales for the month of June provided further confirmation that households continue to shrug off the effects of higher energy prices (Chart 2). While the headline figure posted only a modest gain, that was partly related to a sharp drop in nominal sales at gasoline stations –owing to price effects (see commentary). Focusing on the control group, which removes volatile categories, it showed a much healthier gain in spending while revisions to the prior month were a bit higher. This reinforces the view that consumer spending regained some momentum in Q2, after sputtering in Q1. However, the spend dynamics remain K-shaped, with lower-and-middle income consumers increasingly price sensitive and hesitant to spend on discretionary items – something that was highlighted in this week’s Fed Beige Book.

Anyone hoping that Fed Chair Warsh would relent and provide some forward guidance during his first Congressional testimony this week was sorrily disappointed. Instead, Warsh restated the Committee’s unwavering commitment to return price stability, but provided no hints on the Fed’s next move. Several other policymakers spoke this week and perhaps the biggest takeaway is that while all were encouraged by last month’s softer inflation figures, one data point does not make a trend. Several more months of easing inflation will be required to convince officials that price pressures are moving in the right direction. If this were to occur, expectations for rate hikes should fade, leading to some downward pressure on yields.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of June 26th, 2026

Financial News Highlights

- Oil prices fell below $70/barrel, flirting with pre-conflict levels as the U.S. and Iran continue to negotiate towards a permanent resolution.

- The Federal Reserve’s preferred inflation metric, core PCE, rose 3.4% year-over-year in May.

- Personal income and spending both rebounded in price-adjusted terms in May, though households have increasingly relied on savings to support spending.

Oil Prices Retreat as AI Volatility Picks Up

The first week of summer was relatively quiet on the economic data front, with financial markets consumed by developments in the Middle East and evolving trends in AI. The latter proved to be a source of volatility in equity markets this week, as news of personnel changes at Alphabet led to a sell-off that spread to the broader AI ecosystem. This was partially reversed later in the week, but still highlights the inherent sensitivity of markets under the combined influence of elevated valuations and market concentration. The S&P 500 was down 1.8% while U.S. Treasury yields moved modestly lower on the week as of the time of writing.

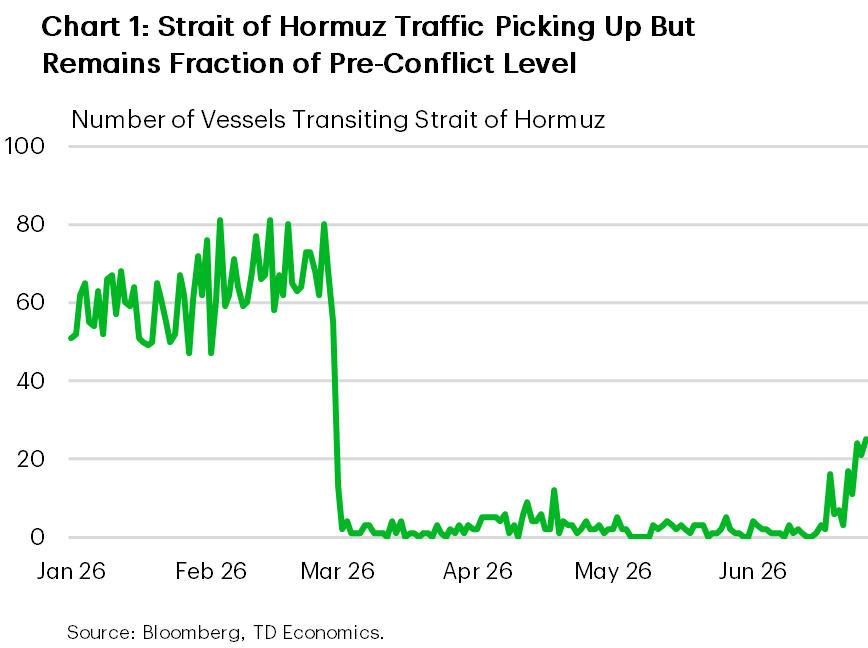

On the geopolitical front, negotiations between the U.S. and Iran continued after the two sides signed a 60-day memorandum of understanding (MOU) last week. The cessation of hostilities and reopening of the Strait of Hormuz have been enthusiastically welcomed by financial markers, with oil prices now back at their pre-conflict level. However, it bears repeating that the resumption of oil trade through the vital passageway is likely to be a gradual process as evidenced by the current level of maritime traffic through the strait (Chart 1). Combined with the possibility for roadblocks to be encountered during negotiations, risks related to oil prices remain skewed to the upside.

The feedthrough of higher energy prices to the economy was evident in the PCE inflation reading for May. Prices were 4.1% higher year-on-year (y/y) during the month, primarily driven by a 24% increase in energy prices. However, broader inflation pressures were also present, with core PCE inflation, which excludes food and energy products, rising 3.4% y/y. With energy prices having sharply reversed, some downward pressure on overall inflation is already in-tow. However, uncertainty around the magnitude and duration of energy-related second-order effects has given policymakers reason to adopt a more hawkish stance.

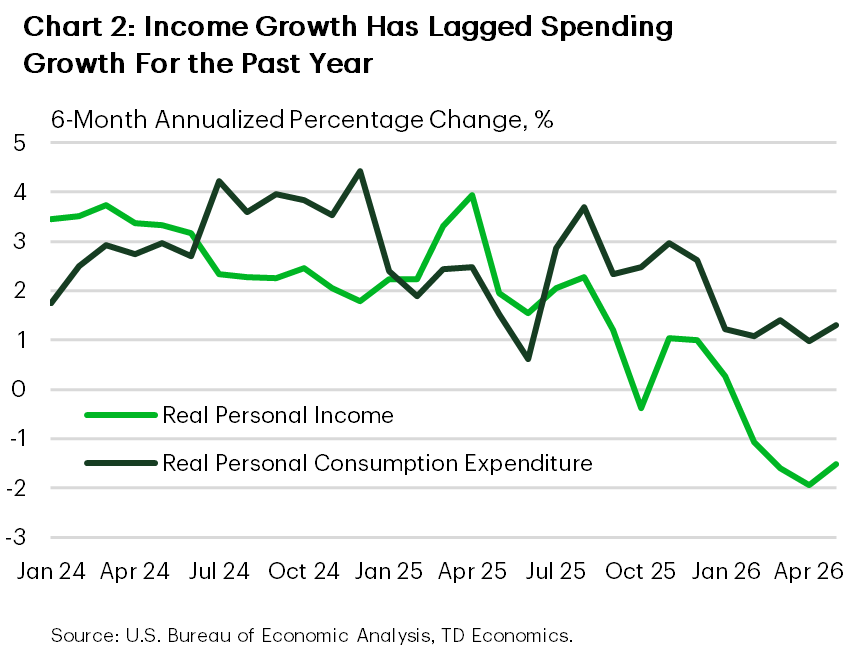

Personal income and spending both rebounded in real (price-adjusted) terms in May after softer readings in April, reflecting the sustained resilience of the American consumer. Still, much of the spending in recent months has been driven by a drawdown in savings, with the savings rate remaining at 3% in May – far below its historical average of 5-6%. While robust financial returns over the past few years may be offsetting the extent to which consumers need to save to meet their financial goals, the downward trend in the savings rate also began in mid-2025, coinciding with the introduction of broad tariffs and likely reflective of the multitude of cost pressures that have weighed on consumers over the past year (Chart 2).

Looking ahead to next week, the June employment data release on Thursday will be the highlight. Markets currently expect 118k new jobs to have been created during the month, marking a moderate deceleration relative to the strong reading in May. Fed Chair Warsh will also participate in a panel discussion next Wednesday, which will be watched closely for any signals on monetary policy decisions over the second half of the year.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of June 12th, 2026

Financial News Highlights

- The effects of the Iran war were evident in the CPI inflation report, which hit a three year high in May. Core inflation edged up to 2.9% y/y in line with consensus expectations.

- NFIB pricing indicators also moved higher in May and inflation concerns continued to rise, while hiring plans continued to soften.

- Existing home sales beat market expectations in May, but activity remains low compared to historical norms. Lacklustre markets are reflected in home price growth, which is still in the slow lane (1.3% y/y).

Price Pressures Now on the Front Foot

Middle East tensions spiked and then eased again this week, with President Trump threatening new strikes on Iran and then calling them off as he noted progress toward a deal. WTI oil prices, which had been holding near $90/barrel, fell sharply toward $85/barrel. The 10-year Treasury yield also dipped initially, reflecting hopes that a resolution to the conflict would limit the energy shock’s spillover into broader inflation expectations, but recovered some lost ground later in the week as investors digested another firm inflation report.

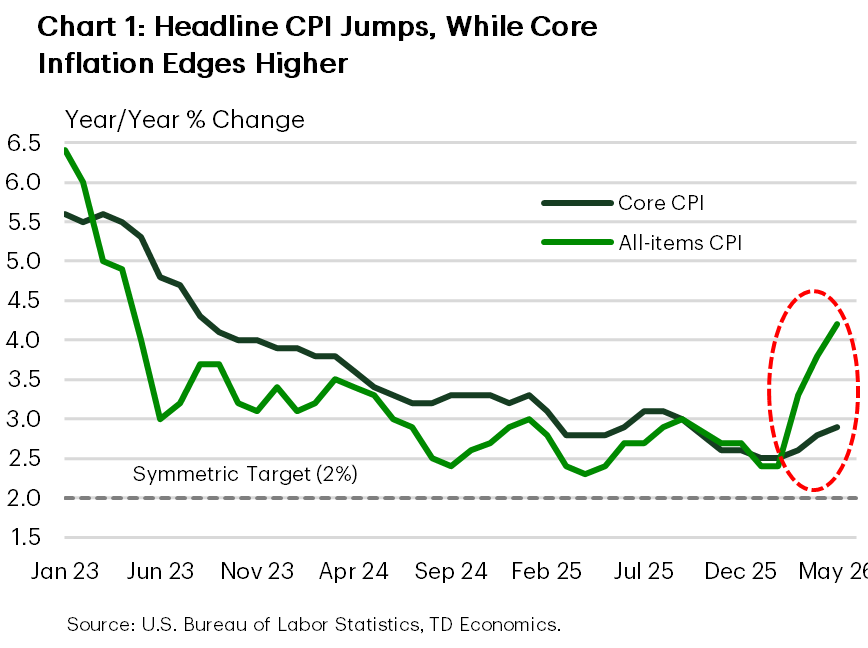

The May CPI report was the clearest evidence that inflation pressures continue to build. Headline inflation accelerated to the fastest pace in three years - 4.2% year-on-year (Chart 1). Higher energy costs accounted for the bulk of that increase. The gain in core inflation was more contained, but the annual rate still moved further above target (2.9% y/y), adding support to a “higher for longer” policy stance (see here). Sifting through the details, shelter cooled after April’s outsized gain and core goods prices slipped, but non-housing services remained firm.

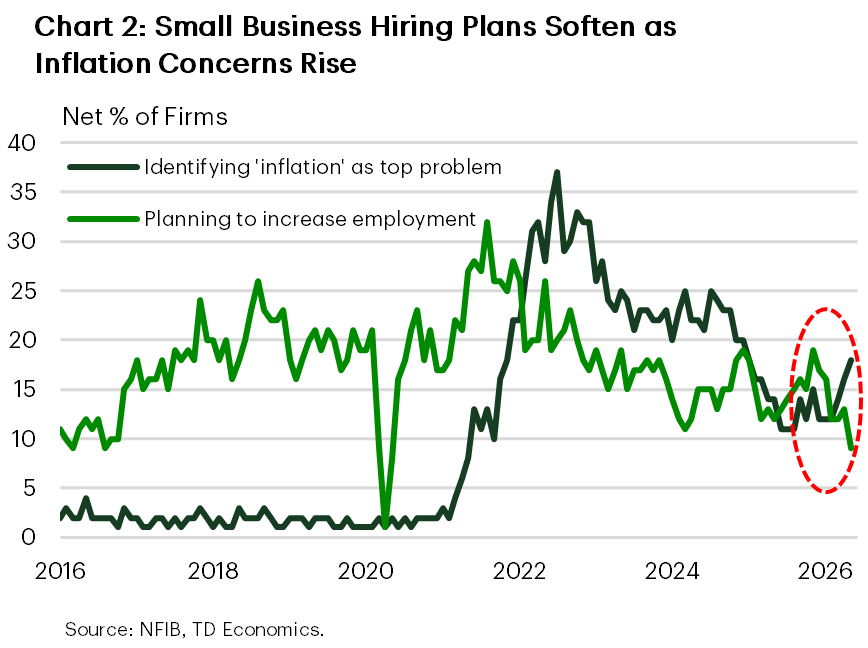

Inflation pressure was also evident in the NFIB small business survey, where a growing share of firms reported that they had raised average selling prices and that they planned further increases in the months ahead. This supports the view that higher energy and input costs are starting to ripple beyond the pump.

Housing offered a modest reprieve from the sour inflation news. Existing home sales rose a solid 3.2% in May to the highest level since December. Still, little has changed in the broader picture, with activity hovering near the 4-million mark for the third consecutive year and home price growth remaining in the slow lane.

Labor market signals, meanwhile, were mixed. Initial jobless claims ticked higher for the third week in a row but remained broadly range-bound, while continuing claims are still low by historical standards. Signals out of the small business survey, however, were less reassuring on this front. Small businesses are pointing to slower job creation ahead, with job openings and hiring plans softening recently amid an increase in inflation concerns (Chart 2).

All told, the effects of the Middle East conflict continue to show up in the data, and this is becoming harder for the Fed to ignore. Our view is that core inflation will likely remain elevated through year-end, supporting the case for an extended Fed pause. Next week marks Kevin Warsh’s first FOMC meeting as Chair. Markets will be watching not only for a clear rate signal, but also for clues on how he intends to communicate. Warsh has indicated a preference for a shift in communication strategy, like potentially not holding a press conference after every Fed meeting. We expect the committee to telegraph a “higher for longer” policy stance in its updated Summary of Economic Projections, which had reflected 25 bps of easing this year and next. It is also likely to drop its easing bias in the statement. This expected shift would move the Fed closer to market pricing, which now reflects a toss-up between “no action” and a 25-bps hike by year-end.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of May 29th, 2026

Financial News Highlights

- Renewed hopes of a U.S.-Iran ceasefire extension pushed WTI prices 9% lower this week to $88 per barrel.

- Consumer spending remained resilient in April, amid rising inflationary pressures and dwindling household savings.

- More Fed officials are joining the chorus of sounding increasingly hawkish, with Fed futures 60% priced for a rate hike by year-end.

Makings of a Deal

It’s been three months since the U.S. and Israel launched the initial attack on Iran. Hopes for a longer-term peace resolution rose this week following President Trump’s comments that a peace deal had been “largely negotiated”. Oil prices fell sharply on the news, though renewed attacks from both sides by mid-week briefly faded the optimism. But by Thursday evening, news outlines were reporting that the two sides had reached an agreement on a 60-day memorandum of understanding to extend the ceasefire, pending President Trump’s approval. Oil prices traded 9% lower on the week and the WTI benchmark currently sits at $88 per barrel. Meanwhile, economic data out this week reinforced a more cautious but still resilient consumer amid renewed inflationary pressures. The S&P 500 edged 1.3% higher on the week, while the 10-Year Treasury yield drifted lower by 12 basis points and currently sits at 4.44%.

This week’s release of the April personal income & spending data offered a fresh dose of reality on the pain being inflicted on American households because of the energy shock. PCE inflation rose to a three-year high of 3.8% year-on-year and is likely to push north of 4% in May alongside a continued rise in gasoline prices. The picture didn’t look much better once the effects of food & energy were removed, with core PCE inflation edging up to 3.3%. Three-and-six-month measures are even hotter, each up 3.8% (Chart 1).

Despite the rise in inflation, the consumer has remained reasonably resilient. Nominal spending rose 0.5% m/m in April, following a stronger gain of 1% in March. After accounting for inflation, April’s gain looked less stellar, but still edged higher by 0.1% m/m. Hotter inflation is also working to erode consumer purchasing power, with real disposable income declining for a third consecutive month. This has left households increasingly reliant on savings to fuel spending. But with the savings rate having slipped to a four-year low, the buffer is looking increasingly thin.

According to a recent survey conducted by the Conference Board, households are reporting softer spending intentions in the months ahead. Fewer households are planning to purchase big-ticket items while two-thirds of consumers plan to reduce overall spending due to higher prices. While the survey metrics have been a less reliable predictor of actual spending post-pandemic, we can’t completely disregard the signal. The energy shock has further strained affordability for lower-and-middle income households, who have not benefited to the same degree from past year’s gains in home and equity prices.

And there’s an increasing risk that affordability pressures could worsen if the energy shock is sustained much longer. A growing chorus of Fed officials are sounding increasingly hawkish amid rising inflationary pressures. Board member Lisa Cook said this week that if disinflation doesn’t soon resume, she would be “prepared to raise rates”. Meanwhile, Fed President Kashkari reiterated that the inflation fight takes priority as the labor market now appears to be in decent shape. This suggests next week’s employment report will play second fiddle to the May CPI numbers due on June 10th. Fed futures are now 60% priced for a rate hike by year-end, but a hotter inflation report could pull forward expectations for a rate hike.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of May 15th, 2026

Financial News Highlights

- Kevin Warsh takes the helm of the Federal Reserve after his nomination was confirmed by the Senate this week.

- Inflation spiked in April, with CPI up 3.8% year-on-year, as higher energy prices filtered through the economy.

- This in turn weighed on retail sales during the month, with real sales down 0.2% month-on-month.

Changing of the Guard

The changing of the guard at the Federal Reserve was formalized this week, as Kevin Warsh was confirmed by the Senate as Powell’s successor on Wednesday. This means Jerome Powell’s eight-year term as Chairman came to an end on Friday. Warsh takes the helm at a time when inflation pressures are rising sharply on the back of elevated global energy prices. Details on a potential resolution to the conflict in Iran remained elusive this week, which led to a 9% uptick in WTI oil prices. Equity markets were roughly unchanged on the week, with the S&P 500 rising 0.2%, as U.S. Treasury yields spiked by roughly 20 basis points, reflecting stronger inflation readings.

In terms of economic data releases, the inflation data for April was the biggest news item. Headline CPI hit a three-year high of 3.8% year-on-year (y/y), on the back of rising energy prices (Chart 1). Stripping out energy and food products, core CPI accelerated for a second consecutive month to 2.7% y/y, partly owing to the feedthrough of energy prices to categories like airline fares. Broad-based passthrough to non-energy categories was absent from the report, but with energy prices rising through early May, subsequent reports may be less benign, particularly if no resolution is reached over the near-term.

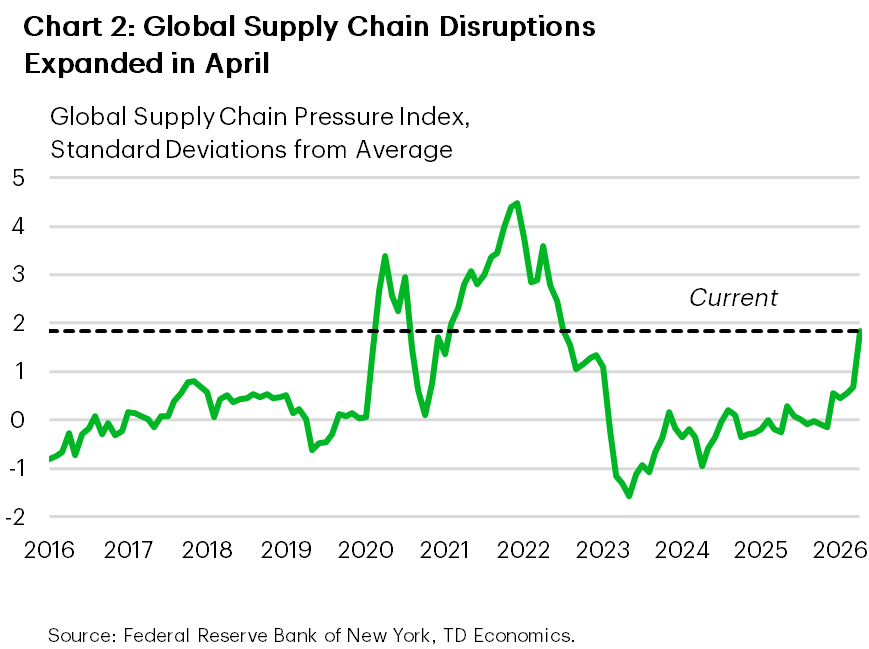

Upstream, the influence of higher energy prices was similarly evident for producers in April, with the Producer Price Index up 6% y/y. Selling price pressures have not been this elevated since late 2022, as global supply chain disruptions have begun to converge with those seen during the initial aftermath of the pandemic (Chart 2). The impacts of these developments on businesses, and the follow-through to consumers, will be monitored closely by the Federal Reserve.

To that end, the April retail sales report provided an early snapshot of consumer health. It showed a solid gain of 0.5% month-on-month in nominal terms, but after adjusting for inflation, sales fell 0.2%. This likely reflected, in part, the comparable contraction in real earnings during the month, which, if sustained, would continue to weigh on consumption going forward. A near-term resolution to the Iran conflict would help ease some of this pressure, although the effects would likely be gradual as supply disruptions take time to fully unwind. Taken together, these crosscurrents leave the near-term policy outlook highly dependent on incoming inflation data.

Against this backdrop, Fed officials in public remarks this week flagged concerns about the inflation reports. Several officials, including Chicago Fed President Goolsbee and Boston Fed President Collins, noted that tighter financial conditions may be required to quell emerging inflationary pressures. The balance of opinion among officials emphasized that a neutral stance would be appropriate over the near term to allow time to assess incoming data. As of the time of writing, financial market pricing for a rate hike by year-end has risen to 40%.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of May 8th, 2026

Financial News Highlights

- U.S. payroll growth was solid in April, defying market expectations, while the unemployment rate held steady at 4.3%.

- Historically lean jobless claims reaffirmed a muted environment for layoffs, while the ISM Services Index signaled continued expansion in the services side of the economy.

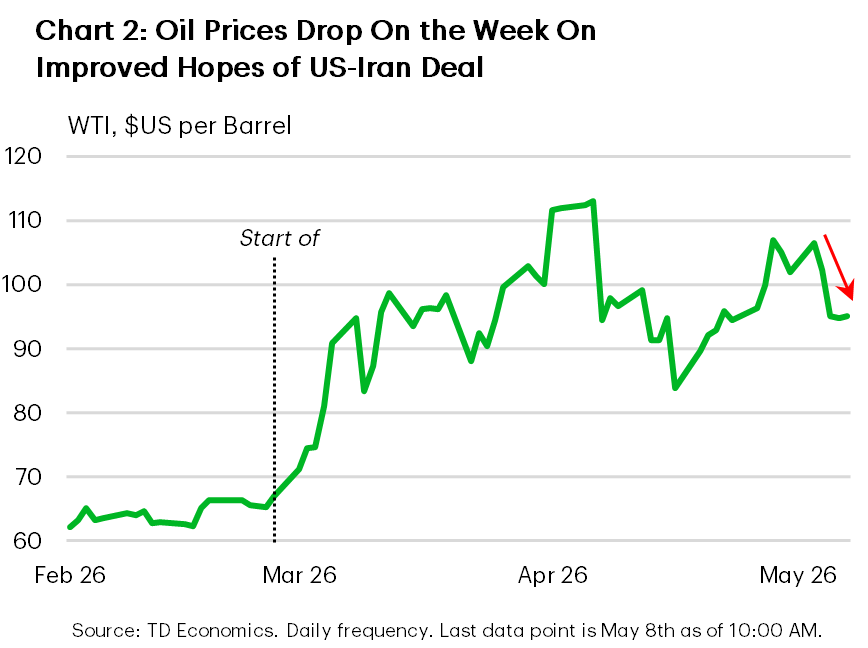

- Volatility in oil prices continued this week as WTI crude oil retreated from $105 per barrel to the mid-$90s later in the week on hopes of a breakthrough in U.S.-Iran negotiations.

Labor Market Resilient Despite Energy Shock

U.S. financial markets remained firm this week. The S&P 500 advanced roughly 2% to new record highs, supported by a pullback in oil prices and a better-than-expected jobs report. Long-term Treasury yields eased later in the week, with the 10-year note hovering near 4.35% – a hair below last week’s close. Market pricing continues to reflect limited expectations for near-term rate cuts amid ongoing energy market uncertainty and a relatively resilient economy.

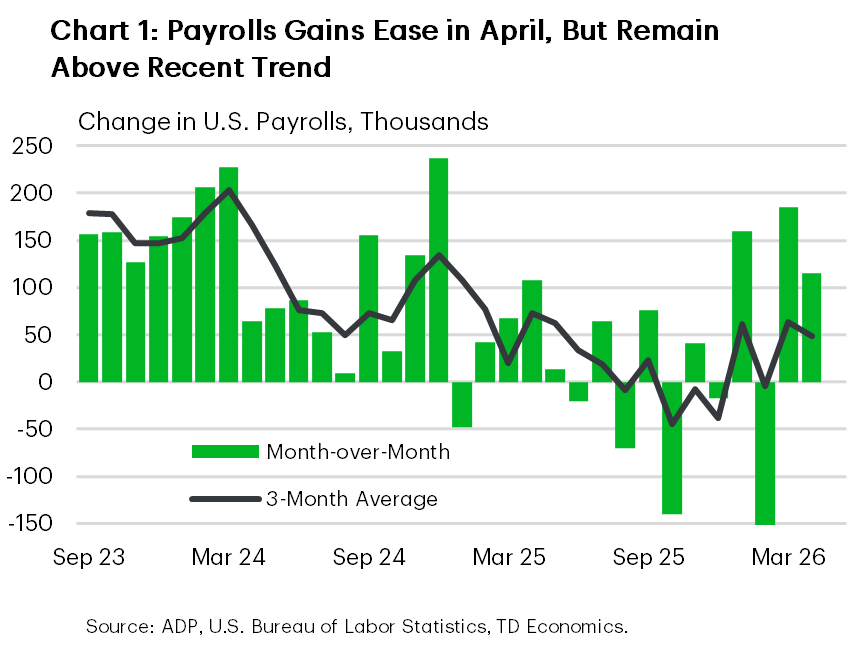

Resiliency was on display in the April jobs report, where nonfarm payrolls rose 115,000 – almost double the market consensus forecast. The unemployment rate held steady at 4.3% amid modest declines in both household employment and the labour force. Payrolls were volatile through the first quarter, due in part to factors like inclement weather and a healthcare strike in California. Looking through the volatility, it appears that job growth has picked up from its anemic trend at the end of last year and is now running at a decent pace that’s allowing it to hold the unemployment rate steady (Chart 1). High-frequency indicators reinforced this resilient labour market picture: initial jobless claims remained very low by historical standards, while continuing claims fell to 1.77 million – a new two-year low.

Other economic data lent further support to the resilience theme. The ISM Services Index eased modestly in April but remained comfortably above the 50-point expansion threshold. The details of the report, however, had a few blemishes. New orders recorded a notable pullback, while the prices-paid component remained elevated at 70.7 – the highest level since late 2022 and up notably from earlier this year – pointing to persistent cost pressures in the services sector.

With respect to prices, the good news is that the price of WTI crude oil, which had surged above $105/barrel late last week, fell back to the mid-$90s over the course of this week (Chart 2). This followed reports of U.S.–Iran negotiations and tentative de-escalation signals around the Strait of Hormuz. While constructive for inflation expectations, sustained disinflation will depend on a more durable resolution to the tensions

These developments are likely front-of-mind for Fed Chair-nominee Kevin Warsh as he prepares to take the helm. Communication from the Fed this week maintained a cautious stance, with New York Fed President John Williams emphasizing that policy is “well positioned” to balance the risks to the dual mandate. Under the current backdrop, market odds remain strongly in favor of no Fed action over the near term, with the probability that rates are held steady this year still sitting at over 70%. Ultimately, this morning’s better-than-expected jobs report, alongside other high-frequency indicators, helps ease concerns that the U.S. labour market has continued to deteriorate. This should give policymakers more breathing room to assess the extent to which higher energy prices filter into core inflation over the coming months.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of May 1st, 2026

Financial News Highlights

- Despite elevated uncertainty, the S&P 500 reached another all-time high this week, riding its best monthly performance in six years.

- The Federal Reserve held the policy rate steady while Chair Powell confirmed he will remain on the Board of Governors until the DOJ’s probe is completely resolved.

- The U.S. economy expanded by a healthy 2% in Q1, while inflationary pressures rose to a two-year high.

A Strait Shrug

U.S. equity markets shrugged off escalating U.S.-Iran tensions and instead focused on this week’s upbeat earnings releases and signs of a still resilient U.S. economy. Further gains in the S&P 500 capped off what has been an impressive run through the month of April, with the index rising +10% m/m – its strongest performance since April 2020. The gain in equities came despite the price of oil moving back above $100 per-barrel (WTI benchmark) on reports that President Trump told aides to prepare for an extended blockade. Meanwhile, Treasury yields across the curve climbed a bit higher, as hawkish undertones in the Fed’s policy statement erased hopes of rate cuts later this year. The 10-year Treasury yield currently sits at 4.38%, while Fed futures are now showing a one-in-three chance of a rate hike by April 2027.

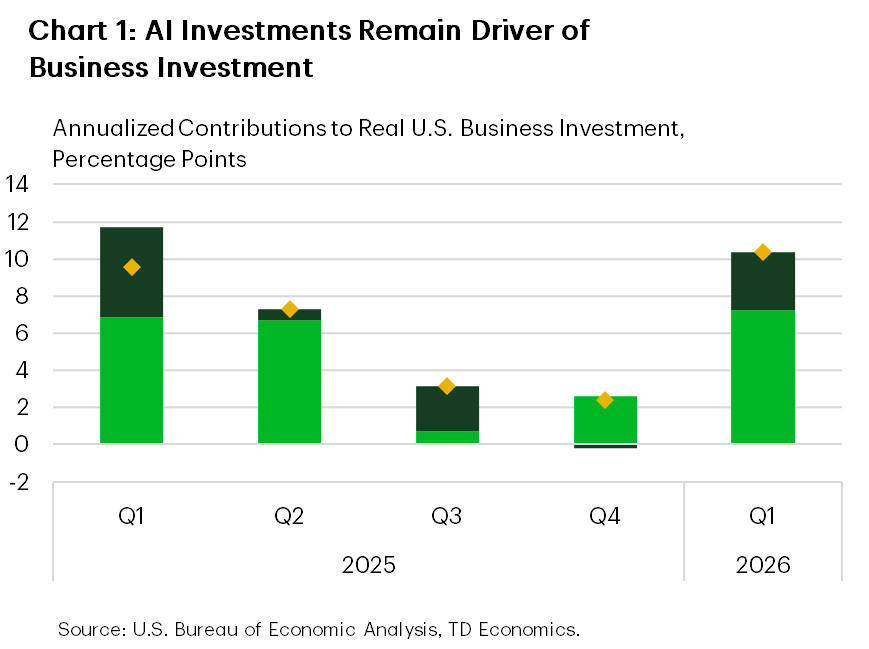

At the onset of the Middle East conflict, we argued that the economic impact from higher oil prices is likely to be relatively small. In large part, that was because of structural factors like the U.S. being less energy intensive and a net exporter of energy products. But we also noted that the shock was hitting the economy from a point of strength, and that was evident in this week’s reading of Q1 GDP. The economy expanded by a respectable 2%, with business investment remaining a bright spot. AI was a significant driver underpinning investment growth, though there was also evidence of some broadening to more traditional areas (Chart 1). The AI spending splurge looks to have legs, with Meta, Alphabet and Microsoft all raising guidance for 2026 planned expenditures this week. Cumulative capex by the “Magnificent 7” is now estimated to be $725 billion – a significant increase from 2025’s ~$375 billion.

Meanwhile, consumer spending was a soft spot in Q1, though some of the weakness appears transitory. The quarter got off to a rough start, as Winter Storm Fern caused major disruptions across most of the U.S. Encouragingly, the spending figures picked up as the quarter progressed, with March’s gain the strongest in fifteen months… in nominal terms. After adjusting for the sharp jump in inflation – partly due to the surge in energy prices – the gain appeared more modest. But it wasn’t only energy prices holding up inflation. Core PCE – the Fed’s preferred inflation gauge – rose 3.2% yr/yr in March, or its fastest rate of growth in over two years (Chart 2).

Rising inflationary pressures have made the FOMC more cautious on the rate outlook, with three Fed officials voting to remove the rate-cutting bias in the policy statement. The shifting sentiment comes at an interesting time for the Fed. This week’s press conference likely marked Powell’s last as chair, with Kevin Warsh expected to be in-seat for the next meeting following his nomination clearing the Senate Banking Committee earlier this week. But Powell noted at the press conference that he plans to stay on the board until the DOJ investigation is “truly over with transparency and finality”. Ultimately, this leaves the composition of the FOMC unchanged, as Warsh will fill the seat of President Trump’s appointee Stephen Miran, leaving little hope that the new Fed chair will be able to deliver on immediate rate cuts.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of April 24th, 2026

Financial News Highlights

- Iran signaled a reopening of the Strait of Hormuz amid a fragile ceasefire, easing oil prices and lifting markets, though evidence of a full normalization in shipping remained limited.

- Retail sales rose sharply in March, boosted by higher gasoline prices but also supported by solid underlying volumes, pointing to continued consumer resilience.

- Business surveys showed activity stabilizing even as war-related supply disruptions pushed price pressures higher, complicating the policy outlook.

Markets Jitter, Prices Bite

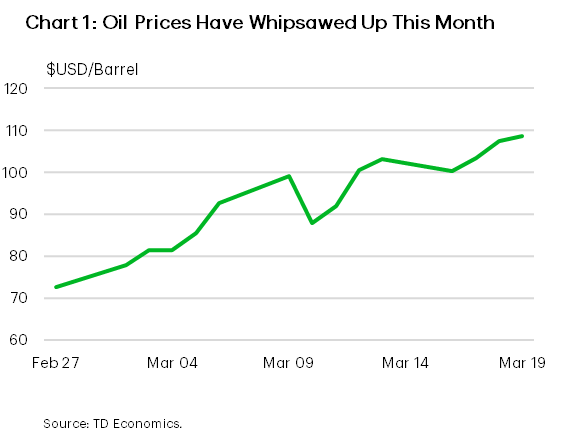

As the Iran conflict approaches the two month mark, financial markets remained highly sensitive to signals around energy supply risks. Early in the week, Iran announced that the Strait of Hormuz would be reopened to commercial shipping vessels during a newly brokered ceasefire, triggering a sharp pullback in oil prices and a relief rally in risk assets. WTI crude fell into the low $80s per barrel range, while U.S. equities moved to new highs as immediate worst case supply scenarios were priced out (Chart 1). That said, reporting around actual shipping flows suggested that conditions on the ground were uneven. As a result, while near term fears eased, geopolitical risks remain elevated and sentiment fragile, leaving markets vulnerable to renewed volatility should tensions re escalate.

U.S. economic data this week offered a reminder that domestic momentum has not yet broken down. Retail and food services sales rose 1.7% in March, driven largely by a surge in gasoline prices, but importantly, real (inflation adjusted) spending also increased a solid 0.8%. Core retail sales excluding gasoline, autos, and building materials posted broad-based gains, suggesting that households have not yet pulled back meaningfully on goods consumption. One area of softness was spending at restaurants, which was little changed on the month, highlighting some emerging price sensitivity among consumers.

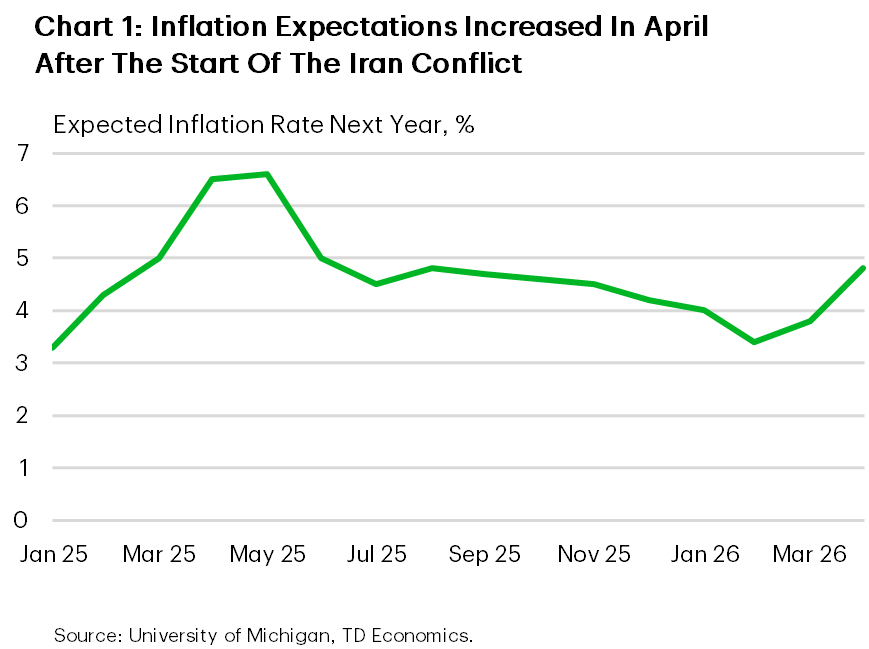

Forward-looking indicators painted a more mixed picture. The latest U.S. PMI readings showed business activity recovering modestly in April after stalling in March, with manufacturing rebounding more strongly than services. However, the rebound was accompanied by worsening delivery times and a sharp increase in input and output prices, reflecting ongoing supply disruptions tied to the conflict. Firms reported precautionary stock building and rising costs, reinforcing concerns that inflation pressures could re-intensify. The University of Michigan survey released today showed inflation expectations over the next year rising sharply, a key indicator energy-driven price worries are becoming more entrenched (Chart 2).

Markets are also increasingly focused on the Federal Reserve policy backdrop. Kevin Warsh’s confirmation hearing this week underscored uncertainty around the future policy framework, with investors parsing how shifts in leadership could influence the Fed’s reaction function at a time when inflation and growth risks are pulling in opposite directions. While Warsh’s confirmation by the Senate Banking Committee was uncertain amid the ongoing DOJ investigation of Chair Powell, headlines on Friday morning suggested the charges had been dropped. This clears a path for Warsh’s confirmation, which means next week’s interest rate announcement will likely be Jerome Powell’s last as chair. Looking ahead, next week’s data calendar is heavy, with personal income and PCE inflation, first quarter GDP, and ISM surveys all due. Together, these releases will help determine whether the economy is slowing enough to offset renewed price pressures.

Vikram Rai, Senior Economist | 416-923-1692

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of March 27th, 2026

Financial News Highlights

- Middle East tensions continue to drive market volatility, with energy prices remaining highly sensitive to tentative signs of de‑escalation.

- Markets have sharply repriced Fed expectations. Odds remain in favor of no Fed action this year, though odds of a hike have also picked up.

Middle East Conflict Keeps Volatility Elevated as Fed Signals Watchful Waiting

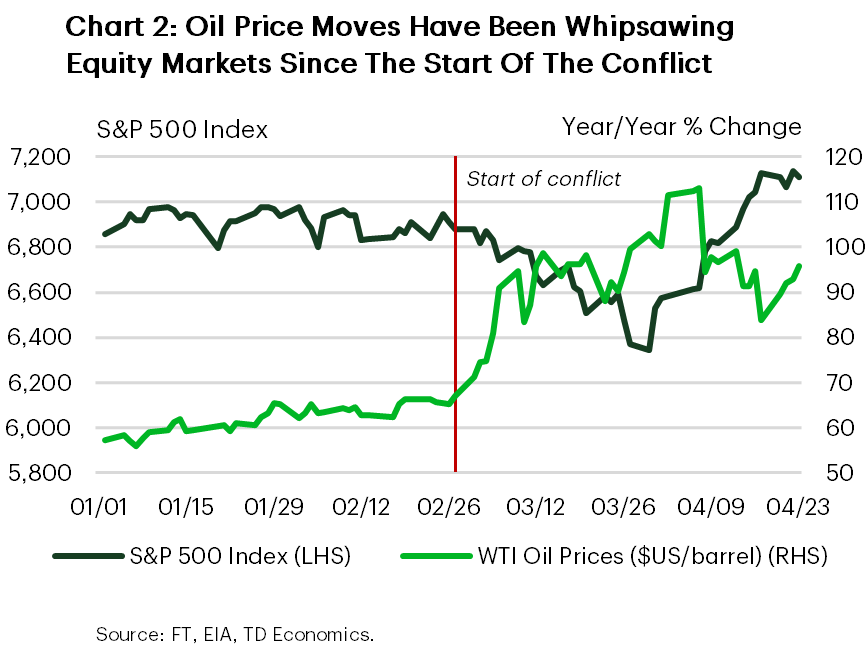

Financial markets remained focused on geopolitical developments in the Middle East this week, with little economic data to digest. Signs that tensions might ease – most notably President Trump’s decision to postpone strikes on Iran’s power plants – provided temporary relief to oil prices early in the week. Planned strikes have now been delayed for a second time, to April 6th. Additionally, President Trump’s trip to China has reportedly been rescheduled for mid-May, fueling speculation that the administration may seek to de-escalate the conflict and pivot back toward major trade negotiations. Despite tentative signs of optimism, the broader geopolitical backdrop remains highly volatile. Peace proposals from Washington and Tehran remain far apart, hostilities continue, and additional U.S. forces are moving into the region. Energy markets have remained acutely sensitive to these developments (Chart 1).

The conflict has exposed vulnerabilities in the global energy supply system, particularly across parts of Asia that rely heavily on Middle Eastern oil and shipping routes. Fuel rationing remains the exception rather than the rule thus far, so the immediate economic impact has come through higher energy prices. In the U.S., average gasoline prices are hovering near $4 per gallon, while diesel prices have moved above that mark.

Elevated energy prices have complicated the monetary policy backdrop. The Fed has left open the possibility of rate cuts later this year, but policymakers have become increasingly cautious amid renewed inflation risks tied to higher fuel costs and trade disruptions. Market pricing has pushed out rate cuts, and raised the odds of a rate hike (Chart 2). Importantly, this repricing reflects growing uncertainty around the inflation outlook, rather than explicit guidance from the Fed.

Recent communication from Fed officials reinforces this “watchful waiting” stance. Vice Chair Philip Jefferson noted that labor market conditions remain “roughly in balance”, yet he highlighted upside risks to inflation from the recent surge in energy prices and potential tariff pass-through effects. These have stalled disinflation and are likely to keep inflation above target over the near term. He affirmed support for the current policy stance, stating that it is well positioned to respond to evolving risks. Governor Lisa Cook echoed this measured tone, underscoring the need to monitor tail risks that could tighten financial conditions abruptly.

Looking ahead, the path of the conflict is highly uncertain. Against this backdrop, the Fed is likely to remain cautious, with recent communications suggesting that the path toward eventual easing has not been closed, but it is increasingly contingent on a sustained easing in inflation pressures. Next week features a heavy slate of data, including the first readings for March. The ISMs will be closely watched to see if the conflict has affected sentiment yet, while the jobs numbers will shed light on how “balanced” the labor market remained. The consensus is that both measures will remain fairly steady, but the details will be closely parsed.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of March 20th, 2026

Financial News Highlights

- Energy markets remain volatile as physical damage and data opacity deepen uncertainty around the Middle East conflict.

- The Fed held rates steady, emphasizing caution as higher oil prices complicate the inflation outlook.

- Softer housing data underscore growing sensitivity to higher yields and tighter financial conditions.

The Fed Pauses, Inflation Persists

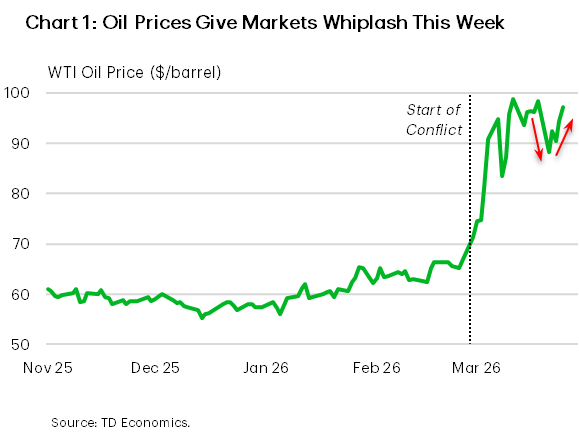

Financial markets remained on edge this week as the conflict in the Middle East escalated, with uncertainty expanding into physical energy supply rather than just shipping disruptions. Reports of damage to key oil and LNG facilities in the Gulf, including infrastructure that could take months—if not longer—to repair, have injected a persistent risk premium into energy markets. Oil prices have swung sharply day‑to‑day and remain well above pre‑conflict levels (Chart 1). This dynamic remains consistent with the base case in our Quarterly Economic Forecast, but risks of even higher prices are growing. Higher gasoline prices hurt consumer spending and the prolonged uncertainty raises downside risks in energy‑importing regions. We flagged these concerns this week in our State Economic Forecast, especially for states with higher exposure to transportation, manufacturing, and energy‑intensive industries.

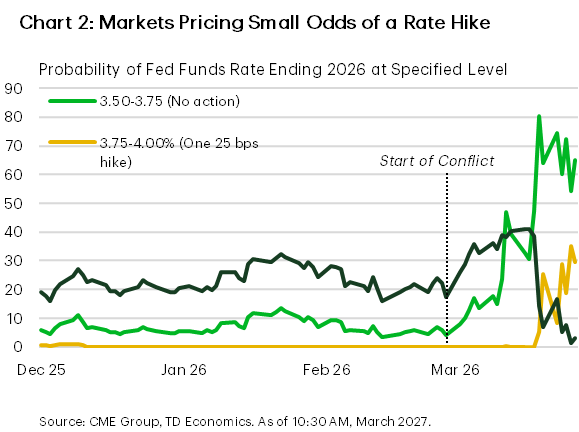

Against this backdrop, the Federal Reserve held its policy rate steady this week, as expected, but the statement was cautious. Chairman Powell acknowledged the heightened uncertainty stemming from the Middle East conflict, and revised projections showed higher inflation relative to December. The Fed continues to signal just one rate cut this year, reflecting concern that higher energy prices could slow the disinflation process at a time when core inflation is already proving sticky. Market reaction reinforced inflation concerns, with fed funds futures beginning to price a non‑trivial risk that the next move in rates may not be lower (Chart 2). Our commentary noted that the Fed appears intent on preserving flexibility, particularly given the risk that a prolonged energy shock could push the economy toward an uncomfortable mix of slower growth and firmer inflation.

Against this backdrop, markets continued to reprice risk this week in response to higher energy prices and a more cautious Federal Reserve. Equity markets struggled to find footing, while Treasury yields pushed higher as inflation risks moved back to the foreground. Incoming economic data offered a mixed picture. New home sales fell sharply in January, a reminder that interest‑rate‑sensitive sectors remain vulnerable to higher yields, though weather effects likely exaggerated the weakness. More broadly, the data flow reinforces that financial conditions are doing more of the near‑term adjustment work as the economy absorbs another external shock.

Looking ahead to next week, attention will undoubtedly remain on developments in the Middle East. Beyond the headlines, investors will also be watching how Fed officials are responding to the evolving situation and also the University of Michigan Consumer Sentiment Survey, a widely followed gauge of household confidence and inflation expectations. With energy prices and volatility high, these data could offer early signs of whether the current shock is beginning to weigh more materially on sentiment—or inflation expectations—an outcome that would further complicate the policy backdrop.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.