Financial News for the Week of December 12th, 2025

Financial News Highlights

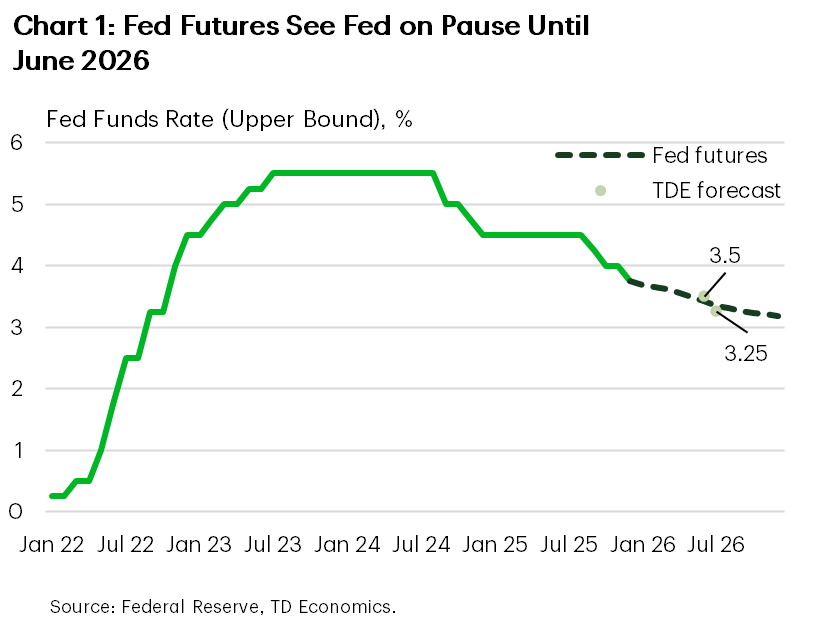

- The Federal Reserve delivered a third consecutive quarter-point rate cut this week, bringing the target range to 3.50%-3.75%.

- Three voters dissented on December’s decision and there was considerable dispersion on the expected rate path for 2026, underscoring the growing divide among FOMC members.

- The median FOMC projection on the federal funds rate suggests just one additional cut in 2026. For now, we think the Fed is on hold until June.

Fed Delivers on December Cut, But Signals Slower Pace Ahead

The main event this week was the Federal Reserve’s much anticipated interest rate announcement. While policymakers elected to push ahead with a third consecutive quarter-point rate cut – bringing the target range to 3.50%-3.75% – the move came amid an increasingly divided FOMC (Chart 1). Uncertainty over the extent and timing of future rate cuts didn’t stop the S&P 500 from briefly notching a new all-time high but pared those gains towards the end of the week. The yield curve steepened by roughly 10 bps, with the 10-year currently sitting at 4.19%.

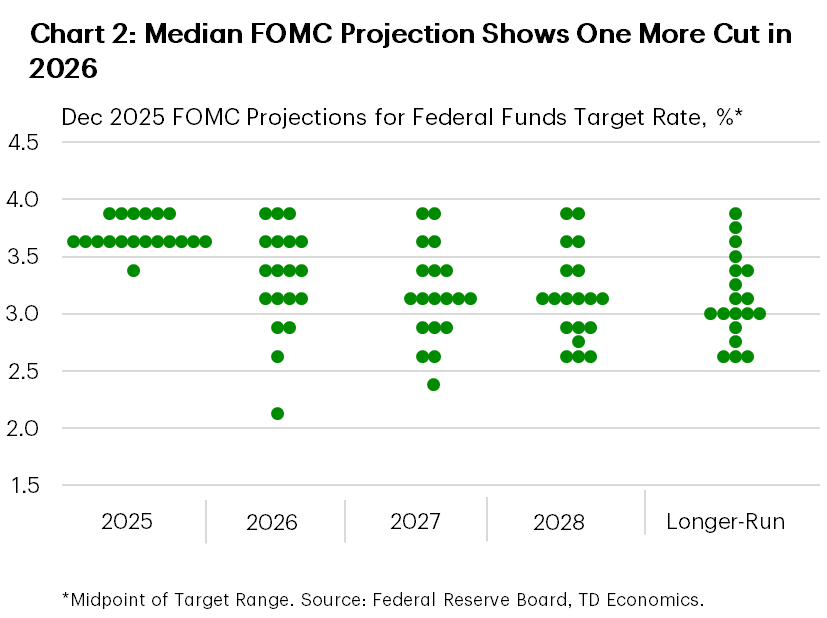

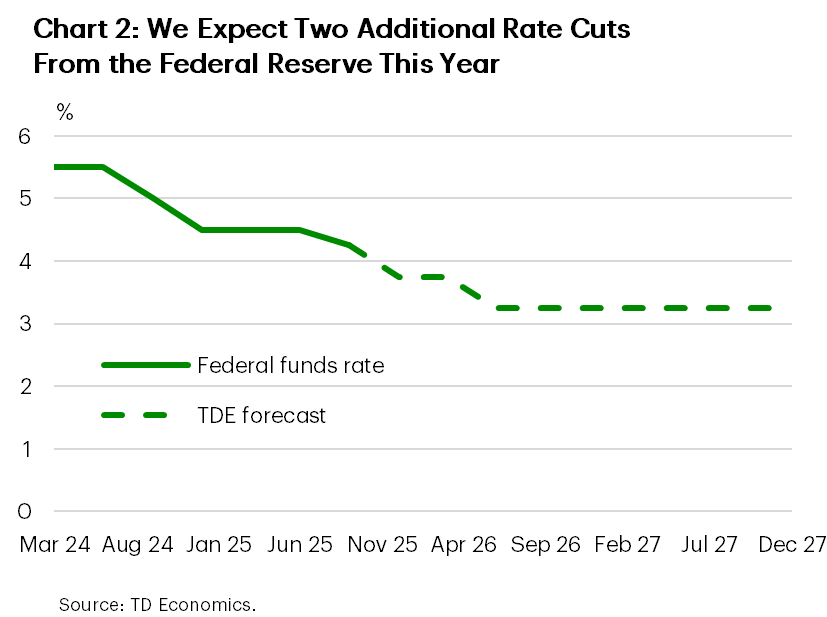

Accompanying the statement, the FOMC also released a revised set of economic forecasts, known as the Summary of Economic Projections (SEP). The SEP represents the median of the individual forecasts submitted by FOMC participant. Relative to the September projection, economic growth for 2025 saw a very modest upgrade (1.7% vs. 1.6%), while there was a notable upward revision to 2026 (2.3% vs. 1.8%). The expected trajectory for the unemployment rate was unchanged, while the inflation forecast is expected to remain above the 2% target through 2027 despite being nudged a tick lower in both 2025 and 2026. Importantly, the median projection on the federal funds rate remained unchanged at 3.6% for 2026 and 3.1% for 2027 – suggesting just one additional cut in each of the next two years (Chart 2). However, there was considerable dispersion across those projections, with the range of estimates for the appropriate level of the policy rate by the end of 2026 spanning 175 bps – a wider range than in September.

The growing divide among policymakers was further underscored by the fact that three participants dissented against December’s decision. Regional Fed Presidents Schmid and Goolsbee favored keeping the policy rate unchanged, while Governor Miran voted for a larger 50 bps cut. But as seen in Chart 2, there were a total of four Fed members who came into the meeting thinking a cut was not required.

The subtle shift in the dots wasn’t lost on market participants. Come January, the four regional presidents who are currently voting FOMC members (Goolsbee, Schmid, Collins, and Musalem) will be replaced by Paulson of Philadelphia, Hammack of Cleveland, Kashkari of Minneapolis and Logan of Dallas. While we don’t know for certain if any of the incoming Fed Presidents ‘quietly’ opposed the December cut, recent speeches by both Logan and Hammack have struck a more hawkish tone. Moreover, Kashkari had advocated for a pause on rate cuts ahead of the October meeting. This suggests that the hawkish tilt from Fed presidents isn’t going away despite the turnover in voting members.

However, this needs to be balanced against a new Fed Chair, who will be in seat May 2026, and is likely to have a more dovish policy stance. Moreover, should Chair Powell elect to not serve out the remaining two years of his term on the board of governors, it will create another vacancy for which President Trump can appoint a new board member. The takeaway from all this is that the division among FOMC members is only likely to deepen next year, putting in question both the timing and extent of further policy easing.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Your First 7 Financial Steps After Losing a Spouse

By Jason List, CFP®, CFA

Stepping into a new financial role after losing a spouse is one of life’s most tender and challenging transitions. If you’re navigating this season, know this: you are not alone, and countless others have effectively taken these same steps with the right support behind them. When we talk about financial steps after losing a spouse, we’re really talking about helping you regain clarity, stay organized, and feel confident that your financial goals are still feasible.

At Aventus Investment Advisors, we believe financial planning should be understandable and empowering. Our mission is to provide objective guidance, honor your values, and help you build a future that reflects both stability and purpose. This guide outlines the first 7 steps we recommend to widows as they begin shaping their next chapter.

1. Start With Breathing Room, Not Urgency

Very few financial decisions need to be made right away. In the early weeks and months, giving yourself permission to pause can be a tremendous gift. Clarity comes more easily when you’re not rushing.

Taking things step by step allows you to stay centered, ask thoughtful questions, and move forward with confidence. Your goal at this stage should be to create the mental space needed to see the road ahead more clearly.

2. Get Organized: Bringing the Financial Picture Into Focus

Once you’re ready, the next step is simply gathering information. That includes account statements, Social Security details, insurance policies, estate documents, and anything related to ongoing income or expenses.

Many widows are surprised by how empowering this process feels. Organization becomes your road map, helping you understand what you have, what needs updating, and which items require attention first. It’s also a chance to bring order to a part of life that may feel uncertain right now.

Clients often tell us that once everything is laid out in a clear checklist, they feel a sense of relief they didn’t anticipate. Understanding your financial picture opens the door to informed, confident decision-making.

3. Understand What Your Money Needs to Do for You Now

Your financial life serves your real life, including your home, your family, your daily needs, and the dreams that are still meaningful to you. Whether that means traveling more often, visiting friends and family, or simply keeping routines you cherish, thoughtful planning begins with understanding what matters most to you.

There is no fixed timeline for defining this next chapter. What’s important is aligning your finances around a life that feels fulfilling and sustainable. With the right guidance, this stage helps you shape a future that supports your well-being.

4. Map Out Cash Flow With Confidence

Cash flow is the anchor of financial stability. For widows, starting with a reasonable monthly income helps create predictability without pressure.

You don’t need to get it 100% right in the beginning. Few people do. The goal is balance: knowing what’s coming in, understanding what’s going out, and building enough flexibility to make changes with ease.

In our work supporting widows as they take financial steps after losing a spouse, we often see clients become noticeably more confident once their cash flow is organized and they can clearly see how their resources support both today and tomorrow.

5. Clarify Longer-Term Goals

It’s natural for long-term goals to shift after losing a spouse. Some clients want to simplify life. Others rediscover dreams they had set aside. Both paths are valid.

What matters is giving those goals space to form. What do you want the next 5, 10, or 20 years to look like? What experiences or opportunities would bring meaning to this stage of life?

At Aventus, our role is helping you translate those goals into a steady, manageable plan that aligns with your values and adapts as your needs evolve.

6. Build Your Trusted Support Team

A strong support team often makes the journey less overwhelming and far more empowering. Working with a fiduciary advisor who is legally committed to putting your interests first can help you feel more safe, understood, and supported.

Our approach at Aventus is grounded in clarity, education, and long-term partnership. We explain your options in a way that feels calm and manageable, not technical or intimidating.

Many widows tell us they appreciate having someone who can simplify complex topics and help them make decisions with confidence rather than uncertainty.

If you’d like to learn more about our philosophy and planning process, you can explore additional resources on our website: Aventus Investment Advisors.

7. Move Forward at Your Own Pace

Financial progress isn’t a race. Small financial steps after losing a spouse can create meaningful momentum. Over time, we’ve seen clients begin with uncertainty and grow into a place of clarity, steadiness, and optimism.

One widow we worked with shared that once she became organized and understood the possibilities in front of her, she felt empowered to take a dream trip she and her husband had always talked about. Moments like that are exactly why we do this work.

Your journey can move in that same direction: toward confidence, purpose, and a future that reflects who you are and where you want to go.

You Don’t Have to Do This Alone

Navigating financial steps after losing a spouse can feel daunting, but it can also be a powerful opportunity to build a financial life that supports your next chapter. You deserve clarity. You deserve confidence. And you deserve a world-class partner who puts your goals and values at the center of every decision.

At Aventus Investment Advisors, we’re here to help you feel organized, supported, and optimistic about what comes next. When you’re ready, we’ll walk with you, one clear and steady step at a time.

To schedule a meeting, call (704) 237-4207 or email jason.list@aventusadvisors.com.

Frequently Asked Questions

1. What are the most important financial steps after losing a spouse, and how soon should I start?

The first priority is to give yourself breathing room. In the early weeks, focus only on urgent items like notifying the Social Security Administration, locating insurance policies, and making sure essential bills are covered. Once you’re ready, you can begin the broader financial steps after losing a spouse, which typically include organizing accounts, reviewing cash flow, understanding survivor benefits, and updating estate documents.. Start when you feel steady, not because you feel rushed.

2. How do inherited IRA rules work for a surviving spouse, and can I combine them with other planning steps?

A surviving spouse generally has the most flexibility with inherited IRA options. In most cases, you can transfer the account into your own name to follow standard retirement withdrawal rules, delay required distributions until your own RMD age, or take distributions based on your needs. This can be coordinated with tax-aware planning and legacy goals. Working with a fiduciary advisor helps keep your inherited accounts aligned with the larger financial steps after losing a spouse, especially if you plan to reinvest, draw income, or update beneficiaries.

3. Which documents should I gather first to feel organized and confident about money decisions in the months ahead?

Start with the essentials: recent statements for bank, investment, and retirement accounts; insurance policies; estate plan documents (trust, will, POAs if applicable); mortgage and deed records; past tax returns; and survivor benefit paperwork. Many people find that creating a simple checklist is one of the most grounding financial steps after losing a spouse; it turns uncertainty into a manageable, step-by-step action plan. A fiduciary advisor at Aventus Investment Advisors can help you confirm nothing is missing and provide guidance on the right timing for each next decision.

About Jason

Jason List, CFP®, CFA, is a Senior Client Advisor with Aventus Investment Advisors in Cornelius, North Carolina. With nearly two decades of industry experience, he helps clients organize, grow, and preserve their wealth through comprehensive planning, investment management, and tax-focused strategies. Clients value his approachable style and the confidence that comes from having a fiduciary partner to navigate life’s milestones, whether retiring, traveling, or buying a new home.

Jason earned his undergraduate degree in mathematics from the University of North Carolina at Charlotte, a master’s in finance from Shanghai University of Finance and Economics, the CERTIFIED FINANCIAL PLANNER® designation in 2012, and the Chartered Financial Analyst® designation in 2024. He joined Aventus in 2021 after working at large financial institutions, drawn to the firm’s focus on personalized, transparent advice.

A Charlotte-area resident for more than 30 years, Jason lives with his wife, Ashley, and their beagle, Mindy. He enjoys traveling, hiking, bowling, and watching sports, and also serves as treasurer for a nonprofit that supports disenfranchised children in Kenya. To learn more about Jason, connect with him on LinkedIn.

Financial News for the Week of December 5th, 2025

Financial News Highlights

- Real consumer spending was flat in September, ending the third quarter on a soft note. Consumption for the third quarter was up 2.7% (q/q annualized).

- The Fed’s preferred inflation gauge – the core PCE deflator – rose by 0.2% month-on-month in September, as expected. That is still above the Fed’s target at 2.8% year-on-year, but down slightly from 2.9% in August.

- Combined with somewhat soft employment data in November’s ADP report, the Fed looks set to check off markets’ wish list for a rate cut next week.

President Trump Deals His Way Through Asia

Markets are convinced that the Fed will deliver an early holiday gift – a rate cut – next week. Odds of a December cut have hung near 90% ever since shifting up in late November, following support for more easing from Fed Presidents Williams (NY) and Daly (San Fran.). Economic data out this week, while mixed, did not perturb that balance. Equities managed to trek modestly higher, with S&P 500 up 1.1% from last week’s close.

September’s personal income and spending report provided a snapshot of spending and inflation trends before the government shutdown. Spending was flat in real terms in September, ending the third quarter on a soft note. Consumption for the quarter was up 2.7% (q/q annualized) – below expectations but still an improvement from 2.5% in the second quarter. September provides a soft handoff to the fourth quarter, which coupled with the government shutdown, slowing job growth, and weak consumer confidence, suggests spending will slow further at the end of the year. Early data from Thanksgiving weekend suggests holiday shopping was healthy but likely grew at a pace slightly below that of last year. Online sales continued to lead the way, with Cyber Week spending up nearly 8% year-over-year (y/y) according to Adobe. In-store gains were softer, with closely watched indicators pointing to growth in the low single-digits. AI tools helped boost retail site traffic, while a growing Buy-Now-Pay-Later (BNPL) trend also played an important role in propping up spending.

Core PCE inflation rose 0.2% month-over-month (m/m) in September, and 2.8% in y/y terms – a modest easing from 2.9% in the prior two months. The ISM services price index recorded a notable pullback in November – marking a modest positive post-shutdown signal with respect to inflationary pressures. Nonetheless, Cleveland Fed Inflation Nowcasting puts core PCE at 0.23% (m/m) for both October and November, 2.8% and 2.9% in y/y terms respectively – still well above target.

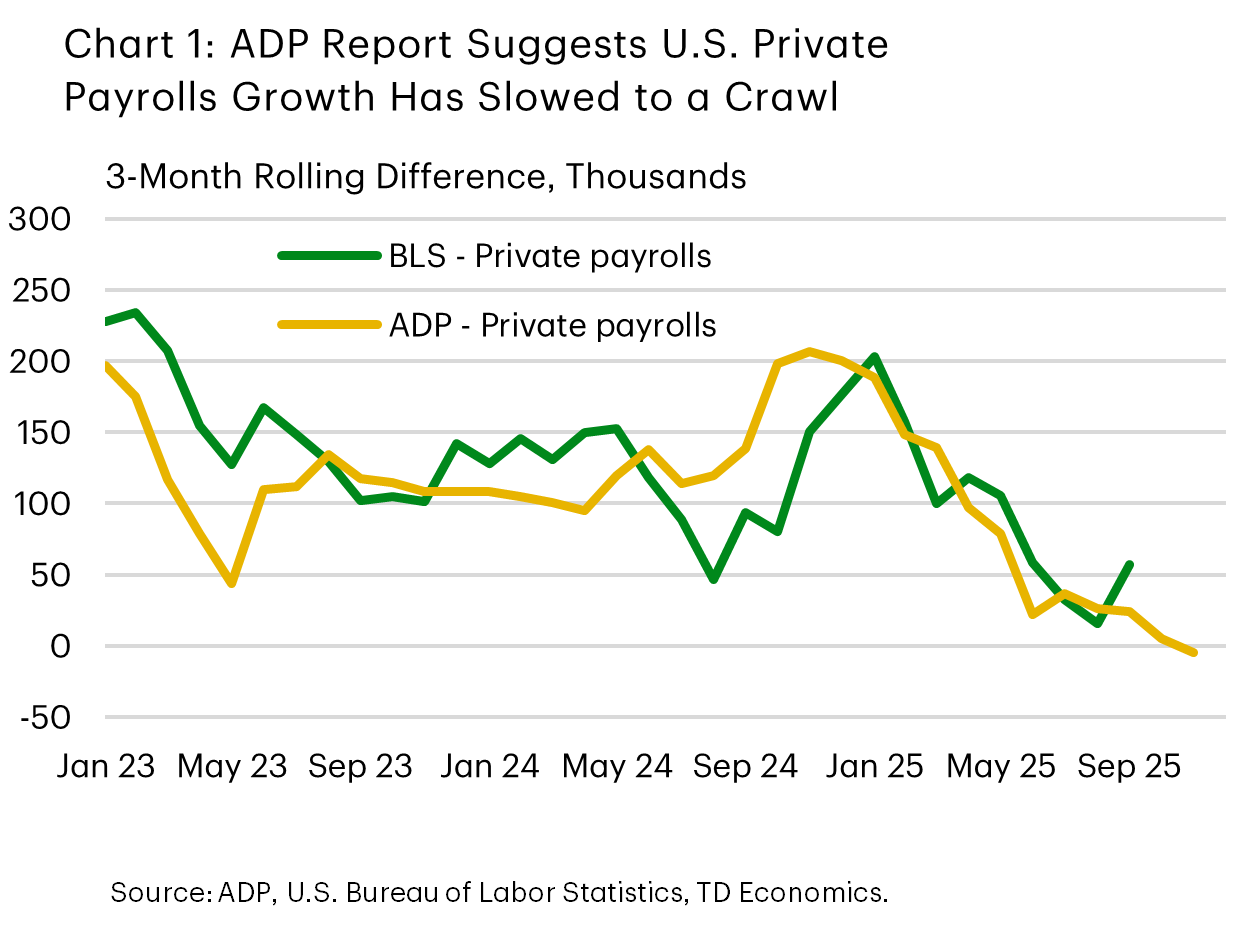

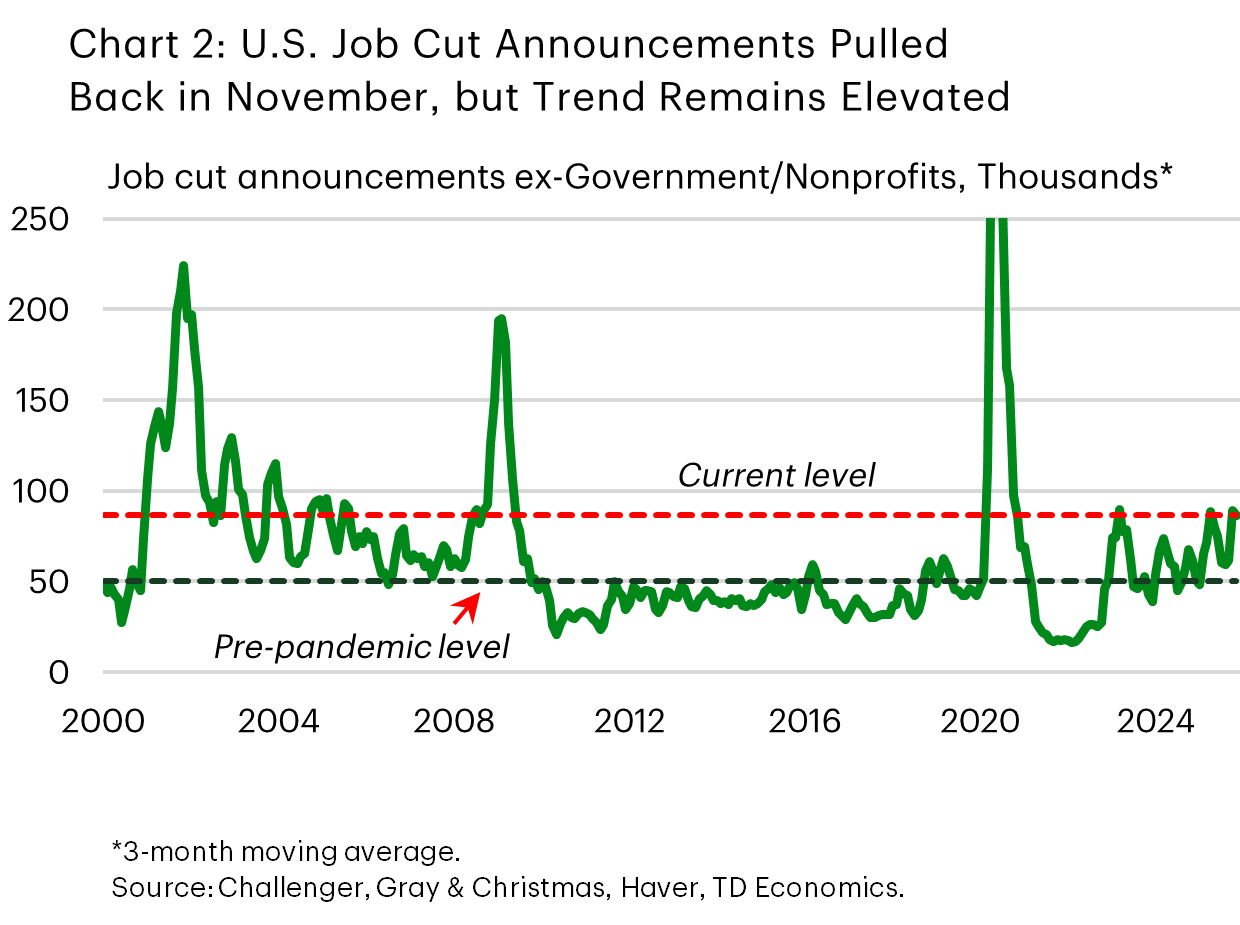

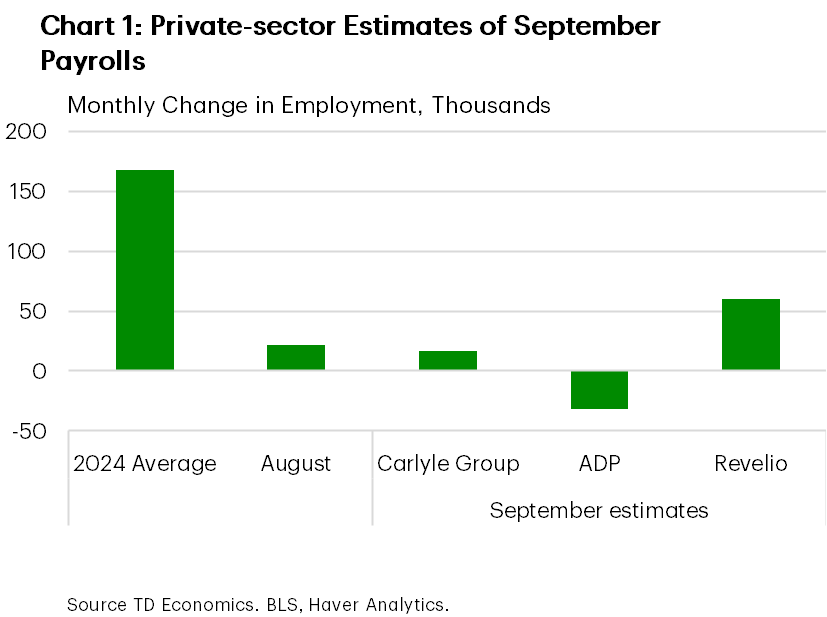

Employment data was mixed. Initial jobless claims dropped to a three-year low of 191k at November’s end. The Thanksgiving holiday may have distorted the data. But even prior to that last week, initial claims were still trending lower. Conversely, the ADP report showed private payrolls fell by 32k in November. Its three-month average, which is more closely aligned with the BLS equivalent, turned slightly negative too (Chart 1). Job cut announcements, meanwhile, also pointed to continued challenges. Layoff announcements in November were cut in half from their October tally, coming in at 71k. But even when looking past the weakness in the government sector, the trend in layoff announcements remains elevated (Chart 2). Overall, markets seemingly expect the Fed to focus on signs of labor market softness and maintain a cautious policy stance.

Our reading is that the Fed won’t disappoint market expectations next week. But in the New Year, the bar for additional cuts may be higher. Having delivered some insurance cuts, the Fed will likely take time to digest delayed economic reports and carefully assessing post-shutdown data to form a clearer picture of the economy’s health.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of November 28th, 2025

Financial News Highlights

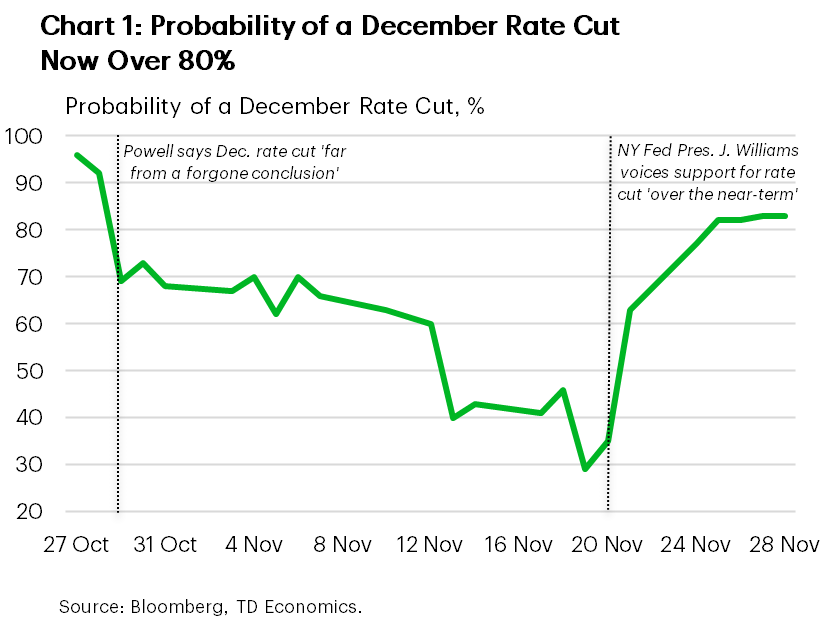

- Market expectations for a Fed rate cut on December 10th are now north of 80%, as key Fed officials voice support for a further reduction.

- Retail sales for September were a bit weaker than expected, suggesting less momentum heading into the fourth quarter.

- The Beige Book provided further anecdotal evidence that growth in the U.S. economy remains sluggish.

Equity Markets Gobble Up Prospects for a December Rate Cut

U.S. equity markets traded higher through the holiday shortened week, boosted by expectations for a December rate cut and renewed enthusiasm for the AI trade. Meanwhile, economic data out this week reinforced the narrative that some sluggishness has materialized in the U.S. economy. The S&P 500 is looking to end the week higher by over 3%, more than erasing last week’s losses and is now up 16% year-to-date. Treasury yields dipped by a few basis points on the week, with the 10-year currently hovering around 4%.

Fed futures have been on a wild ride recently. Just over a week ago, markets attached a roughly one-third probability to a December rate cut. But since then, two Fed officials who hew closely to Chair Powell, including NY Fed President John Williams and San Francisco Fed President Mary Daly (non-voting member) voiced support for a December rate cut. Pricing has since swung back to over 80% (Chart 1). The Fed doesn’t tend to fight the market and with the decision just over a week away, a further trimming in the policy rate looks to be a safe bet. Though if ADP employment data were to surprise to the upside next week, odds may yet shift again.

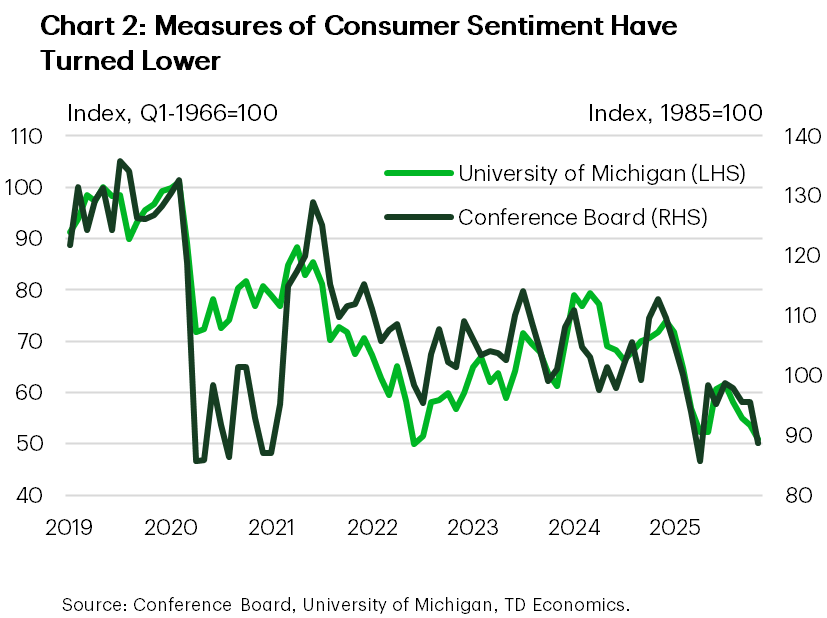

Turning to this week’s economic data releases, retail figures for September showed that spending slowed at the end of the third quarter – putting Q4 on a shakier footing. The softening in September spending isn’t entirely surprising. Measures of consumer sentiment have nosedived recently, with the Conference Board’s November reading slipping to its lowest level since April and second lowest reading since the depths of the 2020 Global Pandemic (Chart 2). Survey details show that consumers’ assessment of job availability is particularly downbeat, as are prospects for making ‘larger purchases’ over the next six months. While shifts in consumer confidence metrics have proven to be a less reliable predictor of spending patterns post-pandemic, the steady downward trend across multiple measures suggests the direction of travel is likely to be lower over the near-term.

This was further confirmed in the Fed’s Beige Book, which noted that overall consumer spending had ‘declined further’ in recent months, even though higher-end retail spending remained resilient. The Fed’s contacts chalked some of the weakness up to the government shutdown, and a pullback in EV sales following the expiration of the federal tax credit. However, the softening labor market also likely had some influence, with the majority of Districts seeing a decline in hiring and about half noting weaker labor demand. Importantly, employers across most Districts reported limiting headcounts using hiring freezes, ‘replacement-only’ hiring and attrition rather than through layoffs.

This reinforces the ‘low hire, low fire’ narrative’ (see report). But it’s a precarious balance, and one where the downside risks have the potential to materialize very quickly. While this supports the case for a bit more easing in the fed funds rate, still elevated inflation and a policy stance that is quickly closing in on neutral are important considerations that can’t be overlooked. Bringing the policy rate much lower runs the risk of putting the Fed out of position in the event the labor market were to firm in the months ahead.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Taxes in Retirement: Money-Saving Strategies

Whether you’re a business owner or a working professional, you’ve spent years sharpening your tax strategy. Managing taxes in retirement is a little different. When you understand how retirement income taxes work, you can build a tax strategy to help you keep more of what’s yours.

Understand How Retirement Income Is Taxed

Curious about taxes in retirement? Many retirees have multiple income streams, and not all income streams are taxed the same way. Generally, these sources are taxed at your individual income tax rate:

- Distributions from 401(k)s, traditional IRAs, and other tax-deferred accounts

- Pension payments

- Wages (if you work part-time or have self-employment income)

- Short-term capital gains

Some types of income, including qualified withdrawals from Roth accounts and health savings account (HSA) distributions, generally aren’t taxed.

Depending on your tax situation, up to 85% of your Social Security benefits may be taxed as earned income.

Tax-Efficient Strategies to Keep More of What You Earn

When it comes to handling taxes in retirement, no strategy is universal. Depending on whether you’ve already retired or are planning to retire soon, your approach may vary.

For Pre-Retirees

As a pre-retiree, consider these strategies:

- Max out contributions to your retirement plans: If you’re still working, consider contributing up to the maximum allowable amount in your 401k and IRAs.

- Diversify your accounts: There’s no way to predict your future tax bracket and future tax laws with complete certainty. When you have a mix of tax-free, tax-deferred, and taxable accounts, it becomes easier to optimize your strategy for taxes in retirement.

For Retirees

If you’ve already retired, these strategies may make sense for you:

- Explore qualified charitable distributions (QCDs): You can reduce the taxable amount of your required minimum distributions through gifting to a qualified charity.

- Develop an intentional distribution strategy: Focus on a distribution approach that allows you to reduce your taxes over time. Keeping your taxable income low can help you reduce Medicare premiums too.

Our Commitment to Comprehensive Financial Care

Getting familiar with strategies that can reduce your taxes is a great start. Finding a great tax preparer to help you with your taxes is another important step in the process.

We have heard from our clients over the last couple of years that they have struggled to find a good tax preparer for a reasonable price. Although we aren’t a tax-preparation firm, we are able to file tax returns for current clients that have straightforward tax situations.

Your Guide to Taxes in Retirement

Aventus Investment Advisors is here to help you navigate your finances before and during retirement. As fiduciary advisors, we act in your best interests at all times. Whether you’re already retired or you are working toward retirement in the near future, we’re ready to help you build a customized plan.

If you have questions about what we do or want to learn more about taxes in retirement, contact us online today. To schedule a meeting, call (704) 237-4207 or email jason.list@aventusadvisors.com.

About Jason

Jason List, CFP®, CFA, is a Senior Client Advisor with Aventus Investment Advisors in Cornelius, North Carolina. With nearly two decades of industry experience, he helps clients organize, grow, and preserve their wealth through comprehensive planning, investment management, and tax-focused strategies. Clients value his approachable style and the confidence that comes from having a fiduciary partner to navigate life’s milestones, whether retiring, traveling, or buying a new home.

Jason earned his undergraduate degree in mathematics from the University of North Carolina at Charlotte, a master’s in finance from Shanghai University of Finance and Economics, the CERTIFIED FINANCIAL PLANNER® designation in 2012, and the Chartered Financial Analyst® designation in 2024. He joined Aventus in 2021 after working at large financial institutions, drawn to the firm’s focus on personalized, transparent advice.

A Charlotte-area resident for more than 30 years, Jason lives with his wife, Ashley, and their beagle, Mindy. He enjoys traveling, hiking, bowling, and watching sports, and also serves as treasurer for a nonprofit that supports disenfranchised children in Kenya. To learn more about Jason, connect with him on LinkedIn.

Financial News for the Week of November 21, 2025

Financial News Highlights

- Equity markets sold off this week as investors continued to worry about the valuations of AI companies.

- Although the data fog has started to clear, it did little to resolve differences among FOMC members, with a rate cut in December now looking less likely.

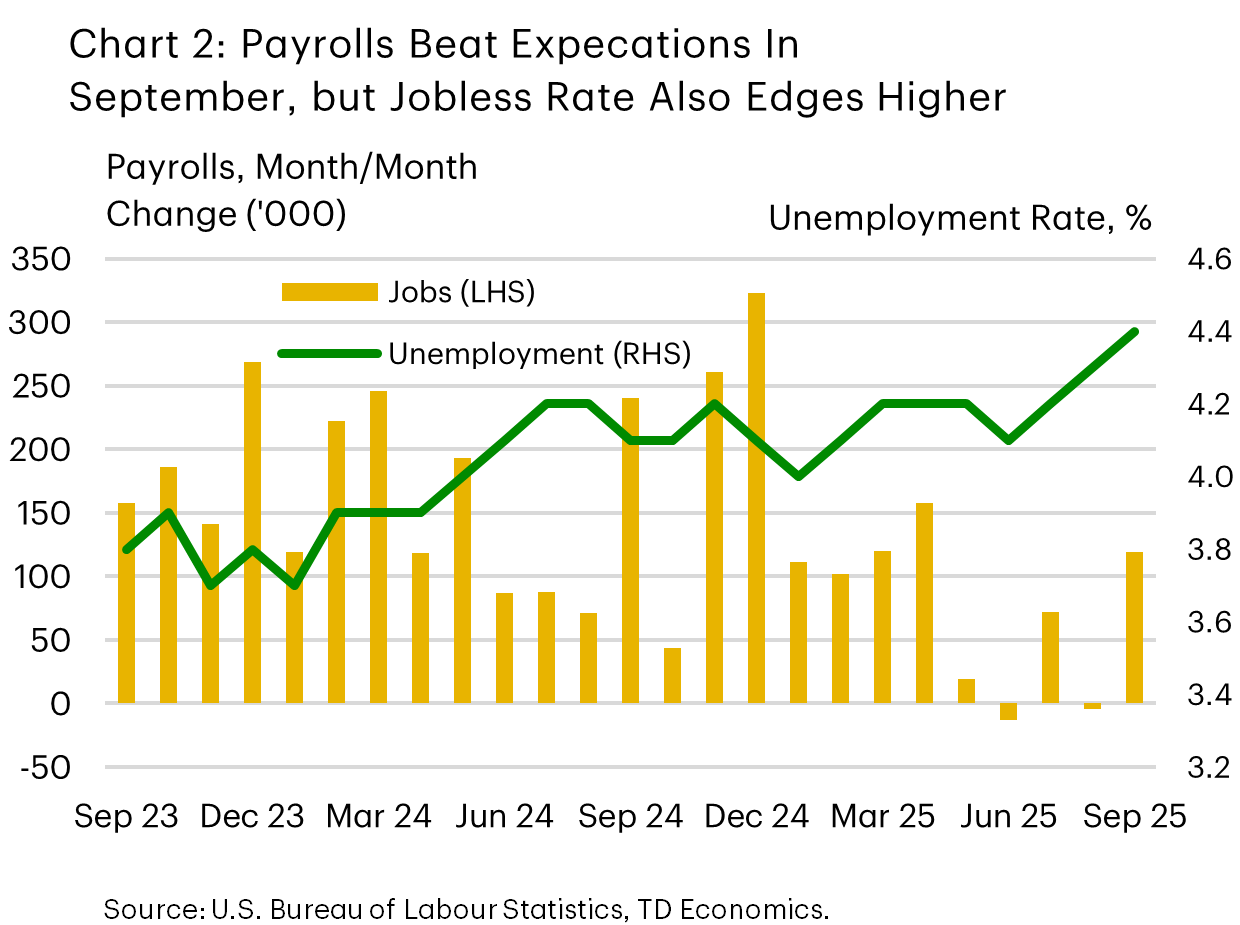

- The delayed September payrolls report was better than expected, rising by 119,000 jobs. However, the unemployment rate increased to a new cyclical high of 4.4%.

Data – In, December’s Rate Cut – Out?

Equity markets sold off this week amid concerns about high tech-stock valuations and aggressive AI capital spending. As of writing, the tech-focused Nasdaq Composite was down 2.5% on the week, while the S&P 500 had declined 1.9%.

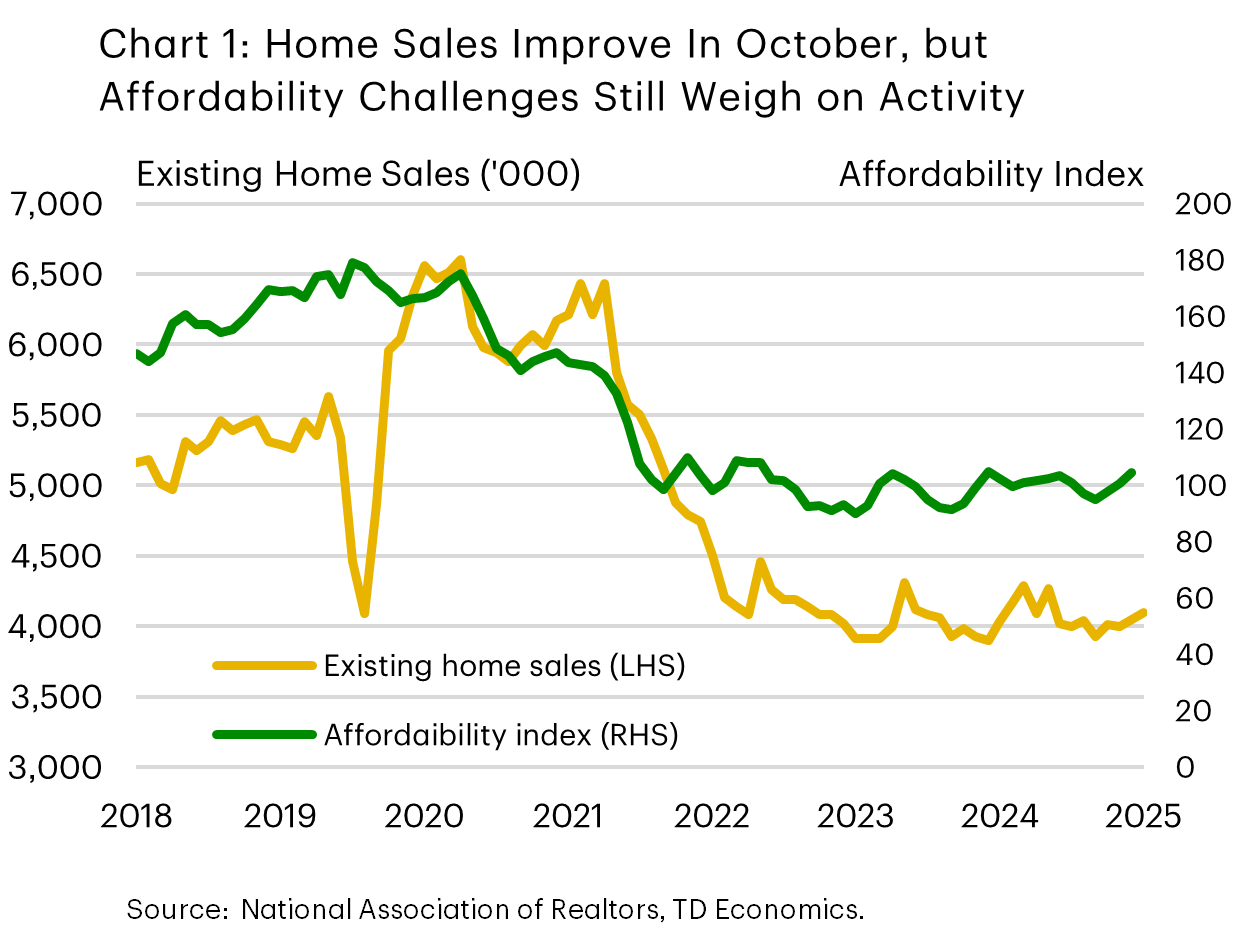

Official economic data began to trickle in, with September’s payroll report being the most notable. However, reporting backlogs are expected to persist. October payrolls will be released with November’s figures on December 16, not in time for the FOMC’s next meeting on December 9–10. Other data points, like October CPI, will not be released. On the housing side, existing home sales edged higher in October, supported by falling mortgage rates. Still, the housing market continues to tread water as affordability remains stretched, despite some modest improvement in recent months (Chart 1).

A busy slate of Fed speakers reaffirmed the lack of consensus among FOMC members for another rate cut in December. Some, like Governor Jefferson (voter), advocated for a cautious, “meeting-by-meeting approach,” as the policy rate moves closer to neutral. Chicago Fed President Goolsbee (voter) joined the hawkish camp, downplaying the recent labour-market weakness and emphasizing the lack of progress on inflation.

Minutes from the October FOMC meeting also highlighted the growing divide, with many participants seeing no case for easing in December. This contributed to market pricing shifting towards the next cut coming in January rather than December. After that meeting, Chair Powell stated that a December cut “is not a foregone conclusion, far from it.”

But policy doves like Governor Waller (voter), argued that another rate cut in December is warranted, given his assessment that the labor market remains weak, longer-term inflation expectations are anchored, and the impact of tariffs on inflation are likely to be transitory. Echoing this view, FOMC Vice Chair Williams emphasized that inflation expectations remain “very well anchored” and noted room for further cuts over the ‘near-term’. These remarks helped to tip market odds back in favour of a December cut on Friday morning.

The delayed September payrolls report did little to reconcile the divide among policymakers. Hawks were likely reassured by the better-than-expected job gains: payrolls rose by 119k—the strongest reading since April (Chart 2). However, policy doves are likely to point to the negative revisions to prior months, the narrow concentration of job gains, and the uptick in the unemployment rate.

All in all, hawkish voters appear to outnumber the doves on the FOMC for now, and there is no official jobs or inflation data before the next meeting to shift views. Therefore, we expect the slow-and-steady approach to carry the day and for the Fed to hold rates steady in December. Chair Powell perhaps said it best: “when you’re driving in the fog, you slowdown”. That said, the door for a cut in January remains open.

Ksenia Bushmeneva, Economist | 416-308-7392

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

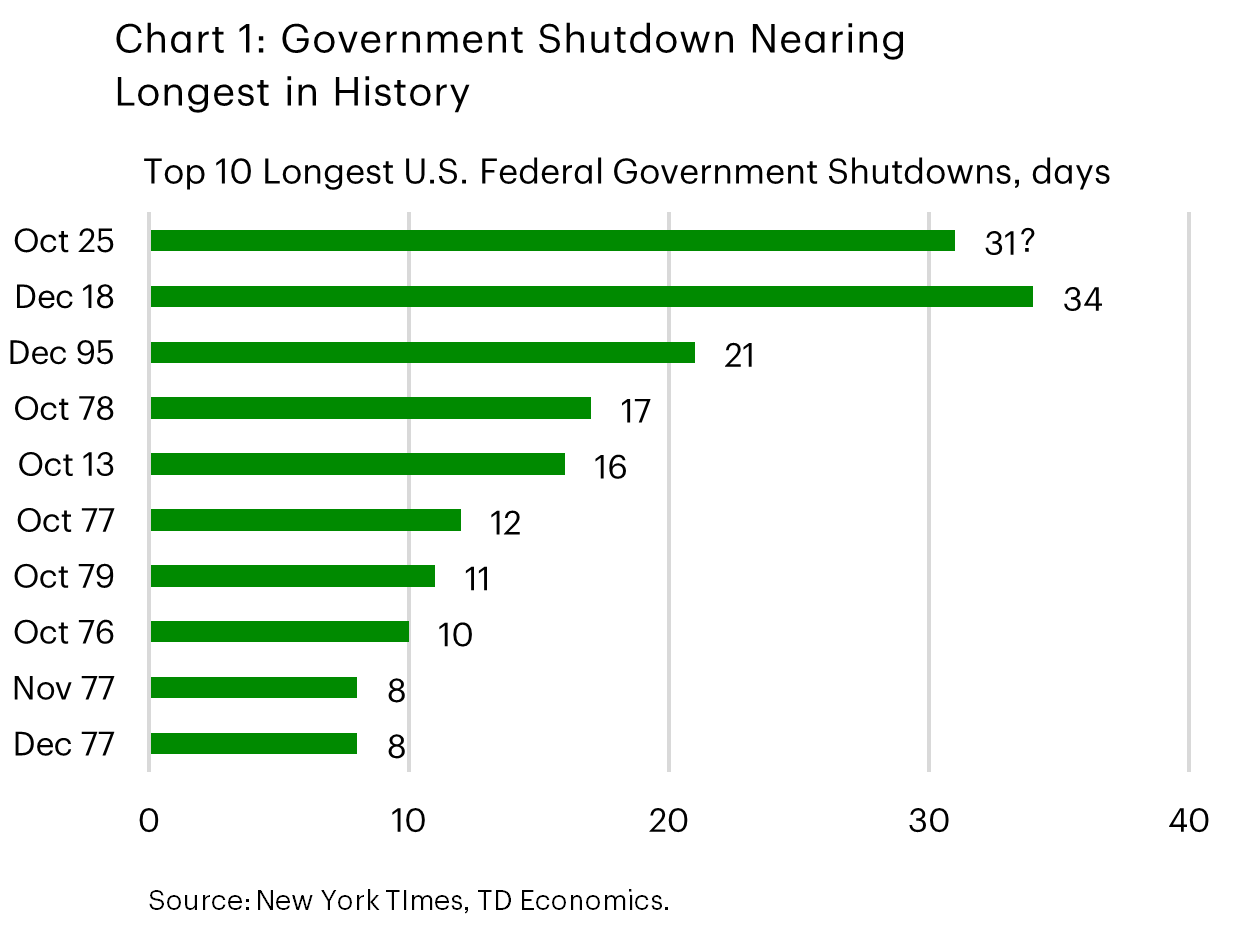

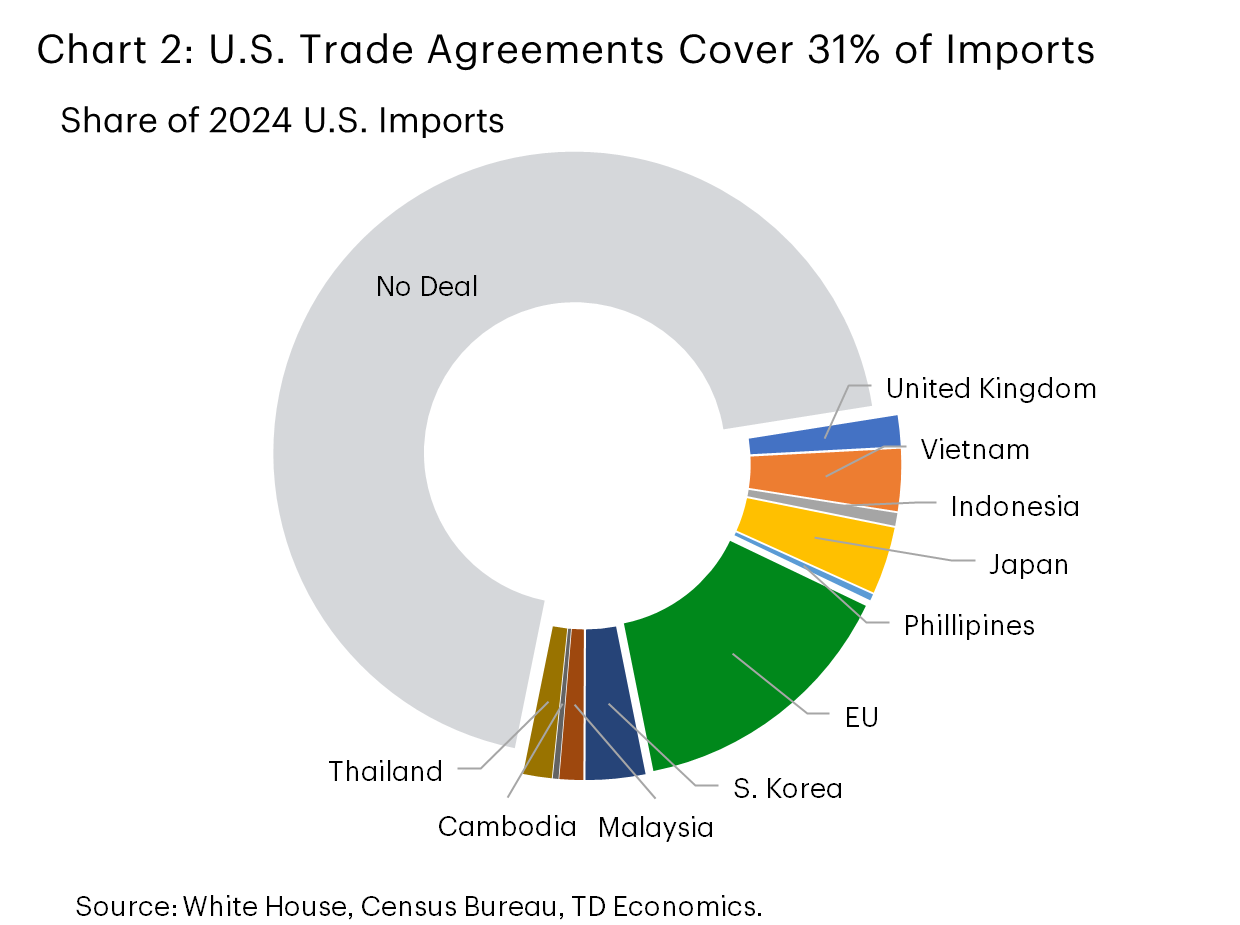

Financial News for the Week of October 31st, 2025

Financial News Highlights

- With no end in sight, the government shutdown is nearing the longest in U.S. history.

- A meeting between President Trump and President Xi led to a further easing in U.S.-China trade tensions. The administration also announced trade agreements with Thailand, Malaysia and Cambodia.

- The Federal Reserve delivered another quarter-point rate cut – bringing the target range to 3.75%-4%. It will also end its quantitative tightening program as of December 1st.

President Trump Deals His Way Through Asia

The government shutdown entered its 31st day on Friday, and if it extends past November 3rd, will become the longest in U.S. history (Chart 1). At the time of writing, there is no offramp to end the shutdown. On Tuesday, Senate Democrats rejected (for the thirteenth time) a House-passed stopgap measure to fund the government through November 21st, while Senator Thune pushed back on the idea that Republicans were considering piecemeal bills that would reopen portions of the government. Elsewhere, President Trump traveled to Asia this week, which culminated in three new trade agreements and a further easing in trade tensions with China. Stateside, the Federal Reserve delivered another rate cut and signaled an end to its quantitative tightening program. Powell’s remarks that a December rate cut “is not a foregone conclusion” led to some firming in Treasury yields, as market pricing for a December cut fell to 70%. A healthy slate of earnings reports capped off the week, pushing the S&P 500 up 1.0%.

In a further move to de-escalate trade tensions with China, President Trump agreed to cut the fentanyl tariffs from 20% to 10%, suspend the increase of its reciprocal tariffs (scheduled to rise from 10% to 35% on November 10th) and ease restrictions on blacklisted Chinese firms. In return, China eased its restrictions on rare earth exports and said it would increase purchases of U.S. soybeans. Both countries also agreed to suspend their port fees, which came into effect earlier this month.

The U.S. also reached trade agreements with three other counties this week, including Thailand, Malaysia and Cambodia. Trade to these countries account for roughly 3% of total U.S. annual imports, but combined with the other seven agreements, 30% of U.S. trade is now covered by a new trade deal (Chart 2). Details of this week’s agreements remain vague, but based on White House fact sheets, each country will face a 19% reciprocal tariff rate and have agreed to reduce tariffs and trade barriers on U.S. imports along with making commitments to purchase energy products and aircrafts.

The Federal Reserve’s move to cut its benchmark rate by another 25 basis points – bringing the target range to 3.75-4.0% – came as little surprise. However, Powell’s remarks in the press conference regarding a December rate cut being far from guaranteed offered a shot in the arm to market odds, which had another cut as a near certainty. Indeed, the statement showed a growing divide among FOMC members. Recently appointed Stephen Miran dissented in favor of larger (50bps) cut, while Jeffery Schmid voted to hold rates steady. Given the data fog created by the government shutdown, Powell noted that there was a “growing chorus to at least wait a cycle” before making another cut, particularly given today’s policy rate is at the upper end of some estimates of neutral. We interpret Powell’s hawkish tone as a way of bringing more balance into market expectations. Another cut in December remains our base case, but we acknowledge that a flurry of data releases once government reopens could quickly shift views on the economic outlook and reshape the Fed’s thinking on its policy adjustment.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of October 24th, 2025

Financial News Highlights

- The federal government shutdown entered its 4th week, becoming the 2nd longest in history.

- The CPI data release for September, delayed by the shutdown, showed inflation moderated during the month but remained elevated on aggregate.

- Trade negotiations with China will ramp up over the next week in advance of the November 1st deadline for 100% additional tariffs threatened by the President.

Persistent Inflation, Shutdown Pose Challenges for Federal Reserve

The ongoing government shutdown became the 2nd longest in history this week, as it stretched into week 4. With divisions in Congress largely unchanged relative to September, a resolution remains out of sight, but as the economic impacts become more material, intransigence will likely yield. Elsewhere in D.C., President Trump called off trade negotiations with Canada over the use of anti-tariff television advertisements broadcast in the U.S., forestalling a near-term trade agreement with the nation’s second largest trading partner. Despite political dysfunction in the Capitol and rising trade tensions in recent weeks, the S&P 500 still managed to rise 2% this week from a host of positive third quarter earnings reports.

While the Department of Labor remains unfunded, the CPI data for September was released on Friday owing to its use in the annual inflation adjustment to social security payments. The data showed that recent inflationary pressures moderated slightly in September but remained elevated on aggregate, with the three-month annualized percentage change in core CPI running above 3.5% (Chart 1). With price growth still well above the Fed’s 2% target and the timing of future data releases uncertain, policy decisions are expected to be cautious moving forward.

The shift in the Federal Reserve’s stance on monetary policy over the past few months came on the heels of a slowdown in the labor market, tracking of which has been obscured by the lapse in data releases. As the FOMC begins deliberations next week, they will likely assume that the slowdown persisted through September and opt to meet financial market expectations for a quarter-point rate cut. Chair Powell’s press conference will be closely watched for insights into how the policy response function of the Federal Reserve will adapt to a prolonged government shutdown, as inference becomes more difficult the further we are from the last official data release.

On the trade front, U.S. Treasury Secretary Bessent will be meeting with a Chinese delegation in Malaysia over the weekend. The deadline to reach some form of agreement is becoming tight, with President Trump’s threat of 100% tariffs on China starting November 1st. The President will also be travelling to Asia Friday night, with plans to visit Malaysia, Japan, and South Korea, culminating with the Asia Pacific Economic Cooperation (APEC) summit where he is expected to meet with his Chinese counterpart. Amid rising trade tensions in recent weeks, financial markets will be watching for any signs of de-escalation.

Markets will also be watching for several big tech earnings reports next week, including Microsoft, Apple, Alphabet, Amazon, and Meta, which collectively account for nearly a quarter of the S&P 500 (Chart 2). Given the high level of concentration in equity markets, growing concerns about elevated valuations, and the influence of these trends on the economy, these results will be monitored closely on the heels of Wednesday’s Federal Reserve decision.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of October 17th, 2025

Financial News Highlights

- Alternative data helped fill the void of official releases due to the ongoing government shutdown. The Cleveland Fed’s Inflation Nowcasting model estimated core inflation remained around 3% (y/y) in September.

- The Chicago Fed’s Advance Retail Trade Summary indicated retail & food services sales excluding autos were healthy in September.

- Fed Chair Powell signaled that the central bank could soon reach a point where it may stop reducing the size of its balance sheet, also known as quantitative tightening.

Reading the Tea Leaves Amidst the Data Fog

This week’s U.S. economic landscape remained shrouded in fog due to the lack of official data amidst the ongoing government shutdown. If it continues until Monday, it will be the third longest in history. In the official data drought, focus has shifted to alternative indicators, particularly from the Federal Reserve, which is still operating during the shutdown. US-China trade tensions ebbed and flowed, while concerns surrounding regional banks made a comeback, weighing on equity markets. Still, equities managed to eke out some gains, with the S&P 500 up 1% from last Friday’s low. Bond yields declined amid uncertainty and expectations of further monetary easing. Notably, the 10-Year Treasury yield fell below 4% and is now hovering near last year’s level.

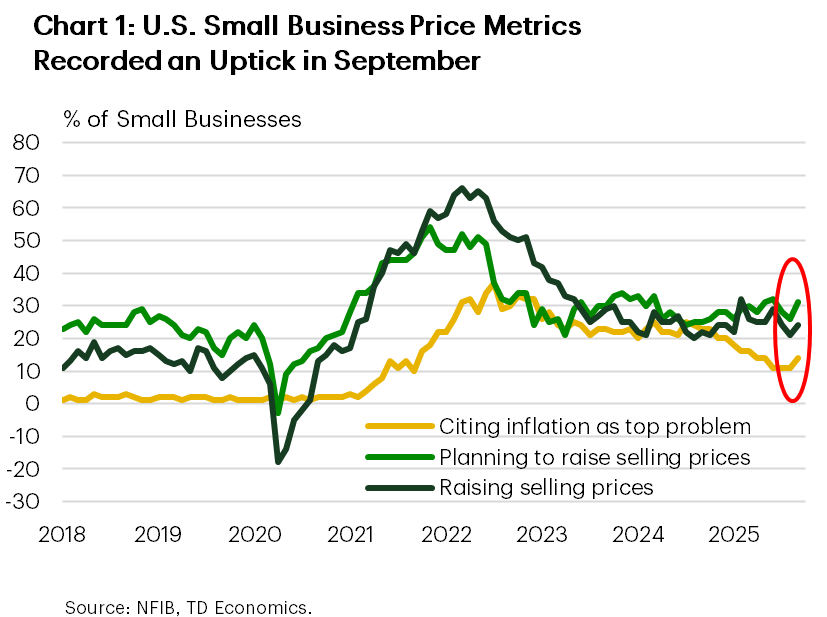

In the absence of the CPI report, alternative inflation indicators are sending conflicting signals. The Cleveland Fed’s Inflation Nowcasting model estimated core inflation at 0.26% month-over-month in September, suggesting year-on-year core inflation remained near 3%. The lack of acceleration would support another Fed rate cut amidst a deteriorating labor market. However, the Fed’s Beige Book reported further price increases, with several districts noting “faster input cost growth due to higher import prices and rising costs for services like insurance, health care, and technology”. The NFIB’s small business survey also showed moderate upticks in its price metrics (Chart 1). The CPI report is set to be released next week, which should help clear some of the fog.

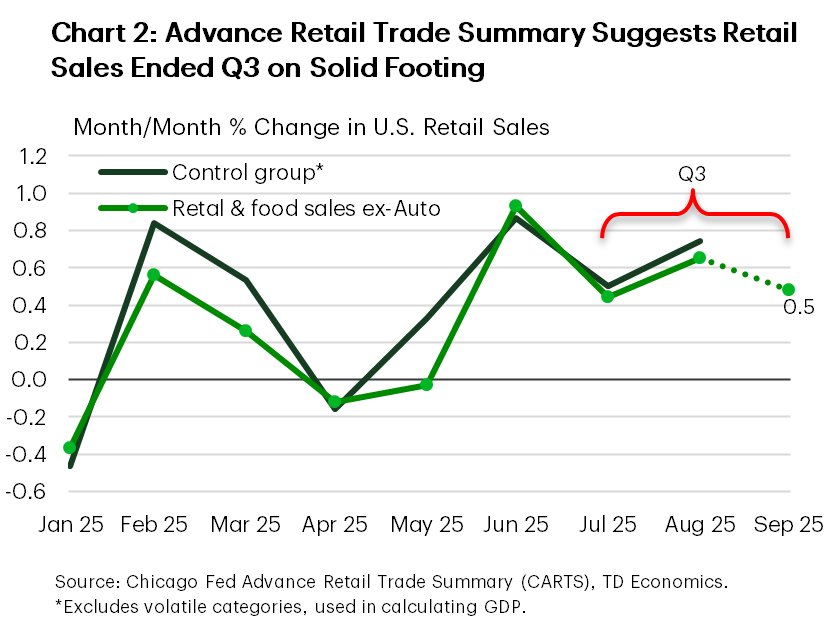

The September retail sales report is also delayed, but the Chicago Fed’s Advance Retail Trade Summary (CARTS), which tracks weekly sales, offers some insight. CARTS indicates that retail & food services sales excluding autos rose by 0.5% in September, suggesting a solid finish to the third quarter (Chart 2). However, given ongoing uncertainty and other consumer challenges, momentum is expected to ease in the fourth quarter. The Beige Book echoed this, noting that overall consumer spending, especially on retail goods, trended down in recent weeks, with auto sales being the main exception.

On the employment front, the Beige Book described labor demand as “subdued” and employment levels as “largely unchanged”. More employers reported lowering headcount through layoffs and attrition, citing weak demand, high uncertainty, and, in some cases, increased investment in AI. Layoffs were mentioned 14 times, up from 6 previously. NFIB employment metrics also pointed to a weak hiring trend among small businesses in September.

Fed Chair Powell reiterated recent messaging and placed more emphasis on labor market risks in a speech this week, supporting additional easing. Powell also signaled the central bank could soon stop reducing the size of its balance sheet. While he provided no set timeline for the end of quantitative tightening (QT), he stated “we may approach that point in the coming months,” noting early signs that liquidity conditions are gradually tightening.

Reading the tea leaves, labor market risks remain the key focus. As such, the Fed is likely to deliver another rate cut at the end of this month. The signal that QT may soon end further reinforces the Fed’s dovish stance.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of October 10th, 2025

Financial News Highlights

- The government shutdown continues through its second week, with no clear end in sight, while trade tensions between the U.S. and China have suddenly heated up.

- Absent official data, the market is turning to imperfect private-sector alternatives, which suggest the labor market continued to cool in September.

- We don’t see any developments this week that are likely to cause a big shift in the perception of the economy or the outlook, and so we are still penciling in two more quarter-point rate cuts from the Federal Reserve by year-end.

No Data, No Problem

Up until Friday, markets had been relatively calm amid the ongoing government shutdown, which has entered its 10th day. President Trump’s threat to increase tariffs on China this morning, in response to China’s export controls on rare-earth metals, has upended that. President Trump has gone so far as to declare he is not interested in meeting President Xi in person as previously scheduled for the end of the month, leading to a sharp sell-off in US equities and pushing Treasury yields lower. Markets stoically withstood the failure of seven separate proposals to re-open the government, but the possible breakdown of U.S.-China trade negotiations may be too much to bear. If that wasn’t enough, the end of the shutdown is not clearly in sight. The Senate is now adjourned until October 14, which all but guarantees that military members will miss a full pay cycle, an unprecedented development.

The outlook for the shutdown is not the only thing that is cloudy. The government shutdown means that official economic data are not being published, and policymakers, businesses, and households are unable to see new data on the state of the economy. Various private-sector groups have produced estimates of what happened to employment in September, shown in Chart 1. This was the key piece of data which was due to be published last Friday. While these alternative estimates generally suggest the labor market continued to cool through September, these measures are at best imperfect proxies for the official data. As for what data we do have this week, the preliminary reading of the University of Michigan’s consumer confidence ticked a touch higher in October. However, expectations on the future outlook continued to slide for a third consecutive month, likely driven by the softening labor market and still elevated uncertainty on trade policy.

Several members of the FOMC spoke this week, offering some insight into their thinking amidst the shutdown. New York Fed President Williams indicated that the lapse in government data would not deter him from further easing the policy rate at the Fed’s coming meetings. Meanwhile, other speakers continued to reiterate prior views. Kansas City Fed President Schmid voiced concern about inflation, while Miran, the only FOMC member to vote for a larger 50 basis point rate-cut at the last meeting, again indicated how he expected inflation to moderate. It is little surprise that market pricing at the next Fed meeting has remained relatively unchanged through the government shutdown. Expectations for further easing at a moderate pace are in line with the general view we observed in the FOMC minutes released this week, that interest rates are currently moderately restrictive and risks have shifted somewhat to the downside.

Normally, we would be looking ahead to next week’s release of CPI for more information on how prices are reacting to tariffs, but we are following the shutdown. We will also be closely watching trade negotiations between the U.S. and China to see what comes of today’s escalation.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.