Financial News for the Week of June 27th, 2025

Financial News Highlights

- An abrupt ceasefire between Israel and Iran sent oil prices tumbling, while stock markets rejoiced on the news, with the S&P 500 up roughly 3% on the week at the time of writing in financial news.

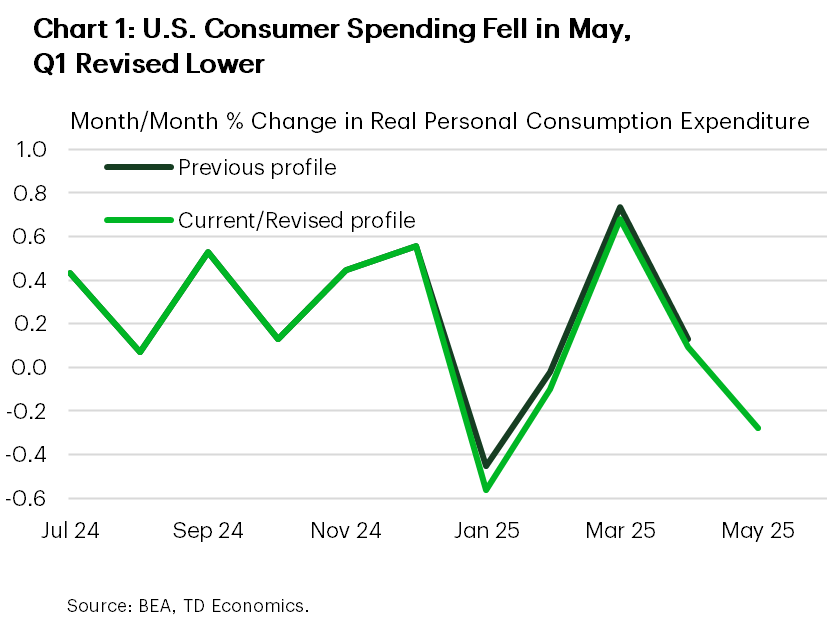

- The U.S. consumer is showing signs of fatigue with real spending falling 0.3% in May.

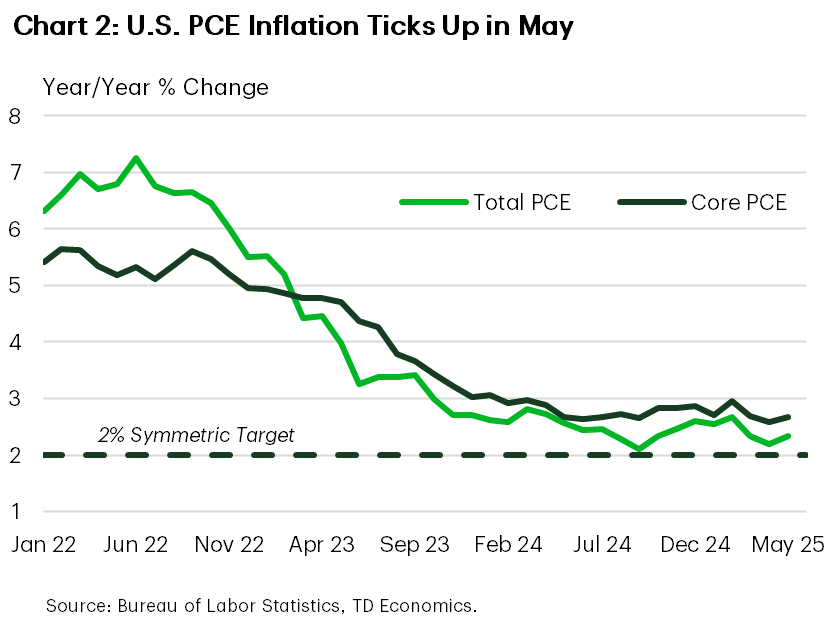

- The Fed’s preferred inflation gauge, core PCE, ticked up modestly from 2.6% to 2.7% (y/y) in May.

Some Calm After the Storm

Geopolitical developments continued to grab headlines this week. However, the world breathed a sigh of relief when Pres. Trump announced a ceasefire between Israel and Iran on Monday. Oil prices fell sharply on the news, while equity markets rallied. This was followed by what appeared to be a successful NATO summit, where most members agreed to increase defense spending targets to 5% of GDP by 2035. Some good news also trickled in on the trade front, with China pledging to approve applications for rare-earth exports to the U.S. – a development that could pave the way for more fruitful trade negotiations. These developments appeared to overshadow more muted developments on the home front.

Geopolitical developments continued to grab headlines this week. However, the world breathed a sigh of relief when Pres. Trump announced a ceasefire between Israel and Iran on Monday. Oil prices fell sharply on the news, while equity markets rallied. This was followed by what appeared to be a successful NATO summit, where most members agreed to increase defense spending targets to 5% of GDP by 2035. Some good news also trickled in on the trade front, with China pledging to approve applications for rare-earth exports to the U.S. – a development that could pave the way for more fruitful trade negotiations. These developments appeared to overshadow more muted developments on the home front.

The passage of the ‘One, Big, Beautiful Bill Act’ hit a snag in the Senate, ahead of Thursday’s vote. The Senate parliamentarian reportedly ruled out several major measures in the legislation, most notably provisions related to Medicaid cuts – complicating the GOP’s math on spending cuts. It remains unclear if the bill will pass by the Republican’s self-imposed deadline of July 4th.

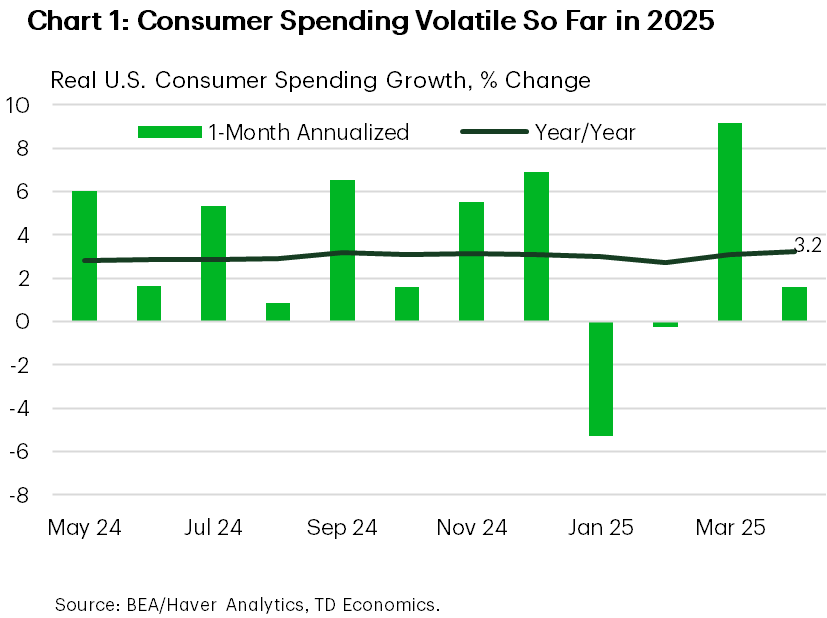

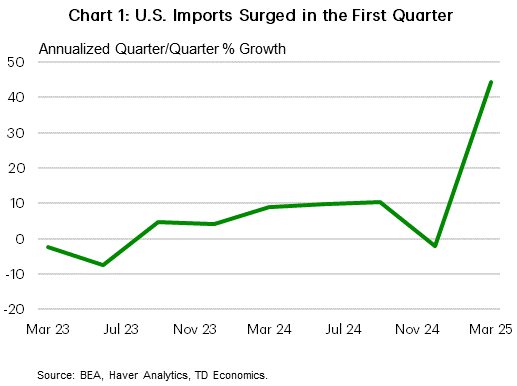

On the data front, the highlight of the week was the May release of personal income and spending. Personal income fell by 0.4% month-on-month (m/m), owing to a sharp pullback in transfer payments. Importantly, compensation to employees – nearly two-third of income – rose by a healthy 0.4% m/m in financial news. However, there were definite signs of waning consumer resilience. Goods spending fell 0.8% m/m, while services were flat on the month, with total spending down 0.3% on the month (Chart 1). Part of the softening in services spending was telegraphed earlier in the week in the third release of Q1 GDP, where it was revised to just a 0.6% gain (previously 1.7%), implying less momentum heading into Q2.

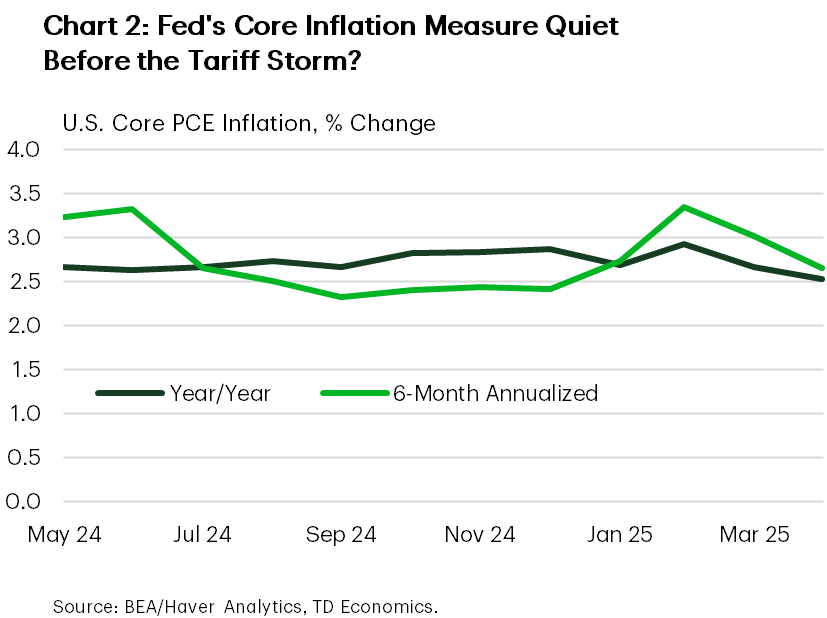

So far, the tariff impacts on inflation have remained relatively contained. While core PCE inflation – the Fed’s preferred gauge – heated up a touch in May, the monthly gain was due to relatively equal contributions from goods and services prices, pushing the year-on-year to 2.7% (Chart 2). Over the coming months, tariff impacts are expected to intensify, though the extent of price passthrough remains uncertain. Driving this point home, Chair Powell maintained a cautionary stance during his semiannual testimony to Congress this week, stating that he expects policymakers to stay on hold until they have a better handle on the impact tariffs will have on prices. This came in contrast to other Fed speakers, including Governor Waller and Bowman, who both noted that they support a July rate cut.

So far, the tariff impacts on inflation have remained relatively contained. While core PCE inflation – the Fed’s preferred gauge – heated up a touch in May, the monthly gain was due to relatively equal contributions from goods and services prices, pushing the year-on-year to 2.7% (Chart 2). Over the coming months, tariff impacts are expected to intensify, though the extent of price passthrough remains uncertain. Driving this point home, Chair Powell maintained a cautionary stance during his semiannual testimony to Congress this week, stating that he expects policymakers to stay on hold until they have a better handle on the impact tariffs will have on prices. This came in contrast to other Fed speakers, including Governor Waller and Bowman, who both noted that they support a July rate cut.

The growing divide among policymakers’ is shaped by differences in the expected passthrough from tariffs and underlying labor market conditions. Waller is of the view that the tariffs wont significantly boost inflation and that because of monetary policy’s long and variable lags, the Fed should proactively cut rates to head off potential downside risks to the labor market. However, Powell and others are of the view that the labor market remains in a good spot and need to see more definitive signs of softening before pushing ahead with rate cuts. This puts next week’s employment report in the spotlight.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of June 20th, 2025

Financial News Highlights

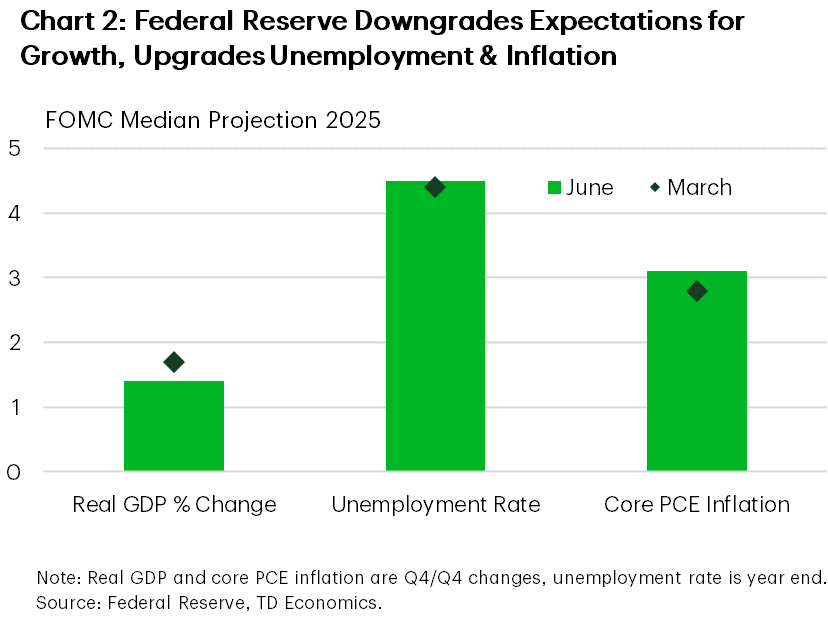

- The Federal Reserve left interest rates unchanged for the fourth consecutive time this year, as members revised their expectations for 2025 inflation higher relative to March in financial news.

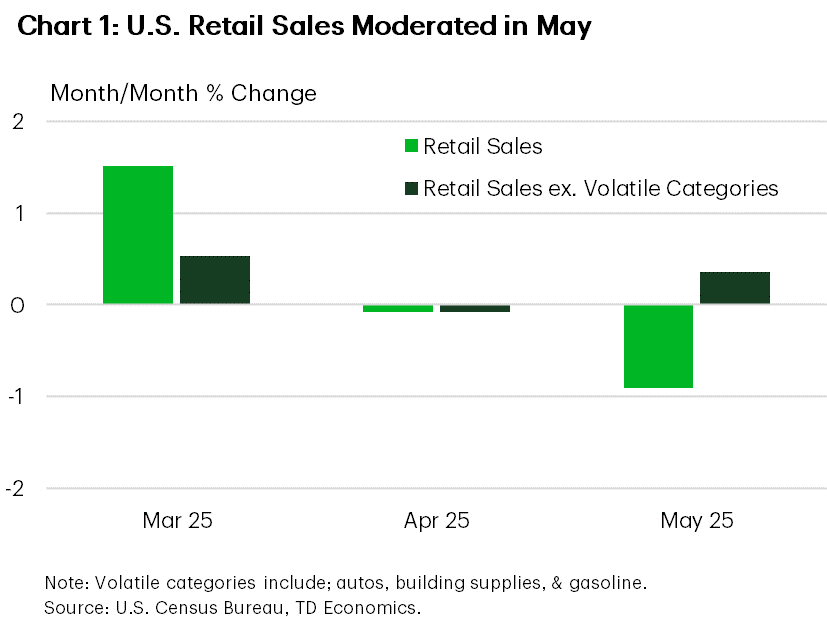

- U.S. retail sales in May contracted notably as tariff front-loading purchases ended, although the broader composition of sales appeared to remain healthy overall.

- Senate Republicans continued to race against the clock on their self-imposed July 4th deadline to pass the President’s multi-trillion-dollar One Big Beautiful Bill Act.

Economic Policy in Wait-and-See Mode

The last week of spring came with no shortage of headlines on the policy front, but it appears monetary, fiscal and trade policy remain in wait-and-see mode for now. The week began with President Trump leaving the G7 leaders’ summit early to monitor rising tensions in the Middle East, which have continued to push oil prices higher. On the home front, a handful of economic data releases and a Federal Reserve interest rate decision were on deck. Meanwhile, Congressional Republicans continued to work on their sizeable tax cut and spending bill. As of the time of writing, equity and Treasury markets were roughly unchanged on the week.

The last week of spring came with no shortage of headlines on the policy front, but it appears monetary, fiscal and trade policy remain in wait-and-see mode for now. The week began with President Trump leaving the G7 leaders’ summit early to monitor rising tensions in the Middle East, which have continued to push oil prices higher. On the home front, a handful of economic data releases and a Federal Reserve interest rate decision were on deck. Meanwhile, Congressional Republicans continued to work on their sizeable tax cut and spending bill. As of the time of writing, equity and Treasury markets were roughly unchanged on the week.

Checking in on the health of the U.S. consumer, we saw U.S. retail sales fall materially in May, largely owing to a pull-back in categories that had seen front-loaded sales in advance of tariffs in months prior (i.e. autos, electronics, appliances, etc.). Excluding the more volatile categories, retail sales saw a healthy gain in May (Chart 1), likely continuing to be aided by a stable job market and solid real income growth. However, moving forward we expect both trends to ease as tariffs apply upward pressure to inflation that builds moving into the second half of the year (see here).

The Federal Reserve emphasized a similar expectation during their decision on Wednesday, with the FOMC’s median projections showing subdued economic growth for 2025, in addition to higher unemployment and inflation (Chart 2). The latter is what in part motivated the Fed to keep interest rates unchanged for a fourth time this year in June, with Chair Powell noting that the Fed was well positioned to wait to see how the economy evolved moving forward. Although tariffs are likely to only be a transitory shock to inflation, loosening monetary policy too quickly in this environment could add to upward pressure on prices – a risk the Fed is determined to avoid. For this reason, monetary policy easing is expected to be gradual through the second half of the year, with markets expecting the first cut of the year in September and only 50bps of cuts cumulatively.

The Federal Reserve emphasized a similar expectation during their decision on Wednesday, with the FOMC’s median projections showing subdued economic growth for 2025, in addition to higher unemployment and inflation (Chart 2). The latter is what in part motivated the Fed to keep interest rates unchanged for a fourth time this year in June, with Chair Powell noting that the Fed was well positioned to wait to see how the economy evolved moving forward. Although tariffs are likely to only be a transitory shock to inflation, loosening monetary policy too quickly in this environment could add to upward pressure on prices – a risk the Fed is determined to avoid. For this reason, monetary policy easing is expected to be gradual through the second half of the year, with markets expecting the first cut of the year in September and only 50bps of cuts cumulatively.

Elsewhere in Washington D.C. this week, Senate Republicans continued to table their versions of sections of the multi-trillion dollar ‘One, Big, Beautiful Bill Act’ (OBBBA), including the Senate Finance Committee, which oversees tax policy and Medicaid. On the surface, the Senate Finance Committee’s markup of the bill broadly includes less generous household tax cuts, more generous business tax cuts, and more stringent cuts to Medicaid compared to the House version. Given the OBBBA only passed the House by a margin of one vote in late May, passing a consolidated, bicameral bill is likely to be a challenging process, especially as Congress only has one week left in-session before their self-imposed July 4th deadline.

Looking ahead to next week, the OBBBA’s progression through Congress will continue to be closely monitored. We will also get an update on personal income & spending for May, which will include the Fed’s preferred inflation metric, core PCE. Possible trade deals remain a topic of interest, with the suspension of reciprocal tariffs scheduled to expire in less than three weeks.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of June 13th, 2025

Financial News Highlights

- The U.S. and China reached a tentative ‘framework’ of a trade deal on Wednesday in financial news. The U.S. administration also signaled an openness to extend the 90-day pause on reciprocal tariffs for some countries.

- WTI prices jumped by more than 6% or $4.5 per-barrel to $72.5 on Friday, following Israeli airstrikes on Iran.

- Inflationary pressures remained subdued in May, with both CPI and PPI readings coming in lower than expected, which helped to push Treasury yields lower.

Trade Tensions De-escalate Just as Geopolitical Tensions Heat-up

A further de-escalation in trade tensions came this week, with the U.S. and China announcing on Wednesday that they had reached a ‘framework’ of a trade deal. That same day, Treasury Secretary Scott Bessent signaled an openness to extend the administration’s current 90-day pause on reciprocal tariffs beyond July 9th for those countries who are ‘negotiating in good faith’. While the combined announcements helped to provide a temporary lift to equity markets, a further escalation in geopolitical tensions in the Middle East on Thursday evening sent shockwaves through global financial markets, pushing the S&P 500 modestly lower on the week. Oil prices shot higher by $4.5 per-barrel, with WTI currently trading at an 18-week high of $72.5. Meanwhile, cooler readings on CPI and PPI for the month of May, alongside healthy demand in 10-and-30-year Treasury auctions helped to pressure term-yields 10-15 basis points lower on the week, with the 10-year currently sitting at 4.38%.

A further de-escalation in trade tensions came this week, with the U.S. and China announcing on Wednesday that they had reached a ‘framework’ of a trade deal. That same day, Treasury Secretary Scott Bessent signaled an openness to extend the administration’s current 90-day pause on reciprocal tariffs beyond July 9th for those countries who are ‘negotiating in good faith’. While the combined announcements helped to provide a temporary lift to equity markets, a further escalation in geopolitical tensions in the Middle East on Thursday evening sent shockwaves through global financial markets, pushing the S&P 500 modestly lower on the week. Oil prices shot higher by $4.5 per-barrel, with WTI currently trading at an 18-week high of $72.5. Meanwhile, cooler readings on CPI and PPI for the month of May, alongside healthy demand in 10-and-30-year Treasury auctions helped to pressure term-yields 10-15 basis points lower on the week, with the 10-year currently sitting at 4.38%.

At this point, details of the U.S.-China trade deal remain limited. Based on what media outlets have reported, China has agreed to lift export restrictions on magnets and rare earth minerals, both of which are critical components in the production of electric vehicles, semiconductors and military equipment. In exchange, the U.S. has agreed to lift its ban on Chinese students but did not remove the export restrictions on high-end semiconductors. Moreover, the agreed framework did not alter the existing tariffs imposed by either country. As it currently stands, the U.S. effective tariff rate on China is around 40%, well off the post-Liberation Day peak of 155%, but still elevated by historical standards in financial news. And with trade levies on most other countries sitting around 10-12%, that puts today’s U.S. effective tariff rate at around 15%, which remains an ongoing concern for investors.

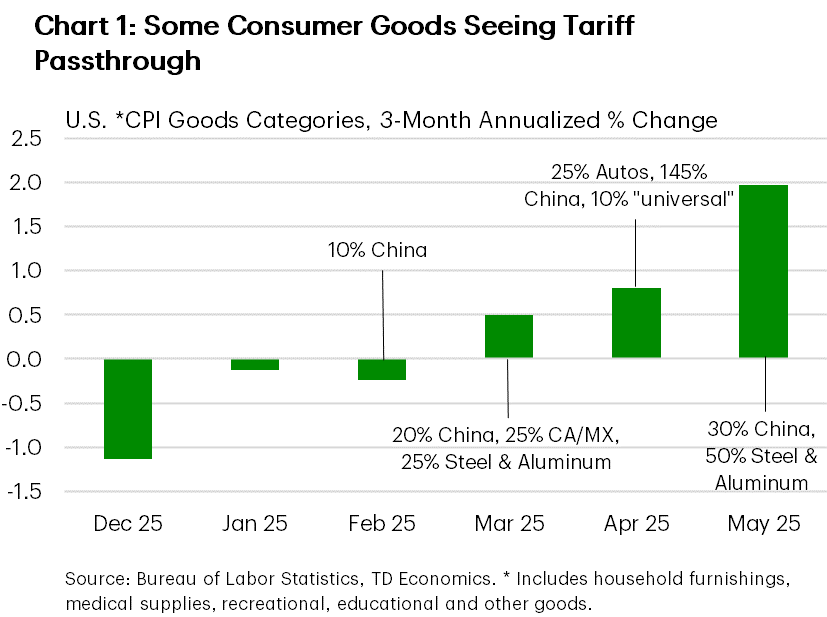

Encouragingly, broader price pressures in the economy remain subdued. May’s CPI inflation print came in on the softer side, as both goods and services prices rose by less than expected. Tariff related impacts remained minimal, though there was some evidence of price passthrough in home furnishings, recreational goods and medical supplies (Chart 1). But inflation is a lagging indicator, and with the bulk of the tariffs coming into effect between March and May, it’s still too soon to see a meaningful shift in pricing behavior. Moreover, the inventory stockpiling that occurred immediately following the tariff announcements has likely been another factor keeping the price gains at bay.

Encouragingly, broader price pressures in the economy remain subdued. May’s CPI inflation print came in on the softer side, as both goods and services prices rose by less than expected. Tariff related impacts remained minimal, though there was some evidence of price passthrough in home furnishings, recreational goods and medical supplies (Chart 1). But inflation is a lagging indicator, and with the bulk of the tariffs coming into effect between March and May, it’s still too soon to see a meaningful shift in pricing behavior. Moreover, the inventory stockpiling that occurred immediately following the tariff announcements has likely been another factor keeping the price gains at bay.

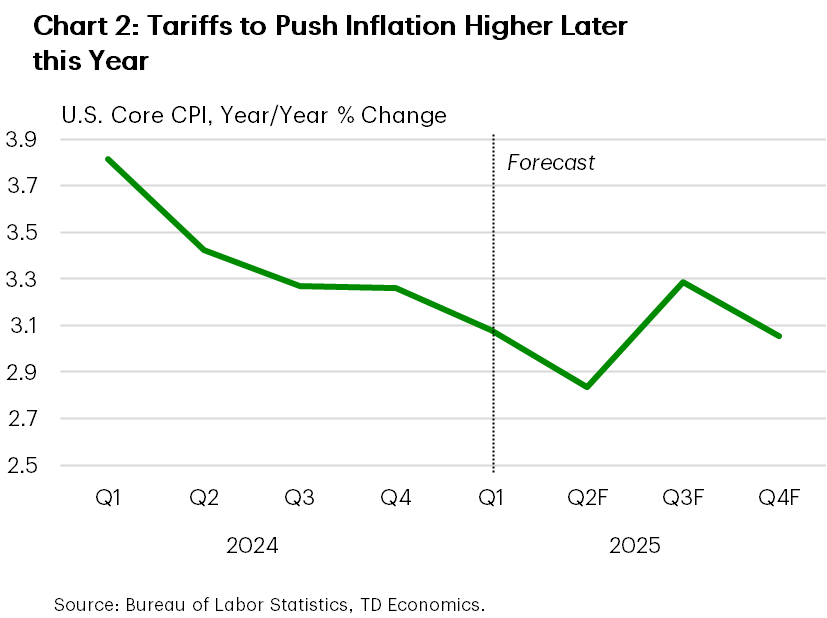

But that doesn’t mean they’re not coming. Over the coming months, inventory restocking will expose more firms to the tariffs, squeezing profit margins and leading to some price increases for consumer goods. Even assuming a mild passthrough to prices, where goods prices increase by just 3.5% by year-end, would likely be enough to push core measures of inflation up to the 3%-3.5% range over the coming quarters (Chart 2).

We’ll hear from the Federal Reserve next week, where it’s widely expected that they’ll keep the policy rate unchanged and continue to communicate a ‘wait-and-see’ approach. But investors will parse every word change of the statement and Powell’s press conference for signs of whether the recent softening in inflation has nudged policymakers any closer to reducing its policy rate.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of May 30th, 2025

Financial News Highlights

- The tariff news felt like a tennis match this week in financial news. Tariff threats on the EU were paused. Then a court struck down the IEEPA tariffs, only to have an appeal court say they could remain in place.

- The economic data showed that inflation pressures were steady through April, while consumer spending has been very volatile so far in 2025.

- President Trump also voiced his desire for rate cuts directly to the Fed Chair this week. Powell reinforced his message that the Fed will be guided by the data.

Tariff News Tennis Match Continues

Equity markets looked to end the week in the black as the tariff news tennis match seemed to net out on the good news side. The week started with a pause on Trump’s 50% tariff threat against the European Union, then a court struck down some of the Trump administrations’ tariffs before the appellate court deemed they could remain in place for now.

Equity markets looked to end the week in the black as the tariff news tennis match seemed to net out on the good news side. The week started with a pause on Trump’s 50% tariff threat against the European Union, then a court struck down some of the Trump administrations’ tariffs before the appellate court deemed they could remain in place for now.

A U.S. trade court invalidated the Trump administration’s use of the International Emergency Economic Powers Act (IEEPA) to levy tariffs. These tariffs include the Canada/Mexico/China “fentanyl” tariffs and the 10% “reciprocal” tariffs. The court ruling has no impact on sectoral tariffs, including those on steel & aluminum and autos. These court battles don’t make it any clearer what will happen with tariffs in the near-term. The administration has other tools they could use to implement tariffs, so this may just be a bump in the road.

The revisions to first quarter economic growth didn’t really change the narrative (see commentary). The slight contraction in the economy was due to a huge surge in imports, while the domestic economy was still running at a solid 2.5% pace. However, some of that growth was likely due to tariff front-running. These distortions make it harder to get a read on underlying momentum in the economy.

One potential warning sign in the first quarter data was a decline in corporate profits. The drop was seen in nonfinancial firms, which may be a signal that they are coming under pressure. However, April’s personal income data showed that income gains on the household side have been resilient. Incomes were boosted by the implementation of the Social Security Fairness Act, which provided a one-time lift. But even so, wages and salaries continue to grow at a healthy clip. Combined with softer spending growth, the personal savings rate ticked up to its highest level in a year, suggesting consumers have some gas in the tank.

Consumers did take a bit of a breather in April after a solid increase in outlays in March (Chart 1). Consumer spending has been quite volatile so far in 2025, whipsawed by natural disasters and swings in durable goods purchases on things like autos as they try to front run tariffs. This makes it difficult to discern a trend in consumer spending. Even so, we expect that weaker sentiment and a softer labor market ahead will cool the pace of spending in the coming quarters.

Consumers did take a bit of a breather in April after a solid increase in outlays in March (Chart 1). Consumer spending has been quite volatile so far in 2025, whipsawed by natural disasters and swings in durable goods purchases on things like autos as they try to front run tariffs. This makes it difficult to discern a trend in consumer spending. Even so, we expect that weaker sentiment and a softer labor market ahead will cool the pace of spending in the coming quarters.

The inflation news was steady-as-she goes in April (Chart 2). However, it is a bit early yet to see much inflation pressure from tariffs. We expect inflation will be lifted above 3% later this year as companies pass along higher tariffs to consumers.

President Trump met with Fed Chair Powell for the first time in his second term, reiterating his view that the Fed is making a mistake by not lowering interest rates. Powell stressed that policy decisions would be dependent on the economic data. The Fed minutes from their decision in early May suggested that they are in no hurry to cut rates as they wait for more clarity on the tariff front. Volatility is making it difficult to get clarity on the economic data these days. Add it all up, and the Fed’s wait and see approach is warranted for now.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of May 16th, 2025

Financial News Highlights

- U.S.-China trade tensions were toned down this week, with both countries agreeing to a temporary truce that would see some tariffs on each other’s goods come down substantially in financial news.

- Following a strong showing in March, retail sales barely grew in April. The details hinted at consumer efforts to get ahead of potential tariff-related price hikes.

- Housing starts managed to eke out some modest growth in April, but the gain was entirely concentrated in the smaller and more volatile multifamily sector.

Trade Tensions with China Simmer Down

Following the U.K. trade deal signed last week, the U.S. de-escalated its tariff fight with another key trade partner this week – China. Stock markets rejoiced on the news with the S&P 500 up almost 5% this week.

Following the U.K. trade deal signed last week, the U.S. de-escalated its tariff fight with another key trade partner this week – China. Stock markets rejoiced on the news with the S&P 500 up almost 5% this week.

The U.S. and China announced a temporary truce, which would see both nations significantly reduce their tariffs for 90 days, effective May 14th. U.S. tariffs on China would drop from 145% to 30%, while Chinese tariffs on U.S. goods would fall from 125% to 10%. China also agreed to ease its critical minerals export restrictions. This development marks a major step in the right direction. Still, it is early days in negotiations and there’s potential for trade tensions to flare up again should an agreement prove elusive. Additionally, some of the damage is already done, with elevated tariffs that were kept on for several weeks already disrupting trade patterns and setting the stage for potential price hikes ahead. Recognizing these risks, at a speech this week Fed Chair Powell noted that “we may be entering a period of more frequent, and potentially more persistent, supply shocks – a difficult challenge for the economy and for central banks”.

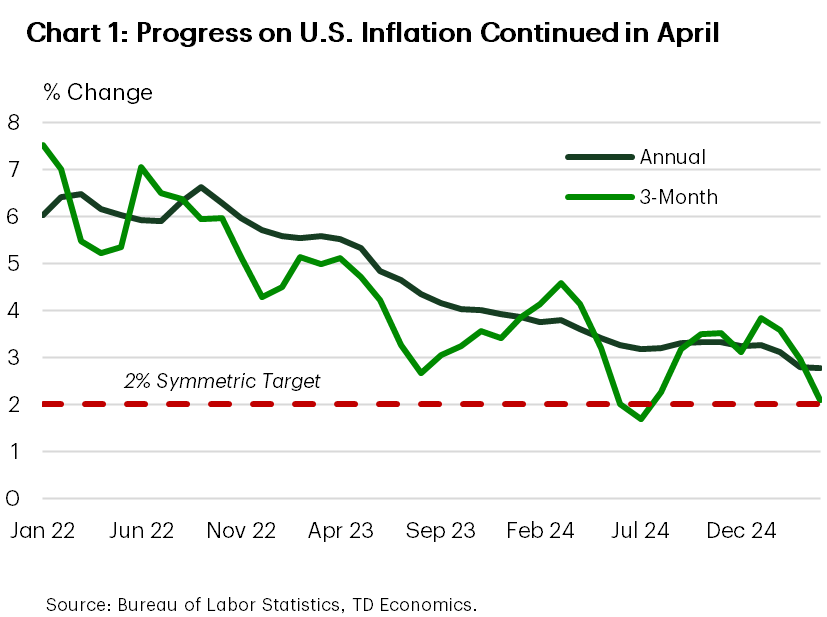

Up until April, inflation appeared to be moving in the right direction. Helped by a reduction in energy prices, total CPI inflation eased to 2.3% year-on-year (y/y) in April – the lowest level since 2021 in financial news. Meanwhile, core CPI held steady at 2.8% y/y, but managed to trend lower on a 3-month annualized basis (Chart 1). Still, this trend is unlikely to last. Citing pressure from tariffs, Walmart announced plans to start passing on tariff costs as early as this month. Other retailers are likely to follow, and consumers will soon start to feel the heat.

With respect to the consumer, following a strong finish to the first quarter, retail sales grew only modestly in April. Sales at motor vehicle and parts dealers edged lower (albeit from an elevated level), while sales at gasoline stations fell more noticeably in part due to lower gas prices. Despite this, a decent showing in a few other categories, including bars and restaurants, and building material stores helped provide some counterbalance.

With respect to the consumer, following a strong finish to the first quarter, retail sales grew only modestly in April. Sales at motor vehicle and parts dealers edged lower (albeit from an elevated level), while sales at gasoline stations fell more noticeably in part due to lower gas prices. Despite this, a decent showing in a few other categories, including bars and restaurants, and building material stores helped provide some counterbalance.

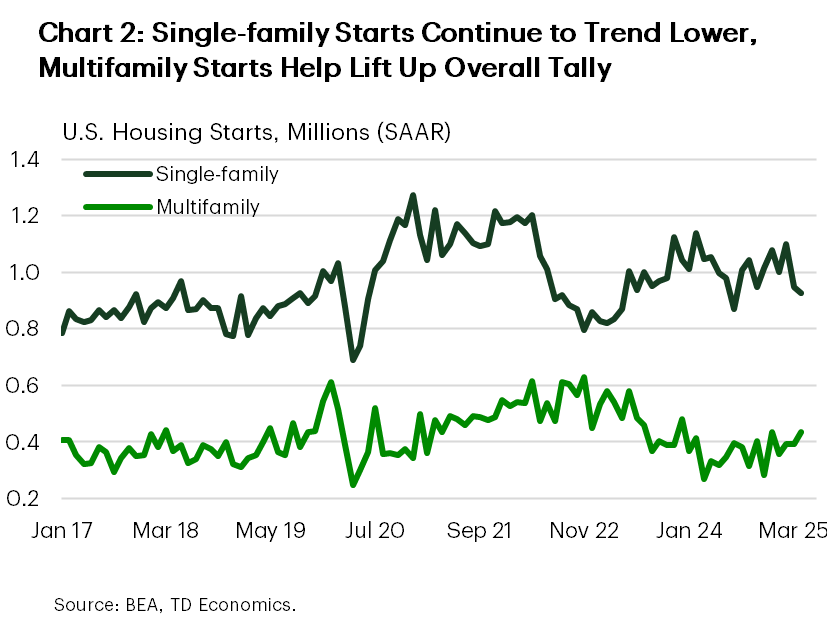

Pulling back the lens, last month’s retail spending data provided further evidence that consumers continued to front-run the tariffs by pulling forward purchases of some big ticket items. Meanwhile, ongoing gains in discretionary spending suggest that the consumer is managing to hold its own for now, despite downbeat sentiment. Housing starts also managed to eke out some modest growth in April (up 1.6% on the month), but under the hood, the details were mixed. Starts in the larger single-family sector continued to trend lower, with last month’s increase entirely stemming from gains in the smaller and more volatile multifamily segment (Chart 2).

All told, the de-escalation in the trade fight with China marks an important step in the right direction, and there could be more on the way, with President Trump today hinting at the potential for further de-escalation with other countries over the next 2-3 weeks. Still, this does not rule out additional flareups, and we are far from being out of the woods.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of May 9th, 2025

Financial News Highlights

- In financial news the U.S. announced a trade deal with the U.K. to reduce several product-specific tariffs, although the 10% reciprocal tariff faced by the U.K. remained in place.

- Formal trade negotiations with China are expected to begin this weekend in Switzerland, as the third largest trading partner of the U.S. remains subject to 145% tariffs.

- The Federal Reserve left interest rates unchanged for the third time this year. Chair Powell noted that it would take time to discern the effects of tariffs on the economy.

The First of Many?

The first full week of May looked like it may provide a modest respite for financial markets, as economic data releases were limited and the Federal Reserve’s decision on Wednesday was short on surprises. However, this proved to be short-lived as the White House announced a preliminary trade deal with the U.K. on Thursday. The S&P 500 ended the week roughly unchanged at time of writing, while the 10-year U.S. Treasury yield rose 4 basis points to 4.36%.

The first full week of May looked like it may provide a modest respite for financial markets, as economic data releases were limited and the Federal Reserve’s decision on Wednesday was short on surprises. However, this proved to be short-lived as the White House announced a preliminary trade deal with the U.K. on Thursday. The S&P 500 ended the week roughly unchanged at time of writing, while the 10-year U.S. Treasury yield rose 4 basis points to 4.36%.

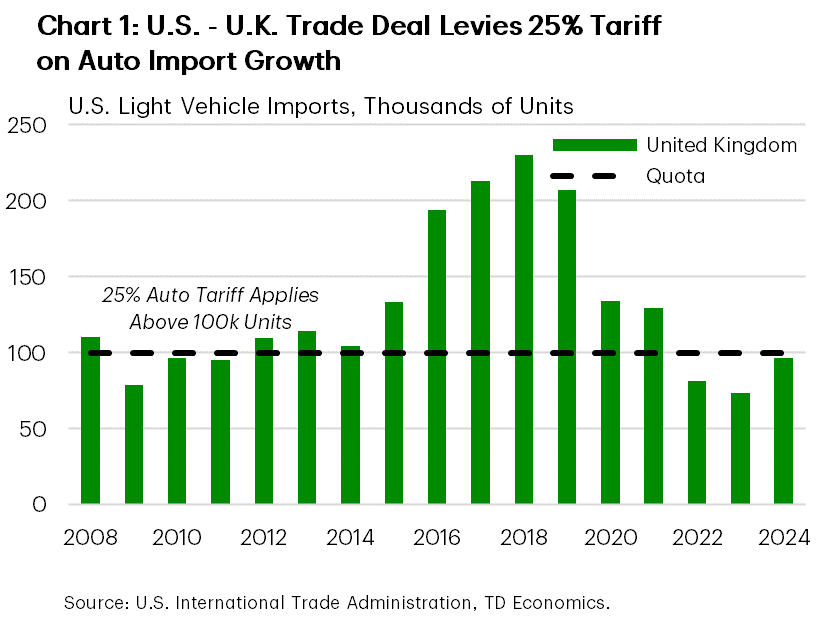

The preliminary trade deal between the U.S. and U.K. (see here), included a full exemption on Section 232 steel and aluminum tariffs for the U.K., in addition to an annual exemption on automotive tariffs for the first 100k units imported (Chart 1). The market reaction to the agreement was relatively tame, as the 10% baseline reciprocal tariff remained in effect. The President noted that this would likely be the global floor for reciprocal tariffs, and that other nations may see levels above this even after negotiations have concluded. It is unclear whether this would be acceptable to other nations. If they take a harder stance during upcoming negotiations, it could delay a broader resolution to the current state of elevated trade tensions.

The EU also outlined a list of goods this week that would be subject to retaliatory tariffs in financial news. The list covers nearly a third of U.S. exports to the region. These tariffs would be levied if negotiations do not result in “a mutually beneficial outcome and the removal of U.S. tariffs”. Chinese officials also called on the U.S. to “be prepared to correct its erroneous actions and cancel its unilateral tariff increases”, ahead of the planned start of formal negotiations with the U.S. this weekend. Early on Friday the President floated the idea of lowering the tariff rate on China to 80%, but no final decision has been made. With less than two months until the 90-day suspension of U.S. reciprocal tariffs expires and dozens of deals yet to be made, time will remain of the essence on the trade front in the weeks ahead.

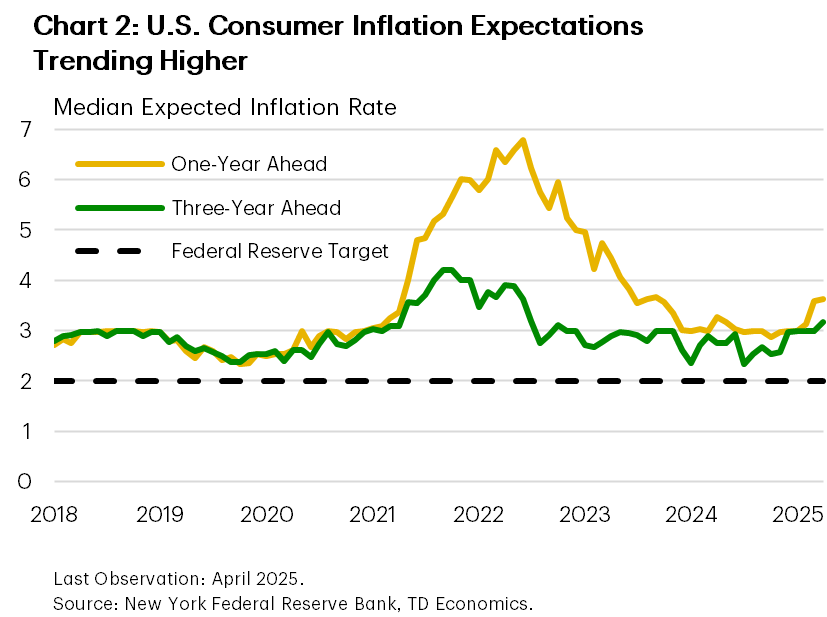

The Federal Reserve pointed to the clouds hanging over the economic outlook in its rate decision on Wednesday. It was the third meeting in a row where the FOMC left the federal funds rate unchanged. During his press conference, Chair Powell highlighted the likelihood that current trade policies would push the unemployment rate and inflation to deviate from the Fed’s dual mandate. However, he also noted that uncertainty remains elevated with respect to the magnitude of the deviation, meriting caution in monetary policy decisions at this time. With survey-based measures of inflation expectations remaining elevated in April (Chart 2), the Fed’s caution would appear prudent at this time.

The Federal Reserve pointed to the clouds hanging over the economic outlook in its rate decision on Wednesday. It was the third meeting in a row where the FOMC left the federal funds rate unchanged. During his press conference, Chair Powell highlighted the likelihood that current trade policies would push the unemployment rate and inflation to deviate from the Fed’s dual mandate. However, he also noted that uncertainty remains elevated with respect to the magnitude of the deviation, meriting caution in monetary policy decisions at this time. With survey-based measures of inflation expectations remaining elevated in April (Chart 2), the Fed’s caution would appear prudent at this time.

Next week, we’ll receive a first look at inflation data for April with the CPI data release, in addition to April retail sales. Although neither is expected to be materially influenced by tariff impacts yet, they will provide a pulse check on consumer and price trends. Also on the docket for next week is the reconciliation bill markup for the House Ways & Means Committee, which could provide insight on the specific tax cut provisions being considered by Congress. Although fiscal policy may not fully offset the influence of tariffs on the economy this year, it could help to prevent a more material slowdown.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of May 2nd, 2025

Financial News Highlights

- The U.S. administration is scheduled to change another tariff rule tonight, ending the so-called de minimis provision which has exempted small packages from most duties in the past in financial news.

- U.S. GDP contracted in the first quarter of 2025, ending a long streak of expansion. The contraction was mostly owed to a surge in imports, as consumers and businesses tried to get ahead of tariffs.

- The U.S. payrolls report for April came in stronger than expected, revealing little impact to the job market from tariffs so far.

Another Week, Another New Tariff

The U.S. economy has been showing resilience to tariffs so far, but will be increasingly pressure tested going forward under the weight of multiple tracks of tariffs in financial news. Tariffs, especially the very high 145 percent levy on imports from China, are about to start hitting even more goods; tonight is the deadline for the so-called de minimis provision to end. Under de minimis rules, small packages of $800 or less imported from China to the U.S. are exempt from tariffs. This provision has meant that e-commerce retailers that sell clothing and other goods online directly to U.S. consumers were able to do so without being affected by tariffs. Over 1.25 billion shipments entered the U.S. in 2024 under the de minimis provision, and its end will mean price increases for a wide swath of consumers. Some of the most affected companies, such as Temu and Shein, have already indicated some changes to their operations because of the change to de minimis rules; these changes could include price increases for customers, shifting some of the sourcing for U.S. sales away from China, and as a consequence possibly seeing their U.S. business shrink. These measures are set to occur as progress on removing tariffs remains elusive, though we did see indications of a willingness to negotiate from both China and the EU late this week.

The U.S. economy has been showing resilience to tariffs so far, but will be increasingly pressure tested going forward under the weight of multiple tracks of tariffs in financial news. Tariffs, especially the very high 145 percent levy on imports from China, are about to start hitting even more goods; tonight is the deadline for the so-called de minimis provision to end. Under de minimis rules, small packages of $800 or less imported from China to the U.S. are exempt from tariffs. This provision has meant that e-commerce retailers that sell clothing and other goods online directly to U.S. consumers were able to do so without being affected by tariffs. Over 1.25 billion shipments entered the U.S. in 2024 under the de minimis provision, and its end will mean price increases for a wide swath of consumers. Some of the most affected companies, such as Temu and Shein, have already indicated some changes to their operations because of the change to de minimis rules; these changes could include price increases for customers, shifting some of the sourcing for U.S. sales away from China, and as a consequence possibly seeing their U.S. business shrink. These measures are set to occur as progress on removing tariffs remains elusive, though we did see indications of a willingness to negotiate from both China and the EU late this week.

We long expected that roll-out of U.S. tariffs would create distortions in the data, notably the natural response of many U.S. businesses and consumers to get ahead of the higher levies. This week’s advance estimate of U.S. GDP growth for the first quarter of 2025 confirmed our expectation – U.S. GDP shrank in the quarter, weighed down heavily by a massive surge in imports ahead of tariffs being put in place, much of the import surge seemingly for companies to stockpile inventories. Inflation was also up for the quarter, but March showed some slowing from earlier in the year. Recent inflation readings are still above the Federal Reserve’s target, however, so we expect this mild softening to be received with great caution.

The vast majority of tariffs were put in place after April 2, so all of this data is just a warm-up, so to speak. Most of this 1st-quarter data is warped by expectations of tariffs in the future, rather than being an indication of underlying trends. The real question of how economic activity is holding up is going to come through the data after April 2. This morning’s jobs report for April, the first such data, was surprisingly resilient, and the unemployment rate remained unchanged at a fairly low 4.2 percent. We also saw April data for vehicle sales this morning come in strong, in part because dealers still have inventory that predates the auto tariffs. But that is still two points of hard data showing that activity did not take a big hit in April.

The vast majority of tariffs were put in place after April 2, so all of this data is just a warm-up, so to speak. Most of this 1st-quarter data is warped by expectations of tariffs in the future, rather than being an indication of underlying trends. The real question of how economic activity is holding up is going to come through the data after April 2. This morning’s jobs report for April, the first such data, was surprisingly resilient, and the unemployment rate remained unchanged at a fairly low 4.2 percent. We also saw April data for vehicle sales this morning come in strong, in part because dealers still have inventory that predates the auto tariffs. But that is still two points of hard data showing that activity did not take a big hit in April.

This week leaves us back in wait-and-see mode, as we have still seen very little data since tariffs were put in place. The economy has to pass through another deadline for tariffs to kick in tonight, and those will also take some time to filter through the economy. The Federal Reserve is set to meet next week, and we expect the central bank is still searching for more clarity on the outlook before contemplating rate cuts. Futures markets had been holding out hope for a June cut, but after today’s jobs report, odds have been dialed back to around 40%. However, given the expectation that a weaker economy will ultimately trump higher inflation as the Fed’s number one concern, investors are still anticipating between 3-4 cuts by year-end.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of April 25th, 2025

Financial News Highlights

- Trade tensions between the world’s two largest economies simmered this week, with the U.S. administration hinting that the tariffs on China would likely be lowered in the very near future in financial news.

- But President Trump appeared frustrated with the lack of progress among other countries, and threatened to reimpose the reciprocal tariffs in the coming weeks if trade deals weren’t signed.

- Amidst all the uncertainty, the housing recovery appears to be on hold. Existing home sales declined to a six-month low in March.

Searching for the Signal Amidst A Lot Of Noise

Disentangling the signal from the noise on U.S. trade matters is becoming an increasingly difficult task. This week, President Trump and U.S. Treasury Secretary Scott Bessent both called out the tariffs on China as being “too high”. At 145%, Bessent said trade with China becomes “unsustainable” and that he expects the current situation to de-escalate in the “very near future”. China appears open to negotiations and even went as far as exempting some U.S. goods from its retaliatory tariffs. The abrupt U-turn in the administration’s tone alongside President Trump’s assurance that he will not remove Fed Chair Powell, helped to fuel a mid-week rally in U.S. equities, with the S&P 500 ending the week up 3.5%. But investors remained skeptical of whether the move to de-escalate was the beginning of a broader pivot or simply backpedaling on the overly punitive levies imposed on China given the significant economic repercussions.

Disentangling the signal from the noise on U.S. trade matters is becoming an increasingly difficult task. This week, President Trump and U.S. Treasury Secretary Scott Bessent both called out the tariffs on China as being “too high”. At 145%, Bessent said trade with China becomes “unsustainable” and that he expects the current situation to de-escalate in the “very near future”. China appears open to negotiations and even went as far as exempting some U.S. goods from its retaliatory tariffs. The abrupt U-turn in the administration’s tone alongside President Trump’s assurance that he will not remove Fed Chair Powell, helped to fuel a mid-week rally in U.S. equities, with the S&P 500 ending the week up 3.5%. But investors remained skeptical of whether the move to de-escalate was the beginning of a broader pivot or simply backpedaling on the overly punitive levies imposed on China given the significant economic repercussions.

Despite claims of over 90 countries having offered to negotiate trade terms, President Trump appears to be growing frustrated with the lack of progress made on reaching deals. He even went as far threatening to re-impose the “reciprocal” tariffs on some countries over the coming weeks if trade deals weren’t signed.

But even if there’s a big push on trade negotiations over the coming weeks, at least some economic damage has already been done. In the April release of the Federal Reserve’s Beige Book, several districts noted a considerable worsening in the economic outlook amid heightened uncertainty stemming from tariffs in financial news. Spending on both business and leisure travel were down, with some districts seeing an outright decline in international visitors. On inflation, many businesses noted that they’re already seeing input costs rise and that they expect to pass-on at least some of the additional costs to consumers. But this may not be possible for some consumer-facing sectors, who are already reporting more tepid demand.

Estimates done by Reuters suggest that of the S&P 500 companies who have already reported quarterly earnings, over 90% have mentioned tariff risks in their earnings transcripts. This is more than double what was mentioned the prior quarter and underscores how today’s uncertainty is touching nearly all industries. This does not bode well for capital spending.

Estimates done by Reuters suggest that of the S&P 500 companies who have already reported quarterly earnings, over 90% have mentioned tariff risks in their earnings transcripts. This is more than double what was mentioned the prior quarter and underscores how today’s uncertainty is touching nearly all industries. This does not bode well for capital spending.

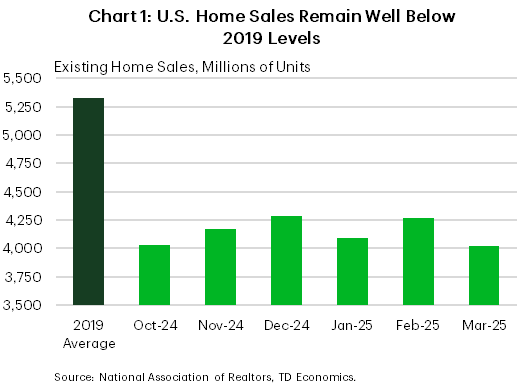

The housing recovery is also looking to be on hold. Existing home sales declined 5.9% m/m in March, falling to a six-month low of 4.0 million units (Chart 1). With mortgage rates again within spitting distance of 7%, and households increasingly worried about employment prospects, we’re likely to see a further pullback in sales activity over the coming months. Construction activity was also sharply lower in March, amid elevated trade uncertainty and higher input costs. Homebuilder confidence for April remained soft, suggesting little rebound in near future.

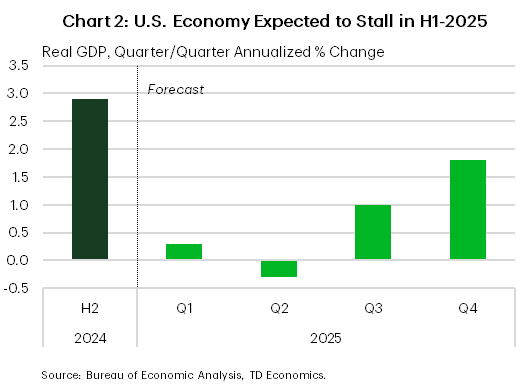

Our current tracking for first quarter real GDP (released April 30th) suggests economic growth grew by just 0.3% annualized after expanding by an above trend pace of 2.9% through the second half of 2024 (Chart 2). But the GDP release will play second fiddle to next week’s more timely April jobs report. Expectations are that the economy added 130k jobs in April, a meaningful stepdown from March’s 228k pace.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of April 11th, 2025

Financial News Highlights

- Market sentiment soured earlier this week as ‘reciprocal’ tariffs went into effect in financial news. Equities sold off initially, but so did Treasuries, with the 10-year Treasury yield up sharply on the week.

- A decision to ease U.S. tariff measures on most countries targeted last week, while increasing tariffs on China, sent markets on a rollercoaster.

- Inflation came in lower than anticipated in March, with core CPI easing to 2.8% year-on-year from 3.1% previously.

Tariff Rollercoaster Continues, Trade Fight with China Escalates

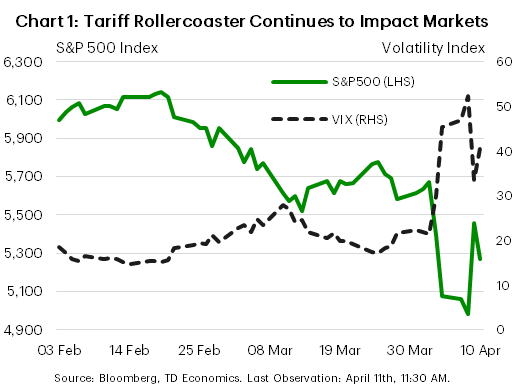

Another tumultuous week has followed for financial markets. On the heels of last week’s announcement that the U.S. would implement higher reciprocal tariffs on a number of countries, some appeared to have reached out for negotiation, while a few others announced their own countermeasures. What stood out was China’s commensurate retaliation to the 34% additional U.S. tariff on Chinese goods in financial news. But this was only the beginning, with the trade fight escalating throughout the week. As higher reciprocal tariffs came into effect, equity markets sold off. Normally when this happens, Treasuries (considered a safe-haven asset) tend to rally. But, in a very concerning move, Treasuries sold off too. Yields (which move opposite to bond prices) shot higher. The dollar also lost considerable ground against a basket of foreign currencies. Before long, the White House appeared to extend an olive branch. In a surprising move, Pres. Trump announced a 90 day pause to last week’s reciprocal tariffs, while also lowering the country-specific rate to a universal 10% for all targeted countries, except for China. Tariffs on the latter were jacked up further. Stock markets rejoiced initially, staging a sharp recovery on Wednesday. But when it came to yields and the dollar, the weak trends described above resumed later in the week (Chart 1).

Another tumultuous week has followed for financial markets. On the heels of last week’s announcement that the U.S. would implement higher reciprocal tariffs on a number of countries, some appeared to have reached out for negotiation, while a few others announced their own countermeasures. What stood out was China’s commensurate retaliation to the 34% additional U.S. tariff on Chinese goods in financial news. But this was only the beginning, with the trade fight escalating throughout the week. As higher reciprocal tariffs came into effect, equity markets sold off. Normally when this happens, Treasuries (considered a safe-haven asset) tend to rally. But, in a very concerning move, Treasuries sold off too. Yields (which move opposite to bond prices) shot higher. The dollar also lost considerable ground against a basket of foreign currencies. Before long, the White House appeared to extend an olive branch. In a surprising move, Pres. Trump announced a 90 day pause to last week’s reciprocal tariffs, while also lowering the country-specific rate to a universal 10% for all targeted countries, except for China. Tariffs on the latter were jacked up further. Stock markets rejoiced initially, staging a sharp recovery on Wednesday. But when it came to yields and the dollar, the weak trends described above resumed later in the week (Chart 1).

Pulling back the lens on the many twists and turns from this week’s events, one thing is clear – the U.S. is softening its tariff stance with most partners targeted last week, but is tightening the screws on China. The White House has clarified that the tariff increases on China so far add up to 145%, while this morning China announced it will increase retaliatory tariffs on U.S. goods to 125%. If tariffs were to hold at these high levels for a while, a large chunk of trade with China would effectively be cut off. While China’s economy would undoubtedly take a hit, as its $439 billion worth of goods sent to the U.S. last year dwindle to something much lower, there  will be major consequences at home too. Reduced access to the Chinese market for U.S. exporters is a first. But perhaps a more concerning aspect is the prospect of product shortages, along with higher prices for inelastic products that can’t be sourced from elsewhere in short order. Domestic production cannot fill the void that will be left by China over the near-to-medium term. In this vein, the trade war will also remap supply chains, with the U.S. inclined to seek product substitutes from other countries, while Chinese exporters will seek to expand in other markets, such as in Europe.

will be major consequences at home too. Reduced access to the Chinese market for U.S. exporters is a first. But perhaps a more concerning aspect is the prospect of product shortages, along with higher prices for inelastic products that can’t be sourced from elsewhere in short order. Domestic production cannot fill the void that will be left by China over the near-to-medium term. In this vein, the trade war will also remap supply chains, with the U.S. inclined to seek product substitutes from other countries, while Chinese exporters will seek to expand in other markets, such as in Europe.

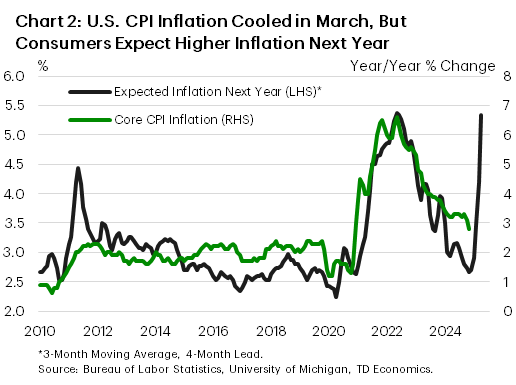

Apart from leaving a mark on financial markets, trade uncertainty is also weighing on consumers and businesses, with the NFIB small business confidence measure continuing to trend lower in March. On a more positive note, producer prices, and inflation as measured by CPI, both came in softer than anticipated last month. Lower energy prices dragged down total CPI inflation (2.4% year-on-year (y/y)), but core inflation also eased, cooling to 2.8% y/y from 3.1% previously. Still, considering the tariffs and the fact that consumers are positioning for higher inflation, this trend looks set to reverse course soon (Chart 2). This leaves the Fed in a difficult position. Minutes from the mid-March FOMC meeting suggest that the central bank wasn’t ready to alter its course yet, with Fed officials leaning against preemptive rate cuts. While a lot has changed in the last three weeks, messaging from Fed officials appears consistent, with several speeches this week driving home the point that the bar for rate cuts remains high.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of March 28th, 2025

Financial News Highlights

- This week’s announcement of new automobile tariffs caught markets by surprise in financial news. But now all eyes are focused on updates on reciprocal tariffs next week.

- The U.S. economy had been humming, but as uncertainty ramps up and consumer confidence continues to dip, the risks of a slowdown are building.

- Worryingly, inflation momentum picked up again in February suggesting price growth could be stickier than anticipated.

Waiting for April 2nd

After steadily rallying since mid-March, markets took a step back this week when new U.S. tariffs on automobiles and parts were announced. The news comes ahead of next week’s much anticipated update on reciprocal tariffs that are expected to cover major U.S. trading partners. In the meantime, February’s Personal Income and Outlays report showed that core inflation picked up again, while spending growth failed to recover from last month’s decline in financial news. The U.S. economy had been humming, but as uncertainty ramps up and consumer confidence continues to dip, the risks of a slowdown are building. All eyes are now firmly focused on next week’s tariff announcement for more clarity on the operating environment going forward.

After steadily rallying since mid-March, markets took a step back this week when new U.S. tariffs on automobiles and parts were announced. The news comes ahead of next week’s much anticipated update on reciprocal tariffs that are expected to cover major U.S. trading partners. In the meantime, February’s Personal Income and Outlays report showed that core inflation picked up again, while spending growth failed to recover from last month’s decline in financial news. The U.S. economy had been humming, but as uncertainty ramps up and consumer confidence continues to dip, the risks of a slowdown are building. All eyes are now firmly focused on next week’s tariff announcement for more clarity on the operating environment going forward.

The big news this week was President Trump’s announcement of new tariffs on automobile imports of 25%, set to take effect on April 3rd. This comes ahead of the expected announcement next week on reciprocal tariffs that markets had been bracing for. At the time of writing, most countries had held off on any new retaliation, likely opting to wait and see what’s in store from next week’s announcements before proceeding. As we wrote, the full impact of the autos tariffs will depend on their duration and how much of the cost firms pass along to their customers.

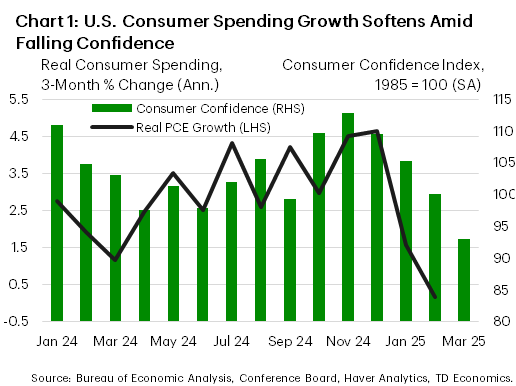

Yet, while we await more clarity on the import taxes, consumer confidence continues to dip, and the darkening moods appear to be flowing through to behavior. The Conference Board measure of consumer confidence has fallen to its lowest level since early-2021. With sinking sentiment, an adjustment in consumer spending appears to be unfolding as real outlays in February failed to recover from the tumble they took in January (Chart 1). This leaves the three-month annualized change in real consumer spending at 0.2%, well short of the 4.6% clip recorded in December. First quarter consumer spending is now tracking only a 0.5% annualized pace, a downgrade from our recent forecast. Importantly, the pullback in real spending is coming at a time of still-healthy income growth, so with the savings rate ticking up to 4.6% (its highest level since June of last year), this suggests that some precautionary savings could be taking place.

Yet, while we await more clarity on the import taxes, consumer confidence continues to dip, and the darkening moods appear to be flowing through to behavior. The Conference Board measure of consumer confidence has fallen to its lowest level since early-2021. With sinking sentiment, an adjustment in consumer spending appears to be unfolding as real outlays in February failed to recover from the tumble they took in January (Chart 1). This leaves the three-month annualized change in real consumer spending at 0.2%, well short of the 4.6% clip recorded in December. First quarter consumer spending is now tracking only a 0.5% annualized pace, a downgrade from our recent forecast. Importantly, the pullback in real spending is coming at a time of still-healthy income growth, so with the savings rate ticking up to 4.6% (its highest level since June of last year), this suggests that some precautionary savings could be taking place.

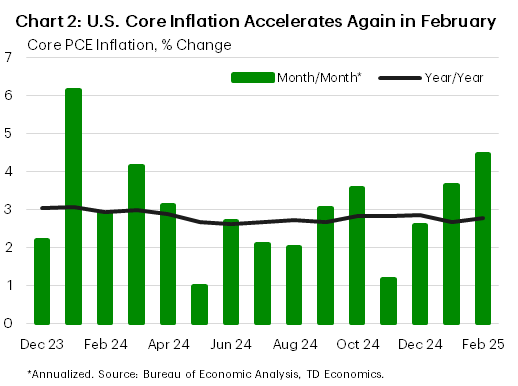

Part of the story is that inflation looks to be heating up again. Higher price growth is cutting into consumers’ purchasing power, restraining real outlays. The core personal consumption expenditures price index saw its biggest monthly gain since January of last year, taking the annual pace to 2.8% (Chart 2). Inflation momentum appears to be gaining steam, and consumer are noticing. Inflation expectations for the year ahead jumped to their highest levels since late-2022.

For the Fed, the combination of softening growth and rising inflation are troublesome. Yet, what could make it more complicated is if inflation expectations continue to rise, creating a self-reinforcing loop of greater price pressures. For now, though, we wait for next week for more clarity on the next set of tariffs to better guide our assumptions around the forecast.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.