Financial News for the Week of August 30th, 2024

Financial News Highlights

- The second estimate of Q2 GDP revealed that the U.S. economy grew at 3.0% annualized, a bit stronger than previously reported, thanks to an upward revision in consumer spending in financial news.

- Spending momentum continued into July, outstripping income growth for the sixth consecutive month and pushing the savings rate to a two-year low of 2.9%.

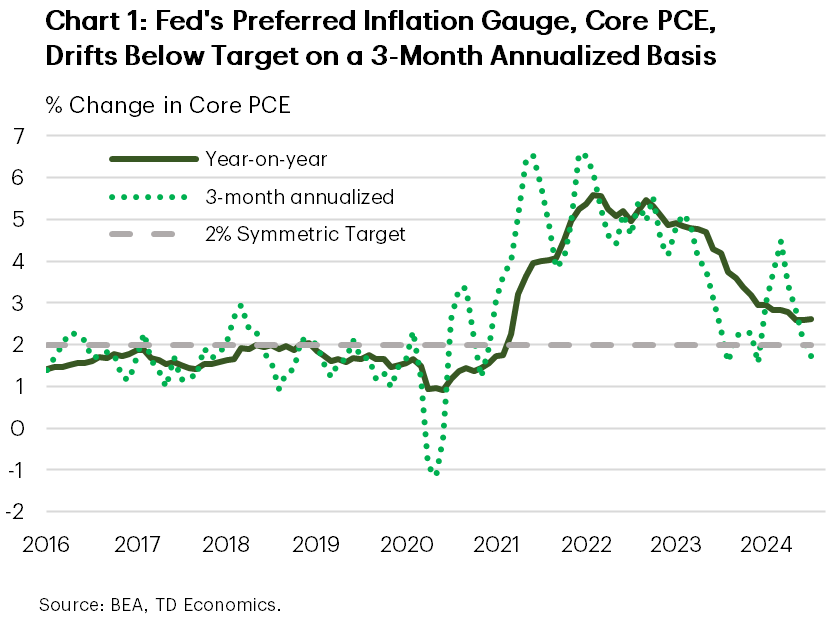

- Core PCE inflation held steady at 2.6% year-on-year in July, while the three-month annualized rate of change fell below the Fed’s 2% inflation target.

Fed to Tilt Focus to Labor Market as it Tees Up First Rate Cut

The Labor Day weekend is upon us, providing an opportunity to celebrate the achievements of the American worker. Keeping with the labor market theme, now that the Fed appears relatively confident that inflation will return to target, we believe it will put a little more emphasis the other side of its dual mandate – the goal of maximum employment – to determine the speed and size of policy easing. In that vein, next week’s payrolls report can’t come soon enough. This week’s data, meanwhile, did little to rock the boat, coming in broadly positive. Amidst this backdrop, long-term yields trended modestly higher, while the S&P 500 looks to end the week lower by 0.6% as of the time of writing.

The Labor Day weekend is upon us, providing an opportunity to celebrate the achievements of the American worker. Keeping with the labor market theme, now that the Fed appears relatively confident that inflation will return to target, we believe it will put a little more emphasis the other side of its dual mandate – the goal of maximum employment – to determine the speed and size of policy easing. In that vein, next week’s payrolls report can’t come soon enough. This week’s data, meanwhile, did little to rock the boat, coming in broadly positive. Amidst this backdrop, long-term yields trended modestly higher, while the S&P 500 looks to end the week lower by 0.6% as of the time of writing.

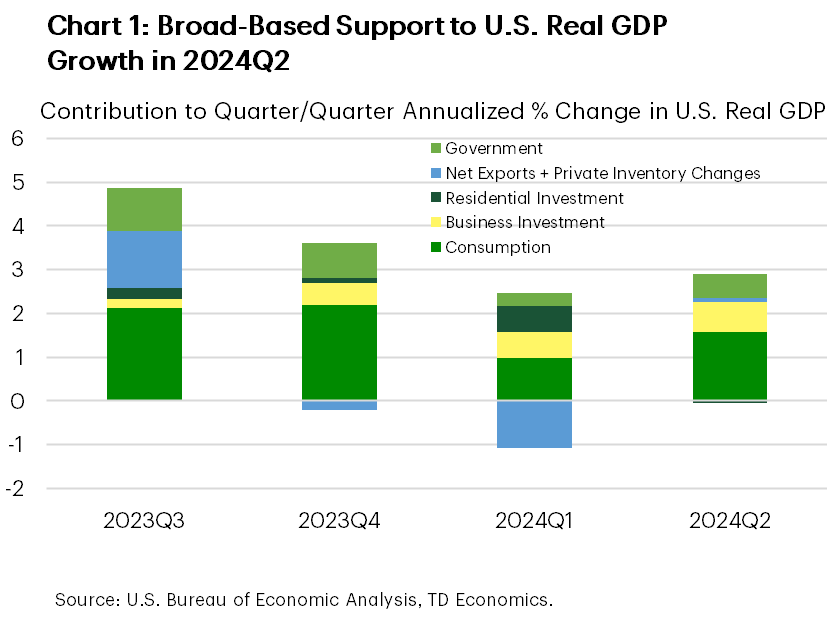

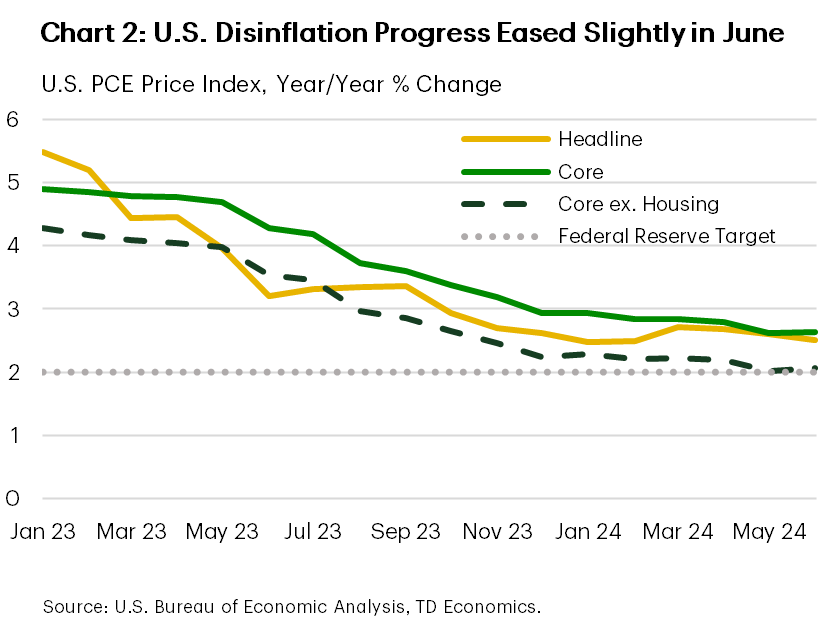

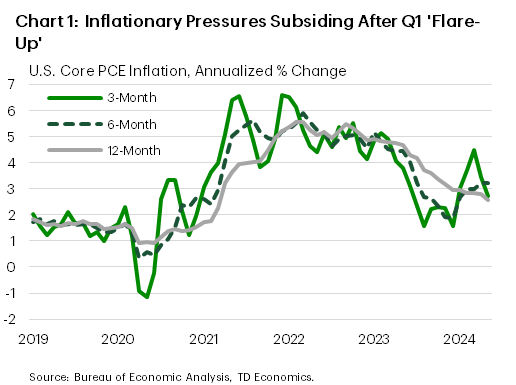

A second read on U.S. GDP revealed an even better growth profile of 3.0% annualized in the second quarter (vs. 2.8% previously), thanks in large part to an upward revision in consumer spending (2.9% vs. 2.3% previously). But this week’s highlight was the July personal income and spending (PCE) report. The latter showed that overall and core PCE inflation held steady on an annual basis, coming in at respectively 2.5% and 2.6% in July. Looking to more recent trends, on a 3-month annualized basis, core PCE eased to 1.7% in July from 2.1% in the month prior, suggesting we’re likely to see more cooling in inflationary pressures in the months ahead (Chart 1).

The PCE report also shed light on consumer spending, which had a relatively healthy start to the third quarter in financial news. Real spending rose by 0.4% month-over-month (m/m) in July – an acceleration from 0.3% in the month prior, with both goods and service spending chipping in with healthy gains. However, real disposable personal income continued to trail behind (+0.1%), which meant consumers had to dip into their savings to sustain the higher rate of spending. As a result, the personal savings rate fell to a two-year low of 2.9%.

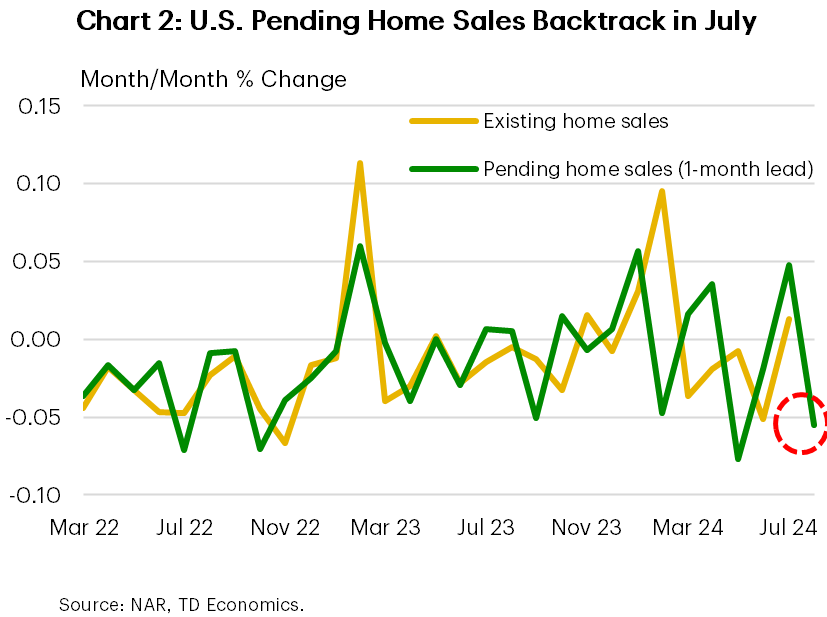

Other consumer-related indicators continued to paint a nuanced picture. Americans were a little more upbeat in August, with the Conference Board confidence measure rising to a six-month high, thanks in large part to an improvement in the “expectations” subcomponent. Still, plans to buy large ticket items, including cars, homes, and major appliances, all trended lower on the month. And it’s not just survey data showing a consumer’s reluctance to make big purchases. Pending home sales – a leading indicator for existing home sales – fell sharply in July (-5.5%), driving home the point that the recent pullback in interest rates has so far failed to spark a sustained improvement in sales (Chart 2).

Other consumer-related indicators continued to paint a nuanced picture. Americans were a little more upbeat in August, with the Conference Board confidence measure rising to a six-month high, thanks in large part to an improvement in the “expectations” subcomponent. Still, plans to buy large ticket items, including cars, homes, and major appliances, all trended lower on the month. And it’s not just survey data showing a consumer’s reluctance to make big purchases. Pending home sales – a leading indicator for existing home sales – fell sharply in July (-5.5%), driving home the point that the recent pullback in interest rates has so far failed to spark a sustained improvement in sales (Chart 2).

Next week, attention will turn towards the August payrolls report, which will help shape whether the Fed cuts by 25 or 50 basis points at its next rate decision in September. Market expectations call for some rebound in job gains relative to July’s gain of 114,000. The recent steadying of both jobless claims and job postings suggests that the chances of another downside miss is less likely, which favors a 25 basis point cut in September.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of August 23rd, 2024

Financial News Highlights

- Minutes from the July 30-31 FOMC meeting as well as Chair Powell’s speech at Jackson Hole showed a clear commitment that the FOMC will start cutting rates in September in financial news.

- The Fed is likely to start slow, cutting by 25 basis points next month. But any signs of a more abrupt cooling in the labor market will result in a more aggressive pace of rate cuts.

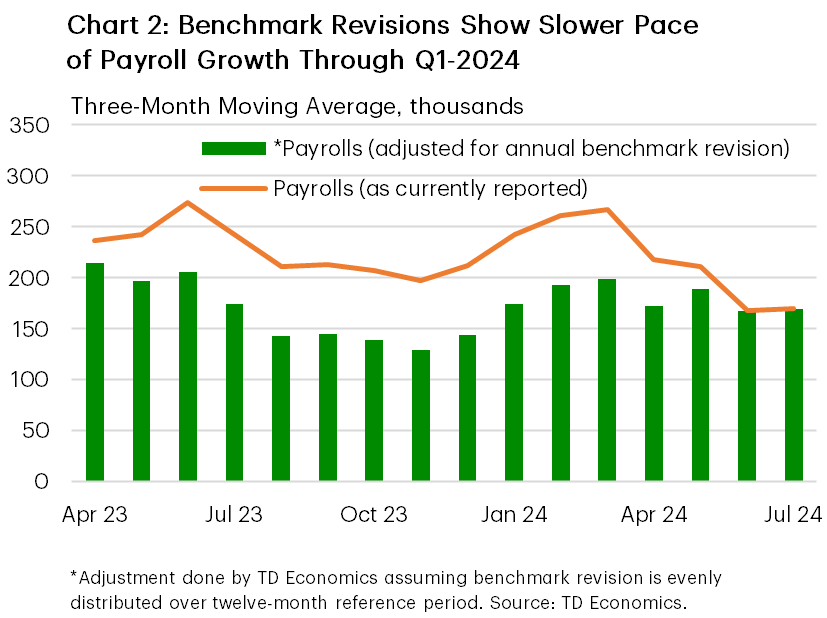

- Adding to evidence of a cooler labor market, annual benchmark revisions showed non-farm employment ended Q1 with less momentum than previously thought.

Fed Chair Powell Endorses September Rate Cut

It was a quiet week on the economic data calendar, but there was plenty of Fed communication for market participants to digest. The headliner was Fed Chair Powell’s speech at the annual Jackson Hole Symposium, where the Chairman signaled a clear desire for the FOMC to begin reducing its policy rate at its next meeting in September. The news hardly came as a surprise, particularly coming after the release of the July 30-31 FOMC minutes, which indicated that the “vast majority of participants” supported cutting rates at the next meeting. Though equity markets see-sawed through most of the week, a clear commitment from Powell that the Fed will soon start loosening its policy stance helped to fuel a late-week rally, with the S&P 500 looking to end the week up 1.3%. Bond yields across the curve were lower by 10-15 basis-points (bps) on the week, with the 10-year Treasury sitting at 3.8% at the time of writing.

It was a quiet week on the economic data calendar, but there was plenty of Fed communication for market participants to digest. The headliner was Fed Chair Powell’s speech at the annual Jackson Hole Symposium, where the Chairman signaled a clear desire for the FOMC to begin reducing its policy rate at its next meeting in September. The news hardly came as a surprise, particularly coming after the release of the July 30-31 FOMC minutes, which indicated that the “vast majority of participants” supported cutting rates at the next meeting. Though equity markets see-sawed through most of the week, a clear commitment from Powell that the Fed will soon start loosening its policy stance helped to fuel a late-week rally, with the S&P 500 looking to end the week up 1.3%. Bond yields across the curve were lower by 10-15 basis-points (bps) on the week, with the 10-year Treasury sitting at 3.8% at the time of writing.

Two years ago, Chair Powell delivered a very somber message during his speech at Jackson Hole, stating the Federal Reserve will do “whatever it takes to restore price stability” even if that meant “inflicting some economic pain” in financial news. At the time, inflation was sitting at a multi-decade high while the labor market had tightened to a degree not seen in recent history. It had become obvious that policymakers had fallen well behind the curve and were scrambling to play catch-up. While many feared that the FOMC’s swift actions of quickly raising the policy rate (Chart 1) risked overtightening and potentially tipping the economy into a recession, the downturn never materialized.

During his speech Friday morning, Chair Powell acknowledged the progress the Fed has made over the past two years, specifically noting that the upside risks to inflation have diminished while the downside risks to employment have increased. While Powell offered nothing in terms of the speed of adjustment, other policymakers speaking this week highlighted the importance of a “gradual” and “methodical” approach to loosening policy, which supports a 25 basis point cut in September. However, Powell also emphasized that the FOMC “does not seek or welcome any further cooling in the labor market”, which suggests the next several employment reports will be critical in determining the future path of the policy rate.

During his speech Friday morning, Chair Powell acknowledged the progress the Fed has made over the past two years, specifically noting that the upside risks to inflation have diminished while the downside risks to employment have increased. While Powell offered nothing in terms of the speed of adjustment, other policymakers speaking this week highlighted the importance of a “gradual” and “methodical” approach to loosening policy, which supports a 25 basis point cut in September. However, Powell also emphasized that the FOMC “does not seek or welcome any further cooling in the labor market”, which suggests the next several employment reports will be critical in determining the future path of the policy rate.

Fears of a further cooling in the labor market aren’t completely unfounded. Earlier this week, the BLS released its preliminary annual benchmark revisions for non-farm employment, which showed that payrolls were 818 thousand less over the twelve-month period ending in March 2024 - the largest downward adjustment since 2009. This implies that job gains likely averaged closer to 174 thousand per-month over the reference period, as opposed to the 242 thousand currently reported (Chart 2).

Even after incorporating the revisions, there’s nothing yet to suggest that the labor market has overcorrected. This is why we feel that the FOMC is likely to opt for a more gradual approach in the beginning. However, it is clear that policymakers have become hypervigilant of the labor market and any further signs of cooling is likely to bring a more aggressive path for rate cuts.

Thomas Feltmate Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of August 16th, 2024

Financial News Highlights

- The July report for the Consumer Price Index showed headline inflation fell below 3% for the first time since March 2021 in financial news.

- U.S. retail sales surpassed expectations in July, rising 1.0% month-on-month.

- Federal Reserve Chair Jerome Powell’s remarks during next week’s Jackson Hole Symposium will headline the week.

Inching Towards a Pivot

A relative state of calm presided over financial markets this week as incoming economic data continued to support the case for the first Federal Reserve rate cut in September in financial news. Inflation data for July showed that the annual change in prices fell below 3% for the first time since March 2021, while retail sales for the month came in above expectations. In response, equity markets rose on the week with the S&P 500 up 3.7% as of the time of writing, while U.S. Treasury yields steadied with the two-year yield roughly unchanged at 4.08%.

A relative state of calm presided over financial markets this week as incoming economic data continued to support the case for the first Federal Reserve rate cut in September in financial news. Inflation data for July showed that the annual change in prices fell below 3% for the first time since March 2021, while retail sales for the month came in above expectations. In response, equity markets rose on the week with the S&P 500 up 3.7% as of the time of writing, while U.S. Treasury yields steadied with the two-year yield roughly unchanged at 4.08%.

The Consumer Price Index (CPI) report for July showed that inflation picked up slightly relative to June in monthly terms, primarily driven by an uptick in shelter costs. However, the monthly increase in headline and core inflation was still below the level consistent with the Federal Reserve’s 2% target. As a result, the 3-month annualized percentage change in core CPI fell to its lowest level since early 2021 (Chart 1). While the Fed’s preferred inflation metric, core PCE, sat at 2.6% in June, momentum in CPI inflation continues to indicate that inflation pressures will likely ease further moving forward.

This was also evidenced by the Producer Price Index (PPI) report released this week, which showed that upstream production costs decelerated in July. Annual growth in producer prices had been rising through the first half of the year, which contributed to the slowing in the disinflation progress as these costs were likely passed on to consumers. Therefore, the reversal in this trend in July, especially if sustained, would likely provide further relief to consumer price growth moving forward. Taken together the trends in the July reports for PPI and CPI inflation support the case for the Federal Reserve to begin to gradually reduce interest rates at their next meeting in September.

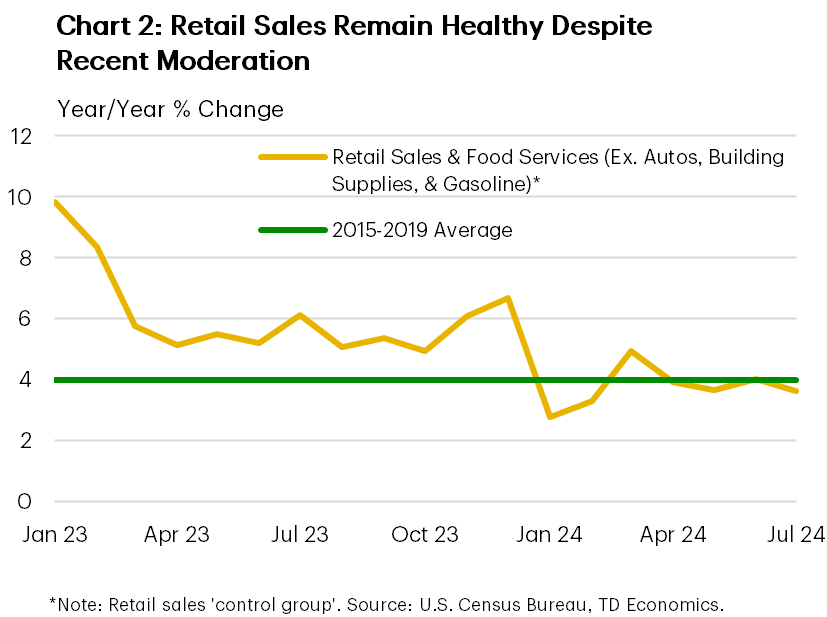

Fortunately, the moderation in price growth seen recently has not required a decline in consumer demand. As indicated by July retail sales, spending rose more than expected to start the second half of the year. This was in part driven by a rebound in auto sales after a cyber-attack against a dealership software firm depressed sales in June. Still, sales in the ‘control group’, which excludes the more volatile spending categories, remained healthy in July (Chart 2). The economy has exited a period of exceptionally strong demand and maintained stable momentum, but the Federal Reserve will be cognizant of the balance of risks moving forward.

Fortunately, the moderation in price growth seen recently has not required a decline in consumer demand. As indicated by July retail sales, spending rose more than expected to start the second half of the year. This was in part driven by a rebound in auto sales after a cyber-attack against a dealership software firm depressed sales in June. Still, sales in the ‘control group’, which excludes the more volatile spending categories, remained healthy in July (Chart 2). The economy has exited a period of exceptionally strong demand and maintained stable momentum, but the Federal Reserve will be cognizant of the balance of risks moving forward.

In the leadup to the Federal Reserve’s annual Jackson Hole Symposium next week, the slate of Fed speakers was relatively light this week. Governor Bowman, who is the only voting member of the FOMC who spoke this week, noted that upside risks to inflation remain and that caution would be warranted in considering future policy adjustments. Fed Presidents Bostic (Atlanta) and Musalem (St. Louis) broadly echoed these concerns, although both noted that interest rates would likely be lower in the second half of the year. Financial markets pared back their expectations for an outsized 50 basis-point (bps) cut in September this week, converging closer to our expectation for a 25bps cut, while they await further guidance from Chair Powell’s remarks scheduled for next Friday.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of August 2nd, 2024

Financial News Highlights

- Nonfarm payroll gains came in lower than expected in July, with the unemployment rate heading higher in financial news. The numbers add to other data suggesting that the U.S. labor market is losing steam.

- While the Federal Reserve held rates steady at their July meeting as widely expected, Chair Powell gave the strongest indication yet that a September rate cut is on the table.

- The manufacturing sector continued to struggle, as the ISM manufacturing index remained in contraction territory.

It’s A Different World

The main highlights of the week were developments in the labor market and a mid-week update from the Federal Reserve. Several reports showed that conditions in the labor market were cooling, while the Fed largely lived up to expectations by holding rates steady. Their signals about a possible cut at the September meeting were generally of more interest to markets. In response to the September signal, stock markets rallied, and bond yields pulled back. This morning’s jobs number was even more of a market mover, with 10-year yields down 13 basis points relative to yesterday’s close.

The main highlights of the week were developments in the labor market and a mid-week update from the Federal Reserve. Several reports showed that conditions in the labor market were cooling, while the Fed largely lived up to expectations by holding rates steady. Their signals about a possible cut at the September meeting were generally of more interest to markets. In response to the September signal, stock markets rallied, and bond yields pulled back. This morning’s jobs number was even more of a market mover, with 10-year yields down 13 basis points relative to yesterday’s close.

What a difference a year makes. The U.S. economy today, with annualized growth slowing from about 4% towards a more trend-like 2%, inflation down and unemployment ticking up, looks starkly unlike it did a year ago according to Fed Chair Powell. After issuing a statement keeping the policy rate unchanged, at his press conference, Powell noted that last year, it was a completely different economy with higher inflation and a robust job market in financial news. Now, he notes, on the employment front, indicators show the job market has gradually normalized from “overheated” conditions and the Fed is able to weigh prices and the labor market more equally as inflation has cooled.

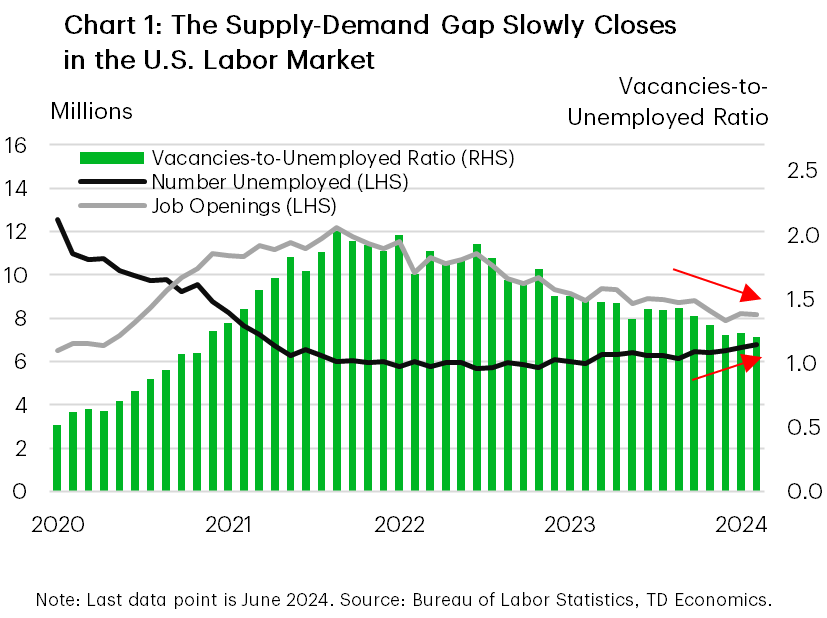

Reports out this week supported his statements on the job market. First up, the more backward-looking JOLTS data showed that the number of job openings in June inched down relative to May. While there are still plenty of jobs available relative to the more than 6.8 million unemployed job seekers in June — the gap has narrowed with the vacancies-to-unemployed ratio falling relative to its value in May (Chart 1). Other elements of the report also supported a softening labor market narrative – the hires rate ticked down and the quits rate was unchanged from May’s downwardly revised 2.1% (which is below where it was immediately prior to the pandemic). Additionally, the Employment Cost Index (ECI) report, which the Fed watches closely for wage trends, slowed at a faster-than-expected pace in Q2.

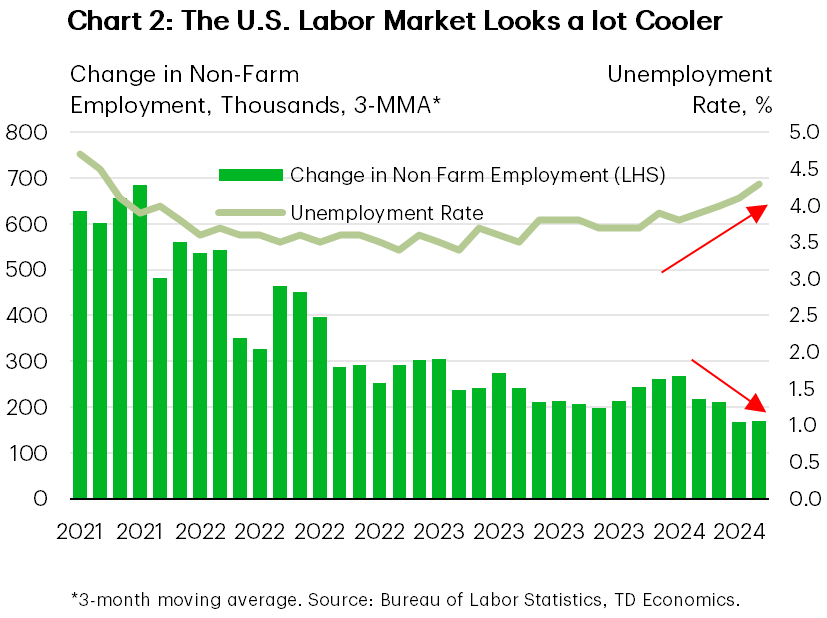

The signal from the more recent July payrolls report was generally in line with the JOLTS and ECI data. The economy added 114k jobs in July, missing expectations (Chart 2). The unemployment rate rose for the fourth consecutive month and annual wage growth decelerated to the slowest pace in over three years. Together, the three employment reports suggest that demand for workers continued to slow and add further evidence that the labor market is cooling.

The signal from the more recent July payrolls report was generally in line with the JOLTS and ECI data. The economy added 114k jobs in July, missing expectations (Chart 2). The unemployment rate rose for the fourth consecutive month and annual wage growth decelerated to the slowest pace in over three years. Together, the three employment reports suggest that demand for workers continued to slow and add further evidence that the labor market is cooling.

On the production side, the ISM Manufacturing Index declined again in June. The series fell 1.7 points to 46.8, marking its fourth consecutive month in contraction territory after a short-lived reprieve in March. Demand continued to slow and output conditions worsened. Persistent contraction in the manufacturing sector alongside slowing consumer demand, present downside risks to US growth, which has already come off the above trend pace of last year.

As Chair Powell hinted at, the U.S. economy is in a different world now. As both sides of the Fed’s dual mandate come into sharper focus, a September cut is almost a guarantee and the chance for three rate cuts this year has certainly risen.

Shernette McLeod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of July 26th, 2024

Financial News Highlights

- The U.S. economy accelerated in the second quarter, growing by 2.8% (annualized), up from 1.4% in the first quarter in financial news.

- At the same time, inflation cooled to 2.5% year-on-year (y/y) in June, as measured by the personal consumption expenditure deflator. However, the Fed’s preferred inflation metric, core PCE, was unchanged relative to May.

- High interest rates continued to burden the housing market in June, as existing home sales fell 5.4% month-on-month.

All Eyes on Next Week’s Fed Meeting

With the second half of the year now well under way, data this week showed a fairly Goldilocks outcome for the U.S. economy in financial news. Growth momentum coming out of the first half of the year was broadly favorable, while at the same time, inflationary pressures are cooling. In financial markets, company earnings reports out this week were mixed on aggregate, with weakness among the large tech firms dragging the S&P 500 down by 0.9% on the week as of the time of writing. U.S. Treasury yields also fell modestly on Friday’s PCE inflation report as markets wait to hear from the Federal Reserve next week.

Starting the week off on Tuesday, June housing data showed that existing home sales fell sharply to end the second quarter, fully retracing the uptick seen in the first quarter. However, this has not translated into material price adjustments, as the median home sales price in June was only a half-step off its all-time high seen in the month prior. With expectations growing for lower interest rates in the second half of the year, it’s possible that some buyers are biding their time.

The decline in the housing market shaved a marginal amount off real GDP growth in the second quarter, but solid growth in consumption, business investment, and government spending pushed the quarterly annualized growth rate to 2.8%, up from 1.4% in the first quarter (Chart 1). Growth in final sales to private domestic purchasers (excluding government spending and private inventory adjustments) was unchanged relative to the first quarter, as stronger consumption was offset by weakness in the housing market. Looking ahead, we expect that growth will moderate through the second half of the year but remain near the long-run average as the Federal Reserve begins to lower rates in the coming months.

To that end, inflation data released on Friday was slightly mixed on aggregate. Although headline PCE inflation declined modestly, core PCE inflation on a year-on-year basis was unchanged owing to a marginal acceleration in core PCE ex. housing, which offset a deceleration in housing inflation. Nevertheless, with housing inflation expected to continue to moderate moving forward and annual core PCE ex. housing inflation still in-line with the Fed’s 2% target (Chart 2), this report will not likely sway the Fed’s confidence about disinflation progress to a great degree.

Looking ahead, on the one-year anniversary of the last time the Fed hiked rates, Chair Powell is expected to begin opening the door to the possibility of a near-term pivot to rate cuts during his press conference next week. Financial markets have fully priced in the first cut occurring in just under two months at the September meeting, with an additional 2-3 cuts expected by year-end. However, overall guidance from the Fed next week is expected to emphasize caution and flexibility. Given the flare up in inflation in the first quarter, the Fed is going to want to be quite confident that inflation will continue to move in the right direction. On the other side of the Fed’s dual mandate, the second-last employment report before the September meeting, out next Friday, will also be monitored closely to determine whether the deceleration in job growth in the second quarter carried into the third.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of July 19th, 2024

Financial News Highlights

- After an eerily calm few months, a fresh dose of volatility descended across global financial markets this week in financial news.

- Top Fed officials speaking this week noted that they are getting ‘closer’ to cutting interest rates. Financial markets have fully priced the first cut to come in September.

- Retail sales and industrial production data for June came in better than expected, while homebuilding remains under pressure.

Nearing the Pivot Point

After an eerily calm few months, this week brought a fresh dose of volatility across global financial markets in financial news. The equity selloff was heavily concentrated across the tech sector, following some speculation that the Biden administration is considering implementing new rules to clamp down on companies exporting chipmaking equipment to China. While the selloff widened as the week progressed, small-cap stocks still managed to end the week 2% higher and are up 8% over the past nine trading days. The S&P 500 is down nearly 0.5% over that same period. The recent outperformance has largely been driven by market participants becoming increasingly confident that the Fed will begin easing its policy stance over the coming months. At the time of writing, market odds are fully priced for the first cut to come in September, with 63 bps of easing expected by year-end.

After an eerily calm few months, this week brought a fresh dose of volatility across global financial markets in financial news. The equity selloff was heavily concentrated across the tech sector, following some speculation that the Biden administration is considering implementing new rules to clamp down on companies exporting chipmaking equipment to China. While the selloff widened as the week progressed, small-cap stocks still managed to end the week 2% higher and are up 8% over the past nine trading days. The S&P 500 is down nearly 0.5% over that same period. The recent outperformance has largely been driven by market participants becoming increasingly confident that the Fed will begin easing its policy stance over the coming months. At the time of writing, market odds are fully priced for the first cut to come in September, with 63 bps of easing expected by year-end.

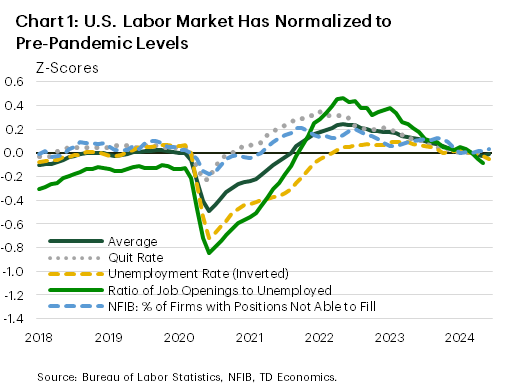

Based on how recent data has trended, investors have good reason to suspect that the Fed will likely begin dialing back its policy rate come September. Last week’s CPI report showed inflationary pressures cooling faster than expected, while recent readings of the labor market suggest that nearly all the pandemic imbalances have been restored (Chart 1). Speaking at an event at the Washington Economic Club this week, Powell reiterated the point on the labor market, citing “… essentially we’re back at equilibrium”. On inflation, Powell noted that recent readings have “added somewhat to confidence”. Other Fed officials including Williams and Waller echoed Powell’s sentiment this week, noting that the improved inflation trajectory has brought the Fed “closer” to cutting interest rates and that the current economic data are consistent with the Fed achieving a ‘soft landing’.

Indeed, economic data out this week support the notion that while the economy is slowing, it’s not falling off a cliff. Retail sales were flat in June, but that was largely related to a sharp pullback in auto sales due to a cyber-attack on a software firm that supports car dealers across the country. Meanwhile, the control retail group – used in the BEA’s calculation of PCE – rose by a healthy 0.9% m/m, while revisions to prior months showed a stronger pace of consumer spending in April/May. Consumer spending is tracking around 2% annualized for Q2, a touch higher than Q1’s 1.5% but handily below the +3% pace averaged through the second half of last year.

Indeed, economic data out this week support the notion that while the economy is slowing, it’s not falling off a cliff. Retail sales were flat in June, but that was largely related to a sharp pullback in auto sales due to a cyber-attack on a software firm that supports car dealers across the country. Meanwhile, the control retail group – used in the BEA’s calculation of PCE – rose by a healthy 0.9% m/m, while revisions to prior months showed a stronger pace of consumer spending in April/May. Consumer spending is tracking around 2% annualized for Q2, a touch higher than Q1’s 1.5% but handily below the +3% pace averaged through the second half of last year.

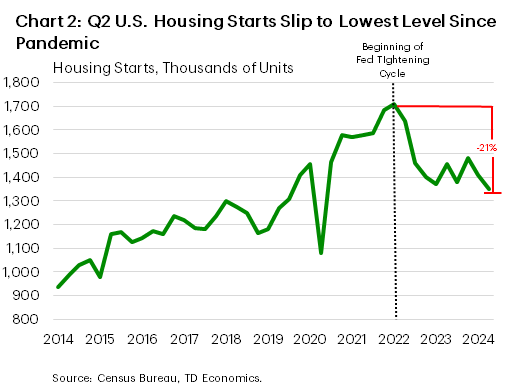

Meanwhile, industrial production data for June rose by a respectable 0.6% m/m and recorded its largest quarterly gain since Q2-2021. Encouragingly, the manufacturing index has now posted gains in four of the last five months and is closing in on levels not seen since the Federal Reserve first started hiking interest rates back in March 2022. Conversely, home building activity continues to feel the pinch of higher rates, with Q2 housing starts slipping to a new post-Fed tightening low (Chart 2).

All told, it’s becoming increasingly clear the U.S. economy is downshifting from last year’s breakneck rate of expansion to something closer to a trend-like pace. Provided the next two inflation readings don’t show any meaningful reversal in recent trends, the Fed likely has a clear path to start cutting rates in the coming months.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of June 28th, 2024

Financial News Highlights

-

- Headline PCE inflation came in flat for the month of May and core PCE inflation eased in financial news.

- Personal income posted a strong gain last month, while spending growth was more moderate, leading to an uptick in the savings rate.

- The heat in the economy still looks mainly to be in the service sector, as goods-producing industries contracted last quarter and goods prices continued to retreat in May.

Services Spending and Prices Starting to Settle

The past week had a relatively light data calendar for the U.S. economy, which continued on relative cruise control to gradually moderating economic growth and inflation in financial news. The current state of the economy was well summarized by Federal Reserve Board Governor Bowman in her speech earlier this week, which emphasized that we have seen only modest progress on inflation in 2024, despite moderating economic growth. The message holds true in the week’s data, which included an update on consumer prices and personal spending, as well as the revised reading on first-quarter GDP.

The past week had a relatively light data calendar for the U.S. economy, which continued on relative cruise control to gradually moderating economic growth and inflation in financial news. The current state of the economy was well summarized by Federal Reserve Board Governor Bowman in her speech earlier this week, which emphasized that we have seen only modest progress on inflation in 2024, despite moderating economic growth. The message holds true in the week’s data, which included an update on consumer prices and personal spending, as well as the revised reading on first-quarter GDP.

Inflation – as measured by the personal consumption (PCE) deflator – continued to moderate in May, with the core PCE deflator posting a ‘soft’ gain of 0.1% m/m – down sharply from the 0.3% gain registered the month prior. The deceleration in price pressures was entirely driven by another month of declines in goods prices and a further slowing in non-housing services prices. More critically, the three-month trend eased to a five-month low of 2.7% (annualized). Fed Governor Bowman repeated earlier this week that inflation has been slow to come down and more progress towards 2% is needed to support rate cuts this year. This morning’s data showed another (small) step in the right direction, though Fed officials will likely need to see at least another several ‘good’ inflation readings before having enough confidence to start dialing back the policy rate.

On the spending side, the release of May’s data showed some retrenchment in the goods and services split, with goods leading personal spending growth after having recorded declines in three of the four prior months. Overall, the softer gain in services spending implies our Q2 tracking for consumer spending is likely closer to 1.5%, which is a bit lower than what was assumed in our updated forecast published earlier this week.

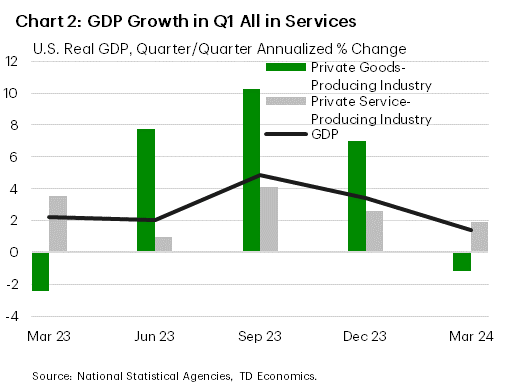

On the spending side, the release of May’s data showed some retrenchment in the goods and services split, with goods leading personal spending growth after having recorded declines in three of the four prior months. Overall, the softer gain in services spending implies our Q2 tracking for consumer spending is likely closer to 1.5%, which is a bit lower than what was assumed in our updated forecast published earlier this week.The last big piece of data out this week was the third estimate of first-quarter GDP. Usually, the 3rd estimate is not very exciting – after all, the first estimate was released two months ago, and revised minimally last month, only to be revised minimally again this week. Mostly old news, in that sense, but in the 3rd estimate we do get one new piece of data: the first look at GDP by industry for the quarter. Here, two observations quickly become clear – goods-producing industries contracted in the first quarter following several quarters of high growth in 2023, and services-producing industries, which had been supporting growth for over a year now, posted moderate growth relative to the last two quarters. The moderation of services growth coinciding with the downtrend in services inflation is an encouraging combination.

Next week, we will be closely following Chairman Powell’s words at the European Central Bank’s policy extravaganza at Sintra for a better view of how the central bank is digesting the latest data. Markets and other observers will also be focused on next week’s jobs data for any signs that the cooling we have seen in spending and prices is spilling over to the labour market.

Vikram Rai, Senior Economist | 416-923-1692

The past week had a relatively light data calendar for the U.S. economy, which continued on relative cruise control to gradually moderating economic growth and inflation in financial news. The current state of the economy was well summarized by Federal Reserve Board Governor Bowman in her speech earlier this week, which emphasized that we have seen only modest progress on inflation in 2024, despite moderating economic growth. The message holds true in the week’s data, which included an update on consumer prices and personal spending, as well as the revised reading on first-quarter GDP.

The past week had a relatively light data calendar for the U.S. economy, which continued on relative cruise control to gradually moderating economic growth and inflation in financial news. The current state of the economy was well summarized by Federal Reserve Board Governor Bowman in her speech earlier this week, which emphasized that we have seen only modest progress on inflation in 2024, despite moderating economic growth. The message holds true in the week’s data, which included an update on consumer prices and personal spending, as well as the revised reading on first-quarter GDP.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of June 21st, 2024

Financial News Highlights

-

- U.S. retail sales grew marginally in May, however the downward revision in April points to waning momentum among U.S. consumers in financial news.

- Housing starts and building permits both declined in May as higher interest rates weigh on builder confidence.

- U.S. existing home sales dipped for a third consecutive month as record home prices stretch buyers’ affordability limit.

Housing Market Strains Under the Weight of Higher Rates and Prices

Data out this week was largely tilted to the housing market, providing an update on where things stand in the usually busy spring season. Thus far, the situation appears largely unimpressive as market activity continues to be impacted by the dowsing effect of higher interest rates and prices. Another look at the health of the U.S. consumer via the retail spending report was also in the lineup. Despite news on the economic front, activity is the stock market was largely driven by the ups and downs of Nvidia, which managed to dethrone Microsoft this week as the most valuable public company in the world. Bond prices also continued to rise, driving yields lower. At the time of writing, the 10-year Treasury yield was down 0.5 basis points relative to where they started the week.

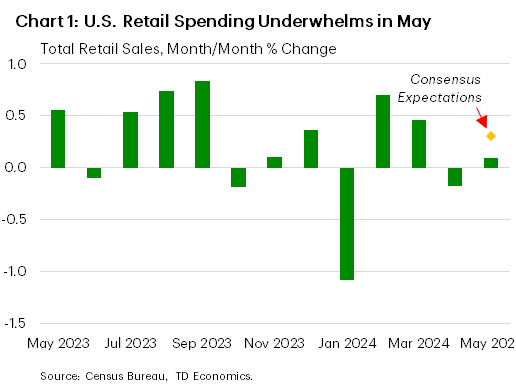

Consumer spending continued to show signs of fading as retail sales barely grew in May (0.1% m/m), following a decline of -0.2% in April. The outturn was weaker than analysts expected (Chart 1). Overall, weak retail sales are consistent with a U.S. economy that is losing momentum. The main takeaway is that consumers may finally be starting to yield to the pressures of elevated prices and higher borrowing costs.

Nonetheless, most Fed speakers throughout the week were key to emphasize that there is still more ground to be gained on the inflation front with the current restrictive policy before normalization becomes appropriate. In a recent interview, Fed Governor Barkin suggested that consumer spending is “fine” despite the weak retail sales print. In his view, “consumer spending is solid, not frothy and not weak” and the Fed is well positioned to respond to any path the economy may take. Other speakers, including New York Fed President John Williams and Boston Fed President Susan Collins, stressed the Fed’s data dependent approach in financial news. Williams noted that he expects “interest rates to come down gradually over the next couple of years” but declined to give specific timing, while Collins stressed the need for patience and time to assess the “constellation of available data.”

On the housing front, homebuilding activity retreated last month with a decline in both housing starts and building permits. A consistent pullback in permitting activity over the past few months, has resulted in a decline in the number of units under construction. Evidently, elevated interest rates are weighing not only on buyers, who have pulled back on new home purchases resulting in higher inventory, but also on builders as it increases the cost of construction financing.Despite a decline in the average 30-year fixed mortgage rate from a recent peak of 7.22% in early May to 6.87% this week, the housing market remains under pressure. Existing home sales slipped again for the third month in a row as home prices hit a record high (Chart 2). Buyers continue to be weighed down by high prices and rates, with little prospect of relief in the near term as the Fed continues to exercise patience with respect to rate cuts.

Looking ahead, the central bank’s preferred inflation gauge is out next week. Fed governors and market participants alike will be eager to see how much of the recent easing in the Consumer Price Index will flow through to the Personal Consumption Expenditure measure. Perhaps the Fed will find more of that “consistent data” they require to support a less restrictive policy stance.

Shernette McLeod, Economist | 416-415-0413

Data out this week was largely tilted to the housing market, providing an update on where things stand in the usually busy spring season. Thus far, the situation appears largely unimpressive as market activity continues to be impacted by the dowsing effect of higher interest rates and prices. Another look at the health of the U.S. consumer via the retail spending report was also in the lineup. Despite news on the economic front, activity is the stock market was largely driven by the ups and downs of Nvidia, which managed to dethrone Microsoft this week as the most valuable public company in the world. Bond prices also continued to rise, driving yields lower. At the time of writing, the 10-year Treasury yield was down 0.5 basis points relative to where they started the week.

Data out this week was largely tilted to the housing market, providing an update on where things stand in the usually busy spring season. Thus far, the situation appears largely unimpressive as market activity continues to be impacted by the dowsing effect of higher interest rates and prices. Another look at the health of the U.S. consumer via the retail spending report was also in the lineup. Despite news on the economic front, activity is the stock market was largely driven by the ups and downs of Nvidia, which managed to dethrone Microsoft this week as the most valuable public company in the world. Bond prices also continued to rise, driving yields lower. At the time of writing, the 10-year Treasury yield was down 0.5 basis points relative to where they started the week.

On the housing front, homebuilding activity retreated last month with a decline in both

On the housing front, homebuilding activity retreated last month with a decline in both This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of June 14th, 2024

Financial News Highlights

-

- In a widely expected move, the Federal Reserve held the policy rate steady in the target range of 5.25%-5.5% in major financial news.

- FOMC participants now expect fewer rate cuts this year, with the median projection showing just one cut by year-end (previously three).

- Consumer Price Index (CPI) inflation came in weaker than expected in May, with the core measure recording its softest monthly gain since August 2021.

The Data Will Light the Way

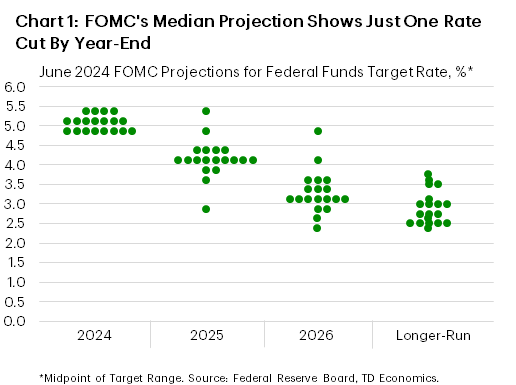

How quickly things can change! It was just six months ago that financial markets were positioned for six rate cuts by the end of this year. At the time, 50 basis points (bps) of cuts were expected to have happened by the June FOMC meeting. Well, that meeting has come and gone, and things haven’t quite shaped up as expected. The median forecast of FOMC participants is now showing just one rate cut by the end of this year. Bond traders are a bit more optimistic, currently pricing for two cuts, after a very soft CPI reading this week. A faster cooling in inflationary pressures helped to catapult the S&P 500 higher by over 1% on the week, while the 10-year Treasury dipped by 22 bps landing at 4.21%.

In a widely expected move, the Federal Reserve kept its policy rate unchanged holding the target range at 5.25%-5.5% for the seventh consecutive meeting. Accompanying the announcement, the FOMC also released a revised Summary of Economic Projects (SEP). In terms of the macroeconomic forecasts, there were few changes made relative to March in financial news. Expectations for growth this year and next remained unchanged at 2.1% and 2.0%, respectively, while the unemployment rate saw a modest upward revision of 0.1 percentage points in 2025 (to 4.2%) and 2026 (to 4.1%). The inflation forecast was nudged higher, with core PCE now expected to hold steady at 2.8% (previously 2.6%) through year-end, before slipping to 2.3% (previously 2.2%) by the end of the next year.

The most notable change in the SEP came from the Committee’s view on the future expectations of the policy rate. On the surface, the updated median Fed funds rate projection appears considerably more hawkish – now showing just one cut for this year as opposed to the three penciled in back in March. But a closer look at the dispersion of forecasts shows that FOMC members are nearly split between one (seven participants) and two (eight participants) cuts by year-end (Chart 1). Four members expect to keep the policy rate unchanged until next year.Broadly speaking, the upward revision to the ‘dots’ is a direct result of inflation having firmed through the first three-months of the year. However, the April inflation data showed some reprieve on that front, and this week’s May reading on CPI came in considerably below expectations. Core inflation rose by just 0.16% month-on-month – it’s softest monthly print since August 2021. The underlying details of the report were also constructive, with services inflation showing a notable cooling – entirely driven by the ‘supercore’ component – while goods prices were flat on the month. Encouragingly, the three-month annualized rate of change on core CPI slipped to 3.3% – a pace of price growth more consistent with late-2023 (Chart 2).During the press conference, Chair Powell acknowledged the last two softer-than-expected readings on inflation. However, he also reiterated that inflation “remains far too high” and that the FOMC needs to “greater confidence” before easing monetary policy. Whether that can be achieved over the next few months remains to be seen. As Powell noted in the press conference, “the data will light the way”.

Thomas Feltmate, Director & Senior Economist | 416- 944-5730

How quickly things can change! It was just six months ago that financial markets were positioned for six rate cuts by the end of this year. At the time, 50 basis points (bps) of cuts were expected to have happened by the June FOMC meeting. Well, that meeting has come and gone, and things haven’t quite shaped up as expected. The median forecast of FOMC participants is now showing just one rate cut by the end of this year. Bond traders are a bit more optimistic, currently pricing for two cuts, after a very soft CPI reading this week. A faster cooling in inflationary pressures helped to catapult the S&P 500 higher by over 1% on the week, while the 10-year Treasury dipped by 22 bps landing at 4.21%.

How quickly things can change! It was just six months ago that financial markets were positioned for six rate cuts by the end of this year. At the time, 50 basis points (bps) of cuts were expected to have happened by the June FOMC meeting. Well, that meeting has come and gone, and things haven’t quite shaped up as expected. The median forecast of FOMC participants is now showing just one rate cut by the end of this year. Bond traders are a bit more optimistic, currently pricing for two cuts, after a very soft CPI reading this week. A faster cooling in inflationary pressures helped to catapult the S&P 500 higher by over 1% on the week, while the 10-year Treasury dipped by 22 bps landing at 4.21%.

Broadly speaking, the upward revision to the ‘dots’ is a direct result of inflation having firmed through the first three-months of the year. However, the April inflation data showed some reprieve on that front, and this week’s May reading on CPI came in considerably below expectations. Core inflation rose by just 0.16% month-on-month – it’s softest monthly print since August 2021. The underlying details of the report were also constructive, with services inflation showing a notable cooling – entirely driven by the ‘supercore’ component – while goods prices were flat on the month. Encouragingly, the three-month annualized rate of change on core CPI slipped to 3.3% – a pace of price growth more consistent with late-2023 (Chart 2).

Broadly speaking, the upward revision to the ‘dots’ is a direct result of inflation having firmed through the first three-months of the year. However, the April inflation data showed some reprieve on that front, and this week’s May reading on CPI came in considerably below expectations. Core inflation rose by just 0.16% month-on-month – it’s softest monthly print since August 2021. The underlying details of the report were also constructive, with services inflation showing a notable cooling – entirely driven by the ‘supercore’ component – while goods prices were flat on the month. Encouragingly, the three-month annualized rate of change on core CPI slipped to 3.3% – a pace of price growth more consistent with late-2023 (Chart 2).This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.

Financial News for the Week of May 31st, 2024

Financial News Highlights

-

- Revisions to economic growth in the first quarter featured a mark down to consumer spending in financial news.

- That theme continued in April, where a contraction in real personal consumption expenditures came as a confirmation that restrictive rates are working.

- Inflation also took another step in the right direction. But sticky services inflation still has room to fall before the Fed can feel confident that inflation has been tamed.

A Slight Downshift

Bond yields are climbing down from this week’s highs as a pair of high-profile data releases suggest the some of the steam is being let out of the U.S. economy in financial news. While there isn’t anything released this week that is going to meaningfully move the needle on the timing of the Fed’s decision, it was encouraging to see that the current restrictive policy stance is cooling the economy. That said, there is still enough strength underlying the economy to keep the Fed’s policy rate right where it is until later this year.

First up was the refresh of the first quarter’s GDP data. Top-line economic growth was shaved down a smidge, to a below trend 1.3% quarter-on-quarter (q/q, annualized) change. Consumer spending too was marked down, from 2.5% to a more trend-like 2.0%. That said, faced with persistently strong price growth and high interest rates, the ability of households to keep buying stuff and spending money on experiences has defied expectations. Specifically, the shift back to services spending has kept demand up on the primarily domestic portion of the economy facing a tight labor market. Moreover, there is room for this trend to run if households continue to adjust their expenditures back towards a pre-pandemic mix, where household services consumption accounted for just shy of 66% of personal consumer expenditures (compared to 64.6% as of April, Chart 1).

So, it came as a welcome surprise that April’s Personal Consumption and Expenditures (PCE) survey showed real PCE pull back 0.1% month-on-month (m/m). More good news came as the core PCE deflator edged down to 0.2% m/m, leaving the annual pace of price growth to 2.8%. That said, the three- and six-month core PCE inflation rates are still 3.5% and 3.2% (annualized), respectively, as the past few months of strong price growth continue to be felt.

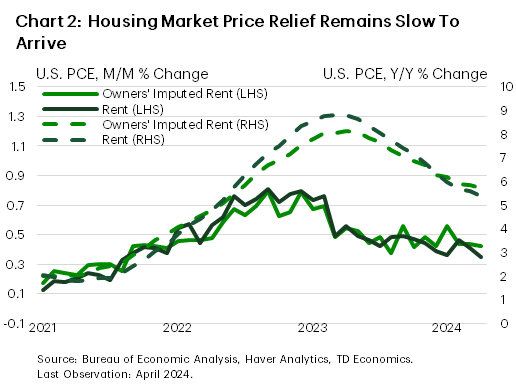

Importantly, while the deceleration in core price growth was welcome, special attention has to be paid to rents and housing costs that have been propping up core price growth. Together the two categories make up roughly 15% of PCE and will be critical to taming inflation. On this front, there was only marginal relief in April. Rent inflation came in at a “soft” 0.4% m/m (the print was 0.35% m/m unrounded). This is in line with the average reading from the prior five months (Chart 2). On the homeownership side too, implied rents came in at the same 0.4% m/m, roughly unchanged from the last few months. Sustained over a year, the 0.4% monthly pace would translate to 4.9% annual growth. The annual rates on the two shelter components are now cruising along at 5.7% and 5.4% for the imputed and actual rent measures, respectively.

For the Fed, April’s data were a step in the right direction, but there is still more work to be done before rate cuts become imminent. So now, all eyes are focused on data coming next week, and specifically the May payrolls report. After April’s real spending and payrolls data surprised to the downside, the focus will be for any signs that the month was not a one-off and weaker momentum continued into May.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.