Financial News for the Week of November 15th, 2024

Financial News Highlights

- Progress on the inflation front appears to have stalled in financial news. Core CPI inflation held steady in October, while the trend over the past three months has accelerated.

- October retail sales were also solid, putting consumer spending in the fourth quarter on a very solid footing.

- Chair Powell moved markets on Thursday by saying that the Fed may not be in a hurry to cut rates. This sent Treasury yields and the dollar moderately higher, while weighing on equities.

Inflation Progress Stalls, Fed in No Hurry to Cut Rates

Political developments continued to dominate the limelight this week. Republicans retained a slim majority in the House, cementing control over both chambers of Congress and the Presidency. In the meantime, President-elect Trump is hitting the ground running, announcing cabinet appointments and White House staff positions. The choices reinforce the campaign themes of slower immigration, along with a tougher stance on China and trade. Amidst the political noise, equity markets remained sanguine early in the week, but did lose considerable steam at the end of the week on growing signs that the Fed may not be in a rush to cut rates. Chief among these are signs of slowing progress on the inflation front.

Political developments continued to dominate the limelight this week. Republicans retained a slim majority in the House, cementing control over both chambers of Congress and the Presidency. In the meantime, President-elect Trump is hitting the ground running, announcing cabinet appointments and White House staff positions. The choices reinforce the campaign themes of slower immigration, along with a tougher stance on China and trade. Amidst the political noise, equity markets remained sanguine early in the week, but did lose considerable steam at the end of the week on growing signs that the Fed may not be in a rush to cut rates. Chief among these are signs of slowing progress on the inflation front.

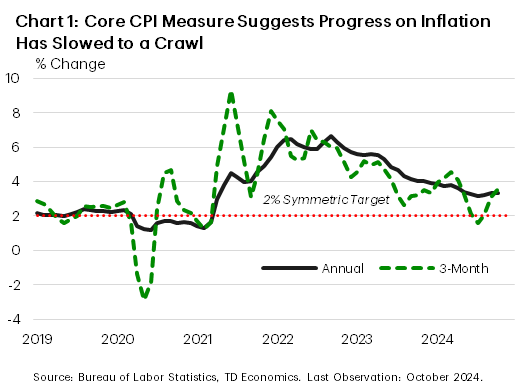

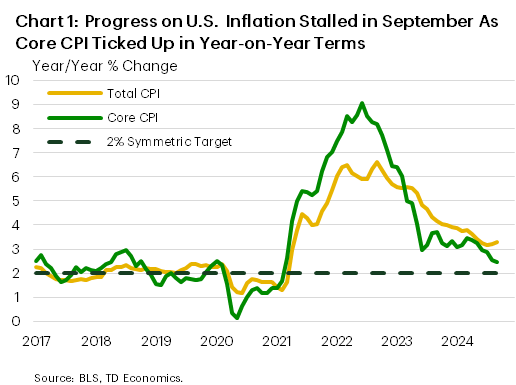

Headline inflation as tracked by the consumer price index (CPI) ticked up in October (see commentary). Inflation pressures were also a little hot under the collar in the core measure, which rose 0.3% m/m for the third consecutive month. Core inflation held steady at 3.3% on a year-on-year basis in October, but the trend over the past three months heated up (Chart 1). Services inflation is showing signs of stickiness, with price growth for core services holding at 4.8% y/y for the second month in a row. This suggests that after some fast initial progress, the final stage of getting inflation back down to the Fed’s 2% target may indeed be a long slog. Producer prices drove home the same point, with growth in core producer price inflation accelerating to 3.1% y/y in October from 2.9% in the month prior.

These latest inflationary trends are not what the Fed wants to see. At a speech this week, Fed Chair Powell noted that “the economy is not sending any signals that we need to be in a hurry to lower rates”, adding that “the strength we are currently seeing in the economy gives us the ability to approach our decisions carefully”. A relatively healthy October retail sales report released on Friday lends support to that latter point. Helped along by an outsized gain in autos, decent growth in retail sales in October built on a healthy September gain to provide a solid start for consumer spending in the fourth quarter, which looks to be tracking 3.3% annualized, up from a few ticks under 3% previously.

These latest inflationary trends are not what the Fed wants to see. At a speech this week, Fed Chair Powell noted that “the economy is not sending any signals that we need to be in a hurry to lower rates”, adding that “the strength we are currently seeing in the economy gives us the ability to approach our decisions carefully”. A relatively healthy October retail sales report released on Friday lends support to that latter point. Helped along by an outsized gain in autos, decent growth in retail sales in October built on a healthy September gain to provide a solid start for consumer spending in the fourth quarter, which looks to be tracking 3.3% annualized, up from a few ticks under 3% previously.

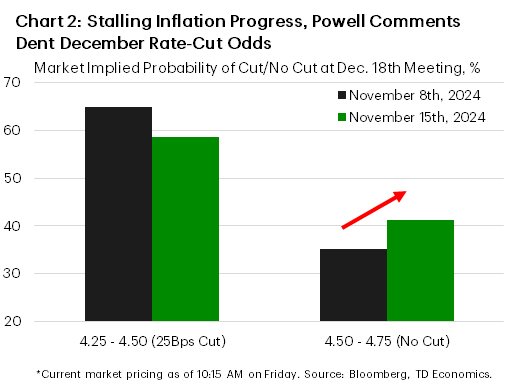

The inflation data, combined with Powell’s comments appeared to move markets, sending yields and the dollar moderately higher, while taking a toll on equities. Market odds for the Fed to take a pause on rate cuts have surged higher in recent days, with a probability of a little over 40% (Chart 2). The next payrolls report should be pivotal for the Fed heading into the December meeting, but given that it may continue to show volatility from one-off factors (i.e., recent hurricanes), the Fed will still have its work cut out for it in trying to ascertain the underlying strength in the labor market.

Next week’s economic calendar sees updates on housing in October, which are not likely to show the impact from the recent upswing in mortgage rates yet. The starts data could be messy due to hurricane impacts, while existing home sales are still expected to be solid.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of November 1st, 2024

Financial News Highlights

- The U.S. economy expanded by a robust 2.8% quarter-on-quarter (annualized) in the third quarter, only a touch slower than the 3% pace seen in Q2 in financial news.

- Growth in both income and consumer spending picked up in September while core PCE inflation held steady at 2.7% y/y.

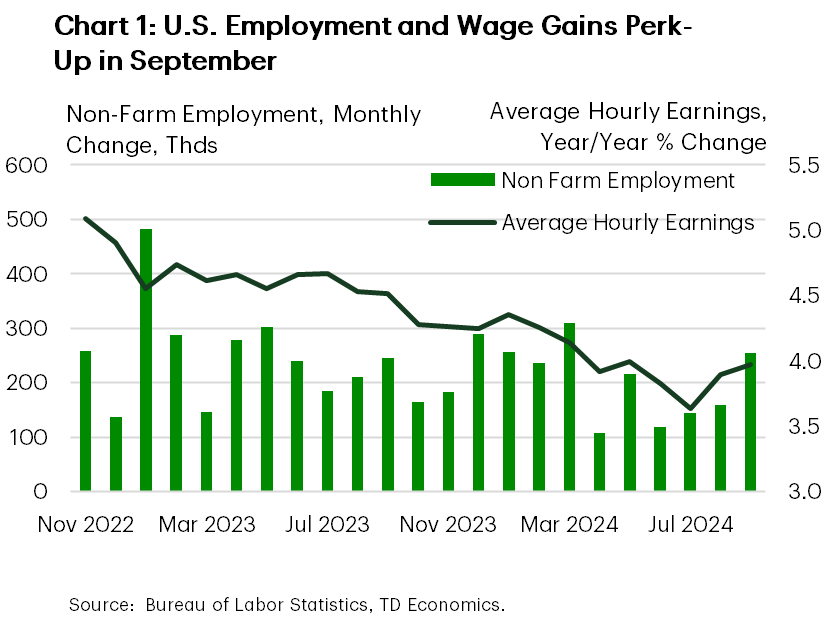

- Employment was essentially flat in October, with the economy adding a meager 12k jobs – well below the already-low 100k consensus estimate. The ongoing Boeing strike and disruptions related to Hurricanes Helene and Milton both weighed on the headline.

The U.S. GDP data delivers treats, but the payrolls report plays tricks

Next week all eyes will be on the U.S. elections and the Federal Reserve meeting. However, this week the focus has been on the health of the U.S. economy – an important reference point for both presidential candidates and the Fed.

Next week all eyes will be on the U.S. elections and the Federal Reserve meeting. However, this week the focus has been on the health of the U.S. economy – an important reference point for both presidential candidates and the Fed.

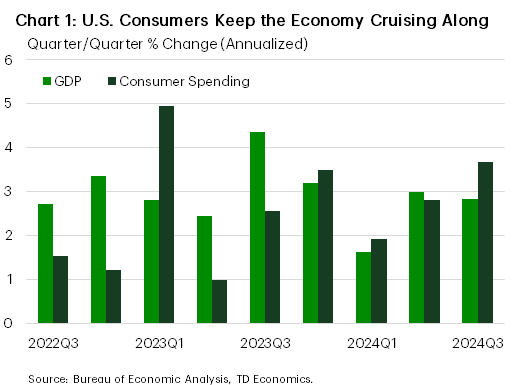

Wednesday’s advanced GDP report showed that the U.S. economy is alive and well. Coming on the heels of the solid 3% gain in Q2, the economy expanded by 2.8% (quarter-over-quarter annualized) in Q3. Consumers were the belle of the ball, with spending accelerating to 3.7%, or the fastest pace since Q1 2023 (Chart 1).

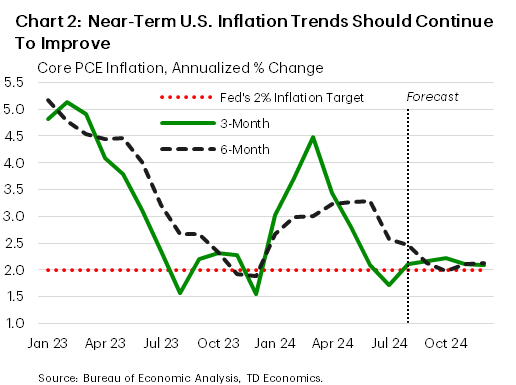

This ongoing resilience was further echoed in September’s personal income and spending report. It showed that spending increased by 0.5% m/m in September, outpacing income and indicating that consumers kept their purse strings open as Q3 wrapped up in financial news. Lower prices at the pump in recent weeks may have boosted confidence, giving consumers some reprieve from the ever-rising prices elsewhere. On that front, core PCE deflator – which excludes food and energy – rose 0.3% m/m in September. This held the twelve-month change steady at 2.7% for the third consecutive month, but this was largely due to “base effects”. Importantly, the 3-and-6-month annualized rates of change sit just above the Fed’s 2% inflation target, suggesting we’re likely to see more downward pressure on the year-ago measure in the months ahead.

As we noted in a recent report, there are several reasons consumers may have more momentum than previously anticipated, such as a notable upgrade to personal income in first half of 2024 and a larger buffer of savings. However, the savings cushion is quickly dwindling, with the personal saving rate having now declined for three consecutive months. This suggests we’re likely to see some moderation in consumer spending to something more consistent with a trend-like pace of around 2% in the months ahead.

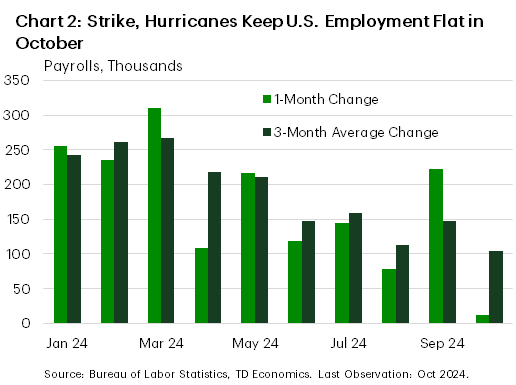

On that note, October’s payroll report was expected to be a weak one, but still surprised to the downside. The economy added just 12k jobs in October, well below the expectation for a 100k gain, while. Adding to the disappointment, downward revisions shaved 112k from the two prior months’ gains. The ongoing Boeing strike helped to cut over 40k from the headline number in October, while Hurricanes Helene and Milton also likely had a heavy hand weighing down the payrolls figure.

On that note, October’s payroll report was expected to be a weak one, but still surprised to the downside. The economy added just 12k jobs in October, well below the expectation for a 100k gain, while. Adding to the disappointment, downward revisions shaved 112k from the two prior months’ gains. The ongoing Boeing strike helped to cut over 40k from the headline number in October, while Hurricanes Helene and Milton also likely had a heavy hand weighing down the payrolls figure.

As a result, the Fed will likely look through October’s noisy employment data, and instead focus more on the broader trends showing that the labor market is decelerating but not necessarily deteriorating. Moreover, with the Fed’s preferred wage metric – the Employment Cost Index – showing wage pressures now growing at a pace roughly consistent with 2% inflation, the FOMC should have all the confidence they need to continue to gradually reduce the policy rate. We expect the Fed to cut by 25 basis-points at next week’s meeting. While this decision seems almost certain, the U.S. elections remain a wild card, promising to keep everyone on edge until the final votes are tallied.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of October 25th, 2024

Financial News Highlights

- U.S. Treasury yields continued to rise as the race for the White House tightened, leading to elevated uncertainty regarding the future path of fiscal policy in financial news.

- Federal Reserve speakers this week noted that further reductions in interest rates would be warranted, although incoming data supported a cautious approach.

- Existing home sales fell to a fourteen year low in September. Elevated interest rates, combined with expectations for lower rates moving forward, worked to keep demand subdued.

Countdown to Election Day

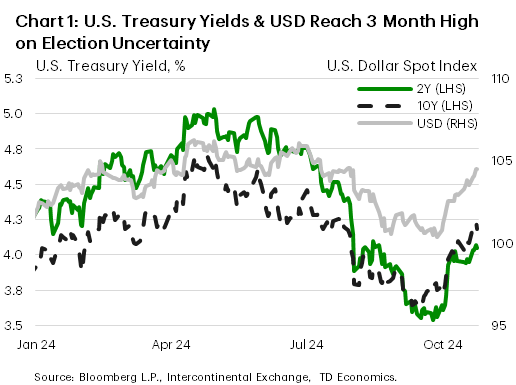

One of the most anticipated global events of 2024 is now nearly a week away. As financial markets anxiously await the outcome of the U.S. presidential and congressional elections, we have seen U.S. Treasury yields and the U.S. dollar rise to three-month highs (Chart 1). The uptick which began earlier this month was initially incited by stronger-than-expected economic data, but recent movements have also likely been driven by the narrowing in the polls for the U.S. presidential election. Given that the election will determine the path of fiscal policy moving forward, and by extension monetary policy, uncertainty related to the outcome is likely to remain a weight on financial markets through to November 5th.

One of the most anticipated global events of 2024 is now nearly a week away. As financial markets anxiously await the outcome of the U.S. presidential and congressional elections, we have seen U.S. Treasury yields and the U.S. dollar rise to three-month highs (Chart 1). The uptick which began earlier this month was initially incited by stronger-than-expected economic data, but recent movements have also likely been driven by the narrowing in the polls for the U.S. presidential election. Given that the election will determine the path of fiscal policy moving forward, and by extension monetary policy, uncertainty related to the outcome is likely to remain a weight on financial markets through to November 5th.

Elevated interest rates continued to dampen housing market activity in September, as existing home sales fell to their lowest level since 2010! Demand is also likely being restrained in part by consumer expectations for lower interest rates moving forward, with Federal Reserve Chair Powell indicating that rates would likely be trending lower through the coming year during his press conference last month. Existing home sales are likely to remain subdued in the near-term as mortgage rates moved back above 6½% in October. Nevertheless, the housing market is expected to thaw over the coming year as the Federal Reserve continues to reduce borrowing costs.

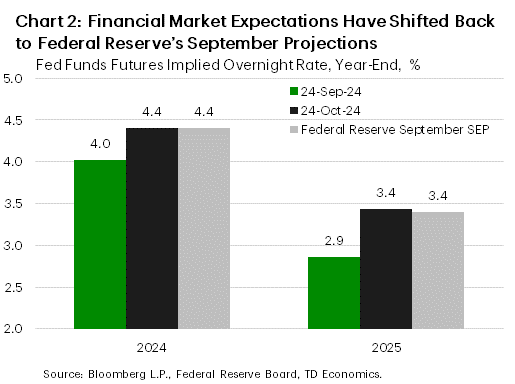

The Federal Reserve will be entering its pre-interest rate decision blackout period this weekend, with no further updates expected until Chair Powell’s post-meeting press conference on November 7th. The Fed officials we heard from this week stated that the strength of incoming economic data would warrant caution in future policy decisions, but all speakers noted that the trajectory of interest rates would continue to be downward. Market pricing has pulled back their expectations for rate cuts, but they are now realigned with the Federal Reserve’s median projection from the September Summary of Economic Projections (Chart 2).

The Federal Reserve will be entering its pre-interest rate decision blackout period this weekend, with no further updates expected until Chair Powell’s post-meeting press conference on November 7th. The Fed officials we heard from this week stated that the strength of incoming economic data would warrant caution in future policy decisions, but all speakers noted that the trajectory of interest rates would continue to be downward. Market pricing has pulled back their expectations for rate cuts, but they are now realigned with the Federal Reserve’s median projection from the September Summary of Economic Projections (Chart 2).

Next week sees a bumper crop of data releases that will be key inputs to the Federal Reserve’s next interest rate decision. The advance estimate for real GDP growth in the third quarter is expected to show the economy continuing to grow at a strong pace of 3.0%. While employment growth remained solid in the third quarter, October’s employment report due out next Friday is expected to show a deceleration in job gains (125k vs. 254k in September). The Federal Reserve will also be monitoring the release of their preferred inflation metric next week, core PCE, which is expected to show a modest decline to 2.6% in September.

Assuming there are no surprises in the incoming data, the Federal Reserve is expected to continue to cut rates at a pace of 25 basis points per meeting through the end of the year. Chair Powell’s remarks on November 7th will be monitored closely for guidance, although they may be competing with the results of the 2024 election for the attention of financial markets. Suffice it to say, markets will not be left wanting for important developments in the coming weeks.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of October 18th, 2024

Financial News Highlights

- The retail sales report once again reinforced the message that the U.S. consumer continues to brush off headwinds in financial news.

- Personal income growth, some remaining pandemic savings, and a healthy labor market should help to support trend-like growth in personal consumption expenditures into early 2025.

- A still healthy labor market, and a commitment to data dependency means a measured and deliberate approach to interest rate reductions.

Slow and Steady

U.S. Treasury yields were on the rise again this week (Chart 1) as a brighter picture of the consumer pared back rate cut bets in financial news. The September retail sales report once again reinforced the message that the consumer continues to plow ahead, brushing off headwinds from higher rates and two years’ worth of rapid cost-of-living increases. Policymakers and markets continue to assess that interest rates need to fall further, but the timing and level of where they ultimately land remains hotly debated.

U.S. Treasury yields were on the rise again this week (Chart 1) as a brighter picture of the consumer pared back rate cut bets in financial news. The September retail sales report once again reinforced the message that the consumer continues to plow ahead, brushing off headwinds from higher rates and two years’ worth of rapid cost-of-living increases. Policymakers and markets continue to assess that interest rates need to fall further, but the timing and level of where they ultimately land remains hotly debated.

Data are streaming in and showing consumers, the backbone of the U.S. economy, are willing and able to spend on goods and services at a healthy pace. Retail sales figures for September rose 0.4% month-on-month, beating out economists’ expectations. Moreover, the “control group” of less volatile expenditure categories surged 0.7% for the month as spending on clothing, personal care and miscellaneous goods surged. With stronger than expected economic news, bond yields surged, rising 6 basis points (bps) through Thursday’s close.

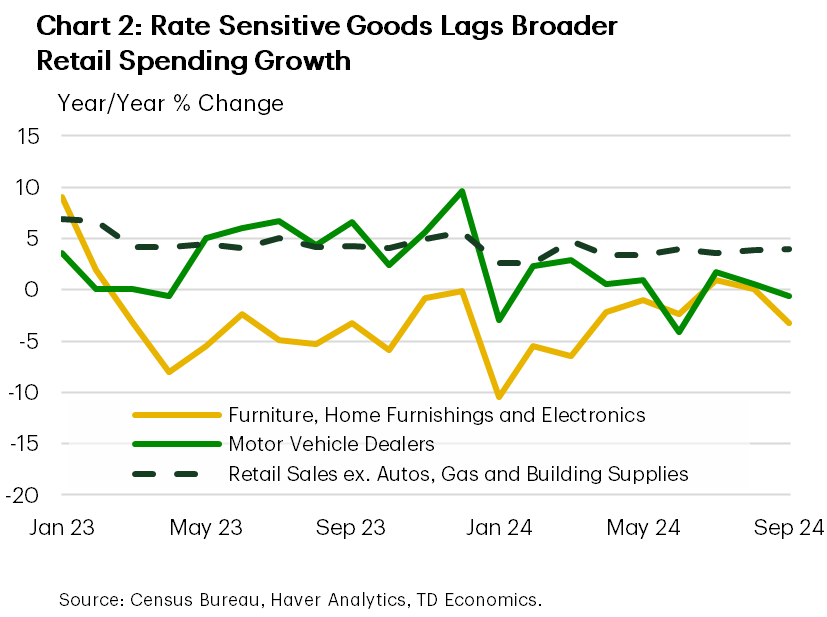

The print suggests plenty of momentum in consumption expenditures into the third quarter, providing a fillip to GDP growth. However, strong doesn’t mean that monetary policy isn’t exerting pressure on households. Sales of motor vehicle dealers were down marginally, as were expenditures on furniture and electronics stores (Chart 2). These categories of goods are more interest rate sensitive, leaving them most susceptible to the still elevated interest rate environment.

However, as we noted this week, the recent upward revision to personal income means households are still holding excess savings that can be deployed. While the funds are mostly concentrated among higher income households that are less likely to spend, their availability means that demand for durable goods could rise as interest rates slowly fall. This sentiment was echoed by Fed Governor Waller this week, when he noted that his “business contacts believe that there is considerable pent-up demand for durable goods, home improvements and other big-ticket items”.

However, as we noted this week, the recent upward revision to personal income means households are still holding excess savings that can be deployed. While the funds are mostly concentrated among higher income households that are less likely to spend, their availability means that demand for durable goods could rise as interest rates slowly fall. This sentiment was echoed by Fed Governor Waller this week, when he noted that his “business contacts believe that there is considerable pent-up demand for durable goods, home improvements and other big-ticket items”.

While the labor market is gradually rebalancing, personal income growth is still robust and some remaining pandemic savings should help to support trend-like growth in personal consumption expenditures into early 2025. Carefully balancing strong growth and a healthy labor market against the risks of a flare-up in inflation will likely leave the Fed adopting a relatively cautious and data dependent approach to interest rates – caution Governor Waller reiterated stating, “monetary policy should proceed with more caution on the pace of rate cuts than was needed at the September meeting.”

Policy remains highly restrictive, and more easing is on the way. A still healthy labor market, and a commitment to data dependency means a measured and deliberate approach to policy. This leaves us thinking the Fed will deliver two more quarter point cuts through 2024.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of October 11th, 2024

Financial News Highlights

- Progress on the inflation front appears to have stalled at the end of the third quarter in financial news, as core CPI inflation ticked up, albeit modestly, by 0.1 percentage point to 3.3% year-on-year in September.

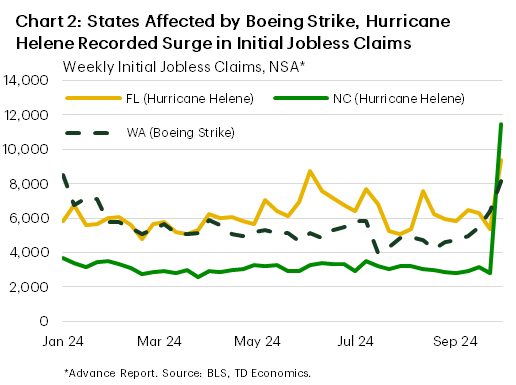

- Initial jobless claims surged higher by last week, as states affected by Hurricane Helene (FL, NC) and the ongoing Boeing strike (WA) recorded outsized increases to their unadjusted initial jobless claims.

- Between stronger job growth, and slower progress on inflation, we expect the Fed to cut rates more gradually, with two quarter-point cuts in November and December.

Rates to Fall, But Not So Fast

The second week of October continued to reflect the theme that began at last week’s close in financial news. A stronger-than-expected payrolls report last Friday drove home the point that the U.S. labor market is holding up better than previously thought, while this week’s CPI report showed progress on the inflation front stalling. All of this suggests that the Fed is likely to slow the pace of rate cuts next month. Bond yields continued the climb higher this week, with the 10-Year yield up another 10 basis points, closing out the week at 4.1%. Equity markets managed to eke out a decent gain, with the S&P 500 up roughly 1% from last week’s close, as of the time of writing.

The second week of October continued to reflect the theme that began at last week’s close in financial news. A stronger-than-expected payrolls report last Friday drove home the point that the U.S. labor market is holding up better than previously thought, while this week’s CPI report showed progress on the inflation front stalling. All of this suggests that the Fed is likely to slow the pace of rate cuts next month. Bond yields continued the climb higher this week, with the 10-Year yield up another 10 basis points, closing out the week at 4.1%. Equity markets managed to eke out a decent gain, with the S&P 500 up roughly 1% from last week’s close, as of the time of writing.

Total inflation as measured by CPI cooled in September, easing from 2.5% year-on-year (y/y) to 2.4%, largely due to falling energy prices. However, the good news ended there. Core CPI inflation rose a tenth of a percentage point, more than the consensus forecast, which pushed the twelve-month change higher to 3.3% y/y (Chart 1). Price growth in the important ‘shelter’ category eased, though we saw broader price pressures heat up across most other service categories, while core goods prices added to overall inflationary pressure – a first in seven months.

With progress on the inflation front stalling and the labor market holding up well, futures markets are now pricing just an 80% probability that the Fed will cut by 25-basis points next month. Minutes from the last FOMC meeting show that the Fed’s strong start to the easing cycle in September was thought of as a “recalibration” to help bring restrictive monetary policy into “better alignment” with recent indicators of inflation and the labor market, and that this should not be interpreted as the new pace of policy easing over the coming months. We anticipate the Fed will deliver two additional 25 basis point cuts by the end of this year.

However, it’s important to note that the Fed will remain heavily data dependent in setting monetary policy. This will become increasingly difficult over the coming months, with large distortions likely to be seen in October/November data because of Hurricane’s Helene and Milton and the ongoing Boeing strike. Besides the tragic loss of life, the recent hurricanes have left behind a path of destruction in the Southeast, which will exude some near-term weakness.

However, it’s important to note that the Fed will remain heavily data dependent in setting monetary policy. This will become increasingly difficult over the coming months, with large distortions likely to be seen in October/November data because of Hurricane’s Helene and Milton and the ongoing Boeing strike. Besides the tragic loss of life, the recent hurricanes have left behind a path of destruction in the Southeast, which will exude some near-term weakness.

The impacts of Boeing and Helene appear to already be featuring in employment data, with a sharp jump in initial jobless claims (up 33,000 to a seasonally adjusted 258,000 last week) tied in part to these events. Large increases in initial jobless claims were recorded in affected states such as Florida and North Carolina (Helene) and Washington (Boeing) (see Chart 2). We anticipate the Fed will look past the transient nature of some of these impacts as it continues to ease monetary policy next month, but communication as related to the next cut will require considerable effort given the many factors at play.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of October 4th, 2024

Financial News Highlights

- The U.S. labor market perked up in September as job gains beat expectations, the unemployment rate ticked down and annual wage gains edged up in financial news.

- The economic outlook, however, has been buffeted by significant disruptions, namely Hurricane Helene and a port worker strike.

- The production side of the economy continues to travel two very different paths with manufacturing contracting, while services expand.

A Duo of Disruption Muddies the Economic Outlook

The labor market was the data highlight in a week rocked by a major strike and natural disaster in financial news. Ten-year bond yields were notably higher relative to yesterday’s close (0.11 basis points) and the S&P500 was also up about 0.4% as the strong jobs report tempered expectations about the Fed’s cutting cycle.

The labor market was the data highlight in a week rocked by a major strike and natural disaster in financial news. Ten-year bond yields were notably higher relative to yesterday’s close (0.11 basis points) and the S&P500 was also up about 0.4% as the strong jobs report tempered expectations about the Fed’s cutting cycle.

Today’s employment report revealed that while the labor market may be cooling, it is doing so at a moderate pace (see commentary). Payrolls gains handily surpassed expectations, the unemployment rate edged down slightly, and wage gains nudged higher (Chart 1). Overall, the report was better than many market participants had expected and complements the previously released JOLTS data for August. The JOLTS report showed that while firms have slowed the pace of hiring there still continues to be steady demand for workers, as the number of job openings rose slightly. After the superheated labor market witnessed earlier in the post-pandemic period, followed by a steady cooling, the current leveling off in demand and supply is in line with a labor market that is coming into better balance.

On the production side, the ISM Manufacturing Index was unchanged in September, remaining in contraction territory for the sixth consecutive month. On the services side, however, things were looking better, with the ISM Services Index rising notably in September. Overall, the services sector continues to hold its ground, offsetting much of the weakness evident in the country’s manufacturing sector (Chart 2).

Major disruptions are threatening the health of the economy, however. Hurricane Helene, devastated parts of the southeastern United States with strong winds and heavy rains leaving widespread destruction. The destruction will depress near-term economic activity and is likely to negatively impact employment surveys. As rebuilding ensues, however, and normal economic activity resumes, a rebound is expected. The timeline on this, however, is uncertain.

In addition, a major dockworker strike at U.S. East and Gulf coast ports added to economic uncertainty. The strike was suspended late Thursday after the dockworkers’ union and the group representing ocean carriers reached an agreement to extend the currently expired contract, until January 15th. This allows dockworkers to resume work while negotiations over wages and port automation, which had been at an “impasse” for months, would now continue. While the worst effects of the strike have been avoided for now, the cloud of uncertainty continues to loom. If the two sides are not able to reach an agreement prior to the end of the extension, then things could be right back to where they were and the longer a strike persists, the greater the economic fallout (see commentary).

The job market showing signs of only gradual cooling, lends support to Powell’s view expressed earlier in the week that officials didn’t see a reason to lower rates as aggressively as they did at their most recent meeting. Barring the uncertainty of recent events, the labor market remains key in the Fed’s assessment of the most appropriate policy action.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 27th, 2024

Financial News Highlights

- The Federal Reserve’s preferred inflation metric, the core PCE index, continued to cool in August with the 3- and 6-month annualized trends converging closer to the Fed’s 2% target in financial news.

- Federal Reserve officials who spoke this week noted that the slowing labor market was a key consideration in their monetary policy decision last week and that further rate cuts were expected moving forward.

- Congress managed to pass a continuing resolution this week to fund the federal government through December 20th, removing the risk of a government shutdown until after the upcoming election.

Government Shutdown Averted as Price Pressures Continue to Ease

The first week of fall was largely consumed by lingering consternation regarding the Federal Reserve’s latest monetary policy decision. Federal Reserve officials who spoke this week provided further clarity on the central bank’s rationale to go big with the first rate cut in over four years, as the latest reading on inflation showed price pressures continued to cool in August. Financial markets were little changed on the week, with Treasury yields rising a few basis-points and the S&P 500 up 1.0% as of the time of writing.

The first week of fall was largely consumed by lingering consternation regarding the Federal Reserve’s latest monetary policy decision. Federal Reserve officials who spoke this week provided further clarity on the central bank’s rationale to go big with the first rate cut in over four years, as the latest reading on inflation showed price pressures continued to cool in August. Financial markets were little changed on the week, with Treasury yields rising a few basis-points and the S&P 500 up 1.0% as of the time of writing.

Friday’s personal income & spending data release for August showed that the health of the American consumer remained favorable on aggregate through the end of the summer. Real personal consumption expenditures rose 0.1% relative to July, with goods spending roughly flat while service expenditures expanded. Consumers continued to receive support from healthy real disposable personal income gains (+3.1% year-on-year in August), although this growth has continued to moderate. This has led to some slowing in consumer spending, which has helped to push the three- and six-month annualized percentage change in core PCE inflation closer to the Fed’s 2% target after the flare-up earlier in the year (Chart 1).

With inflation pressures continuing to cool, the Federal Reserve’s downward policy path trajectory appears to continue to be supported by the incoming data. Federal Reserve officials who spoke this week broadly echoed the statements of Chair Powell last week, noting that the balance of risks has shifted towards the labor market and that ensuring a soft landing would merit looser financial conditions moving forward. Although the majority of officials who spoke this week were focused on downside risks to the economy, Governor Bowman, the lone dissenting vote from last week’s decision, noted that inflation risks remained elevated and that this would necessitate caution moving forward. Market pricing is roughly 50/50 between a quarter- and a half-point cut at the next meeting in November as of the time of writing.

Markets will likely be equally focused on fiscal policy risks moving forward with the U.S. election now less than six weeks away. Thankfully, Congress managed to avoid the risk of a government shutdown this week by passing a continuing resolution through to December 20th. However, with federal government funding and the debt limit suspension both now expiring at the end of the year, fiscal risks are likely to remain top-of-mind in the final two months of the year.

Markets will likely be equally focused on fiscal policy risks moving forward with the U.S. election now less than six weeks away. Thankfully, Congress managed to avoid the risk of a government shutdown this week by passing a continuing resolution through to December 20th. However, with federal government funding and the debt limit suspension both now expiring at the end of the year, fiscal risks are likely to remain top-of-mind in the final two months of the year.

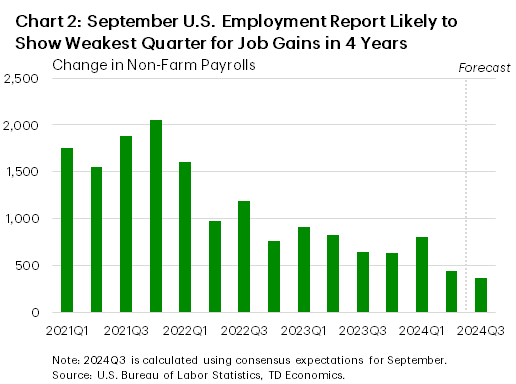

Looking ahead to next week, the biggest item on the docket will be the September employment report released on Friday, with consensus expectations for a gain of 130k jobs. This will likely cap-off the weakest quarter for job gains since the onset of the pandemic (Chart 2). Markets will also be watching Chair Powell’s speech at the National Association for Business Economics Annual Meeting on Monday, in addition to the Vice-Presidential debate in New York City on Tuesday.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 20th, 2024

Financial News Highlights

- The Federal Reserve started its easing cycle with a bang, reducing the policy rate by 50 basis points (bps) in financial news, bringing the target range to 4.75%-5.0%.

- Futures markets are pricing an additional 75 bps of cuts by year-end, slightly more than the updated median FOMC forecast, which shows another 50 bps of cuts.

- Economic data out this week including retail sales, housing starts, and industrial production all came in stronger than expected. Our Q3 GDP tracking sits a 2.1%.

FOMC Starts Easing Cycle With a Bang

There was no doubt heading into this week that the Federal Reserve would be cutting its policy rate on Wednesday. What remained in question, was the size of the cut. Right up until the announcement, market pricing remained relatively split on whether the FOMC would cut by 25 or 50 basis points (bps). Ultimately, policymakers opted for the bigger cut and signaled more easing to come. The more dovish tilt pushed U.S. equity markets higher, with the S&P 500 up just over 1% for the week at the time of writing.

There was no doubt heading into this week that the Federal Reserve would be cutting its policy rate on Wednesday. What remained in question, was the size of the cut. Right up until the announcement, market pricing remained relatively split on whether the FOMC would cut by 25 or 50 basis points (bps). Ultimately, policymakers opted for the bigger cut and signaled more easing to come. The more dovish tilt pushed U.S. equity markets higher, with the S&P 500 up just over 1% for the week at the time of writing.

Accompanying the policy statement, the FOMC also released revised economic forecasts, known as the Summary of Economic Projections (SEP) in financial news. The SEP is an aggregation of each Committee members’ individual forecasts but are not “official” Fed projections. Overall, the median forecast showed that the growth outlook remained little changed relative to the June forecast, with GDP still expected to expand by 2.0% per-year between 2024 and 2027. However, the unemployment rate was revised higher for both 2024 and 2025, and core PCE inflation was marked down in both years.

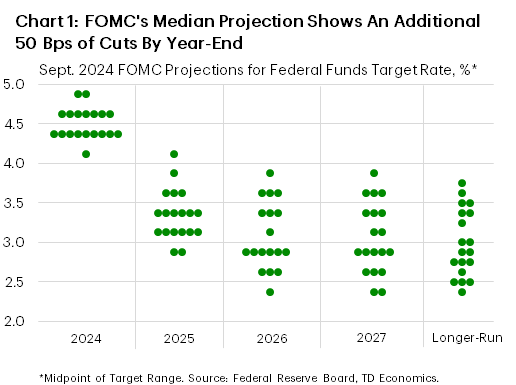

Consistent with the FOMC’s expectations for a slightly softer labor market, and cooler inflation, there were notable downward revisions to the median interest rate outlook (i.e., the “dot plot”) for 2024 through 2026. The revised forecast now shows a total of 100 bps of easing by the end of this year (previously 25 bps) with another 100 bps of cuts projected for 2025, corresponding to a target range of 3.25%-3.5% (Chart 1). This is 75 bps lower than the June SEP.

In the press conference, Chair Powell characterized the larger cut as a “strong start”, but also reiterated that future reductions in the policy rate were by no means on a preset course. Moreover, the Chair pushed back on the notion that this week’s outsized move was driven by a fear that the FOMC had fallen behind the curve. However, he did state that had the FOMC known back at the July 30-31 meeting that the labor market would have cooled as much as it did in the months that followed that rate decision, they probably would have started the easing cycle sooner.

In the press conference, Chair Powell characterized the larger cut as a “strong start”, but also reiterated that future reductions in the policy rate were by no means on a preset course. Moreover, the Chair pushed back on the notion that this week’s outsized move was driven by a fear that the FOMC had fallen behind the curve. However, he did state that had the FOMC known back at the July 30-31 meeting that the labor market would have cooled as much as it did in the months that followed that rate decision, they probably would have started the easing cycle sooner.

As noted in our recent Quarterly Forecast, we feel that odds favor another 50-bps cut in November. If policymakers are truly concerned that today’s policy stance is too restrictive, it’s more likely that they will want to act quickly to alleviate the pressure, before slowing the pace in December.

This is not a guarantee. The Fed remains data dependent, and nearly all economic data out this week including retail sales, industrial production, housing starts, and initial jobless claims came in better than expected, and remain consistent with an economy that’s still expanding in the 2-2.5% range. Next week’s personal income and spending data will provide more insight on August spending trends and is also likely to show a bit more progress on easing inflationary pressures (Chart 2). But it’s the September and October employment reports that could ultimately be the deciding factor of whether the Fed cuts by 25 or 50 bps in November.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 13th, 2024

Financial News Highlights

- Markets have been weighing the prospect that the Federal Reserve will opt for a 0.5 percentage point cut in the federal funds rate next week in financial news.

- Core consumer price index inflation surprised to the upside, lifted by a strong print from owners’ equivalent rent.

- The breadth of inflation continues to gradually narrow, but a still resilient economy supports the case for a standard 0.25 point cut at next week’s Fed meeting.

Here Comes the Cut

After Vice President Harris and former President Trump took their turn in the spotlight on Tuesday night, focus turned back to inflation and where the Federal Reserve is likely to take interest rates from here. Markets were weighing the possibility that the deteriorating economic backdrop was opening the door to a 50 basis-point cut in the Fed Funds rate next week. Alas, inflation didn’t seem to want to cooperate, as Consumer Price Index (CPI) inflation clocked in at 2.5%, as expected, with the core measure surprising to the upside amid an upturn in shelter prices. Current market pricing puts the odds of a 50 basis-point cut at basically a coin toss, but we think the state of the economy and the details of the report argue for a smaller 25 basis-point move next week.

After Vice President Harris and former President Trump took their turn in the spotlight on Tuesday night, focus turned back to inflation and where the Federal Reserve is likely to take interest rates from here. Markets were weighing the possibility that the deteriorating economic backdrop was opening the door to a 50 basis-point cut in the Fed Funds rate next week. Alas, inflation didn’t seem to want to cooperate, as Consumer Price Index (CPI) inflation clocked in at 2.5%, as expected, with the core measure surprising to the upside amid an upturn in shelter prices. Current market pricing puts the odds of a 50 basis-point cut at basically a coin toss, but we think the state of the economy and the details of the report argue for a smaller 25 basis-point move next week.

First, and foremost, this week’s report is a minor setback and not a return to the widespread inflation we saw in 2022. Most of the gain was powered by a strong showing in shelter costs, specifically owners’ equivalent rent (Chart 1). Growth here ticked up for the month, but this has been a steady contributor to inflation this cycle. While the rate could moderate slightly heading into the fall, it was the strongest print in seven months in financial news. Now, importantly, the Fed’s preferred measure looks at core personal consumption expenditure (PCE) inflation, where shelter prices carry a smaller weight. So, this upturn will have a comparably smaller impact on the Fed’s preferred inflation measure.

As for the two other major inflationary culprits, airfares and vehicle insurance, there is reason to expect moderation. New and used vehicle prices have cooled substantially, and after rising car valuations drove insurance rates higher, this impulse should continue to fade. On airfares, last month broke a string of negative prints for the category – an element of giveback that could easily fade.

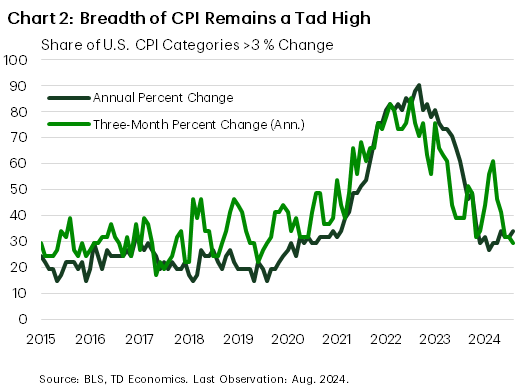

All of which is to say, consumer price inflation is gradually becoming confined to fewer categories (Chart 2). Taking a lens to the three-month percent change of the CPI categories, the share of categories with prices still rising above a three percent (annualized) rate has been below the pre-pandemic average for the past three months. After the uptick in inflation last spring, the return to a downward trajectory is welcome. This trend will need to continue for few more months still before the year-on-year prints start to show the same normalization, but things are pointing in the right direction.

All of which is to say, consumer price inflation is gradually becoming confined to fewer categories (Chart 2). Taking a lens to the three-month percent change of the CPI categories, the share of categories with prices still rising above a three percent (annualized) rate has been below the pre-pandemic average for the past three months. After the uptick in inflation last spring, the return to a downward trajectory is welcome. This trend will need to continue for few more months still before the year-on-year prints start to show the same normalization, but things are pointing in the right direction.

The data suggest that the Fed’s policy rate does not need to be as restrictive as it is, but while former NY Fed President Dudley this week suggested there was “a strong case” for a 50 basis- point cut, we think this is a tad premature. Between this week’s CPI report showing unexpected strength in core consumer prices, the upside surprise in the producer price index, and a labor market that continues to steadily add jobs, there is enough strength to suggest aggressively easing monetary policy is not yet warranted. Our view remains that a 25 basis-point cut next week is the most likely outcome, with two more cuts coming by year-end.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of September 6th, 2024

Financial News Highlights

- The U.S. added fewer jobs than expected in August, even as wage growth accelerated, and the unemployment rate edged down in financial news. Additionally, JOLTS data pointed to lower job openings, suggesting that the U.S. labor market continued to cool.

- Fed Governor Williams stated that the time had come for less restrictive monetary policy but remained mum on the possible size of any cut. Governor Waller, however, suggested he favored starting carefully.

- Manufacturing activity continued to contract in August, with demand easing. However, the services sector, continued to chug along as it has for much of this year.

With Employment Slowing, The Time to Cut is Here

In a holiday shortened week, the labor market took center stage. Both the Job Opening and Labor Turnover Survey (JOLTS) and employment report were on the calendar. Given the Fed’s recent heighten focus on the second leg of its dual mandate – to promote maximum employment – the reports carried larger than usual significance. Notably, they provided a last look at top-tier labor market data before the Fed’s meeting on September 18th. Markets were generally down throughout the week. This morning’s employment report extended that trend as 10-year bond yields edged lower relative to last week’s close (-0.22 percentage points) and the S&P500 also dipped lower (-3.4%), as of the time of writing.

In a holiday shortened week, the labor market took center stage. Both the Job Opening and Labor Turnover Survey (JOLTS) and employment report were on the calendar. Given the Fed’s recent heighten focus on the second leg of its dual mandate – to promote maximum employment – the reports carried larger than usual significance. Notably, they provided a last look at top-tier labor market data before the Fed’s meeting on September 18th. Markets were generally down throughout the week. This morning’s employment report extended that trend as 10-year bond yields edged lower relative to last week’s close (-0.22 percentage points) and the S&P500 also dipped lower (-3.4%), as of the time of writing.

The increase in August’s payroll growth came in lower than anticipated and on a three-month basis, continued to head lower (Chart 1). Additionally, the figures for the prior two months were revised down. Despite this, there was some good news – the unemployment rate ticked down and annual growth in average hourly earnings edged up. Today’s payrolls report was a mixed bag, but overall, adds to the thesis that the labour market has eased off the gas in financial news. In a statement by Fed Governor Williams, following release of the report, he was clear in his believe that it was now appropriate to dial back policy restrictiveness. Further, speaking after the jobs data, Governor Waller pointed to starting rate cuts “carefully”, but was open to moving faster if the data warrant it.

In another sign of a cooling labor market, the more backward-looking JOLTS report revealed that job openings fell more than anticipated in July to 7.7 million. This marked the lowest level in more than three years. Additionally, the job openings to unemployed workers ratio declined to 1.1 from a high of 2 in early-2022. The job separation rate also ticked up in July after a dip in June, though it still remains relatively low. Overall, the JOLTS data suggests that the pandemic era of tightness in the labor market has receded and adds to the mounting evidence of cooling labor demand and a slowing economy.

In another sign of a cooling labor market, the more backward-looking JOLTS report revealed that job openings fell more than anticipated in July to 7.7 million. This marked the lowest level in more than three years. Additionally, the job openings to unemployed workers ratio declined to 1.1 from a high of 2 in early-2022. The job separation rate also ticked up in July after a dip in June, though it still remains relatively low. Overall, the JOLTS data suggests that the pandemic era of tightness in the labor market has receded and adds to the mounting evidence of cooling labor demand and a slowing economy.

On the production side, while the ISM Manufacturing Index managed to edge up in August, it remained in contraction territory for the fifth consecutive month and came in lower than analysts’ expectations. The sector continued to experience weakness in demand as both the new orders and new export orders indexes slid deeper into contraction. The ongoing weakness in the sector rekindled some concerns over the health of the economy. On the services side, however, things were a bit better, with the ISM Services Index coming in at 51.5 in August, up just slightly from 51.4 in July. Overall, the services sector continues to hold its ground, offsetting much of the weakness evident in the manufacturing sector (Chart 2).

With the employment numbers now a known variable, the Fed’s attention will be focused on the inflation data on tap for release next week. Barring any unforeseen flare-ups, all roads seem to lead to a quarter-point rate cut at the September meeting.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.