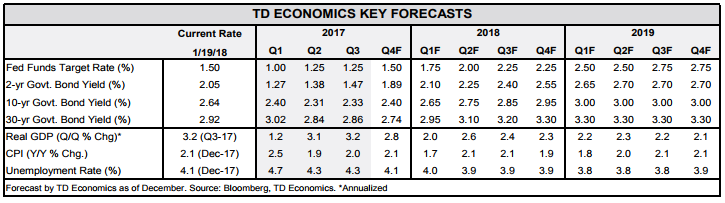

Financial News for the Week of January 26, 2018

HIGHLIGHTS OF THE WEEK

- U.S. economic data was relatively constructive this week; existing home sales remained near their multiyear highs, while real GDP expanded by a robust 2.6% (annualized) to cap off last year.

- The IMF upgraded its global economic forecast to 3.9% for this year and next. Managing Director Lagarde hailed it the “broadest synchronised global growth upsurge since 2010.”

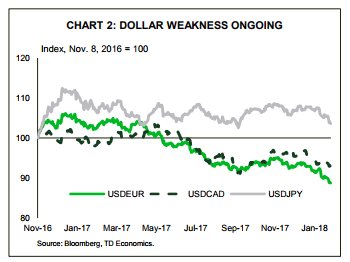

- This year’s Davos meetings were focused on trade, with Trump, Ross and Mnuchin forming the core of the U.S. delegation. The Treasury Secretary grabbed headlines saying that a “weak dollar is good” for the U.S.

- The ECB and BoJ stood pat on rates, with the Fed likely to follow suit next week at Chair Yellen’s last meeting.

Greenback Takes a Beating on Davos Comments

U.S. data was also relatively constructive. Existing home sales remained near multi-year records. Housing markets will have to contend with rising rates and lack of for-sale inventory, but will remain supported by above-trend growth and diminishing slack. U.S. real GDP capped the year with growth of 2.6% (annualized) in Q4 - more than half a point above its potential rate.

Robust U.S. growth comes alongside a solid global backdrop. This week, the IMF updated its global economic forecast to 3.9% for this year and next – 0.2 pp higher than before. The Fund’s Managing Director Lagarde, speaking in Davos, hailed this the “broadest synchronised global growth upsurge since 2010”, also highlighting that trade remains a “significant engine of growth.”

Still, America’s protectionist policies remain a worry. The U.S. this week levied tariffs on washing machines and solar panels. Defending the move, Commerce Secretary Ross stated that the U.S. approach to trade policy is dated, indicating that he is trying to right past wrongs and that the U.S. is done being “a sucker” or “a patsy” on trade.

But, it was Treasury Secretary Mnuchin that grabbed most headlines, stating that “a weaker dollar is good,” – a reversal of U.S. Treasury mantra. A broad U.S. dollar selloff followed, despite attempts by Ross and Trump to repair the damage.

Mnuchin’s comments were criticized by ECB President Draghi who referred to an international agreement last October not to talk down currencies. Speaking after the ECB kept policy rates unchanged this week, Draghi insisted that the bank would consider loosening policy to offset “unwarranted” tightening related to exchange rate. The ECB is unlikely to tighten policy until mid-2019, but is expected to let is bond-buying program lapse in September.

The BoJ also kept rates steady, only altering its inflation outlook wording from “weaker than expected” to “broadly unchanged.” And in what will be the last meeting headed by Chair Yellen, the Fed is also likely to stand pat next week. The incoming Chair, Jerome Powel, will take over on February 3rd, having been confirmed by the Senate this week. We don’t expect the policy to be dramatically altered by the change at the top, with our current view for three Fed hikes this year.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 19, 2018

HIGHLIGHTS OF THE WEEK

- Not even a looming government shutdown could dampen market optimism this week. More evidence of strong momentum in the economy saw equities gain ground, while Treasuries and the U.S. Dollar continued to fall.

- It remained a coin toss at time of writing whether Congress will reach a funding deal to avert a government shutdown at midnight. If government shuts down, many non-essential services won’t operate, and employees will not be paid.

- For markets, shutdowns have been modest negatives in the past. However, markets rallied in the last three. All told the U.S. economy has very solid momentum heading into 2018. A closure would be a slight hit to growth, but not derail the U.S. expansion.

Headed for a Shutdown?

As for that looming shutdown, the House passed a stop gap spending bill that would fund the government until February 16th, but it faces an uphill battle in the Senate. Any continuing resolution to fund the government needs 60 votes in the Senate, and the GOP only has 51 seats so it needs Democratic votes. Dems are opposed to the bill because they want it to deal with the fate of “Dreamers” – people who were brought to the U.S. illegally as children – whose protection from deportation expires in March. Congress has until then to pass a bill to address the Dreamers, but Dems are trying to use their leverage in the Senate to force the issue now. It is a political game of chicken, and at time of writing it is unclear whether a compromise can be reached by midnight tonight.

So, what happens if they don’t reach a deal? Well, we have a fair bit of experience with shutdowns – there have been 18 “funding gaps” since 1976, and three full shutdowns. The most recent shutdown in 2013 led to about 40% of federal government workers being furloughed, the equivalent of about 850,000 people.

In the event of a shutdown, essential services will remain in place, including roles like air-traffic controllers, armed forces, and law enforcement. The Federal Reserve is not funded by Congress, so it too would remain open for business. But, many “non-essential” operations would be closed, like national parks, statistical agencies and the IRS, causing disruption in the lives of many Americans, particularly those federal employees who will not be paid during the shutdown.

This would have a negative effect on growth in Q1. The Bureau of Economic Analysis (BEA) estimated that the last 16-day shutdown lowered real GDP by 0.3 percentage points (annualized) in Q4 2013. If the shutdown were to drag on, for example, for four weeks, it is estimated it would lower real GDP growth by 1.5 percentage points (annualized). Right now, first quarter growth is tracking just shy of 2 ½% annualized, strong enough to withstand the hit.

In the past, shutdowns have not been catalysts for market downturn. On average, markets have shown modest weakness, with the S&P 500 down 0.6% over the period of the closure. However, the index rose in 44% of past government shutdowns. In fact, during the last three, under Clinton & Obama, markets rallied. Given current market optimism on strong global growth, it seems unlikely that a shutdown would derail the rally.

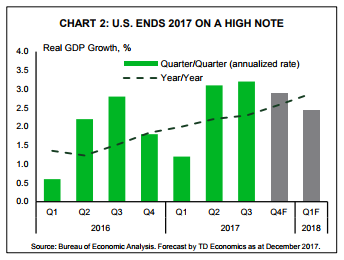

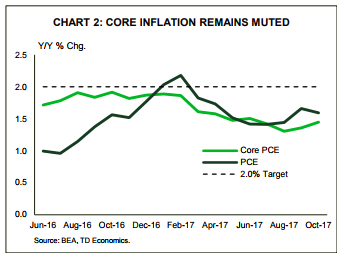

Markets do have solid economic reasons for optimism. Next week we see the first estimate of fourth quarter growth. We expect the U.S. economy ended 2017 with solid momentum at a near 3% annualized pace (Chart 2). That would corroborate the recent Beige Book, which showed widespread momentum across the country.

Leslie Preston, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of January 11, 2018

HIGHLIGHTS OF THE WEEK

- The second week of 2018 marked another strong performance in equity markets. While the advance did take a breather midweek, the main American stock indices resumed their upward trajectory, rising to new highs. The rally received an added fillip from oil prices, which gained additional ground, thanks in part to a bullish inventory report.

- Economic reports drove in the point that the U.S. economy ended the year on solid footing. Retail sales rose 0.4% m/m in December, while November sales received a healthy upward revision. Fourth quarter consumption growth is now expected to come in at around 3.3% (ann.), which should help propel growth forward by a robust 2.6% at year-end.

- On the inflation front, data out this morning suggests that price pressures appear to be building. Core CPI saw a stronger-than-expected 0.3% m/m increase, which lifted the y/y pace to 1.8%. Altogether, this week’s data helps bolster support for a March rate hike, with two more expected later this year.

Upbeat Data Bolster Case For March Hike

Economic reports reinforced the view that the U.S. economy ended the year on solid footing, setting the stage for robust momentum heading into 2018. Retail sales rose 0.4% m/m in December, while November received a healthy upward revision to 0.9% from 0.8% previously. Gains were broad based, with strength seen in categories such as building material, food & beverage, and non-store retailers. Considering these data, fourth quarter consumption growth is expected to come in at around 3.3% (annualized), which should help real GDP growth advance by a solid 2.6% at year-end.

Complementing strong consumer spending, small business owners remained upbeat. Although confidence pulled back slightly in December, the reading remained at historically high levels. Moreover, the recent upbeat trend in optimism has been accompanied by the increased difficulty in finding qualified workers (Chart 1). Given the tightness in the labor market, businesses will need to boost worker compensation in order to attract and retain talent. They will have an improved ability to do so thanks to tax reform which will lower some of the tax burden. This narrative, corroborated by an upward trend in the share of small businesses planning to raise compensation, provides additional comfort with regards to our inflation outlook.

On that note, inflation data out this morning suggests that price pressures appear to be falling into place. While headline inflation was held back by declining energy prices, recording only a

The potential for overheating, given the combined impact of fiscal stimulus and a tight labor market, may necessitate a slightly faster pace of hikes. But for now, we views risks for three hikes in 2018 as roughly balanced. For instance, the fact that core inflation has remained in the 1.7 to 1.8% range for the past eight months makes one month of strong data not very reassuring. Strength was also concentrated in a few key categories, which may not prove sufficient to buoy inflation on a sustained basis. A radical makeover of the Fed, which has a number of vacancies, along with the possibility of a government shutdown as early as next week, pose additional downside risks.

Admir Kolaj, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

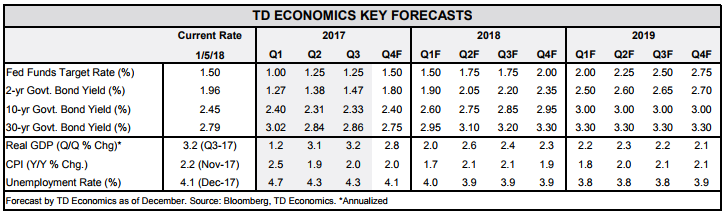

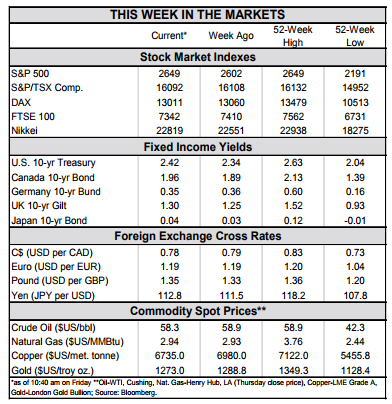

Financial News for the Week of January 5, 2018

HIGHLIGHTS OF THE WEEK

- Investors celebrated tax cuts by snapping up U.S. equities this week, extending last year’s record-setting rally into the first week of 2018. Energy stocks were lifted as WTI hit $62 for the first time since 2014.

- December’s solid jobs report capped the end of a stellar year for the labor market as the unemployment rate remained at a 17-year low of 4.1%. Overall, 2.2 million jobs were added in 2017.

- In 2018, tax cuts will provide employers with more ammunition for pay upgrades, which will help inflation edge higher. We expect the Fed to hike twice in 2018, with inflation expected to reach 2% later this year

Economy Added 2.2 Million Jobs in 2017

Production has been supported by solid spending figures, with U.S. vehicle sales in December being a prime example. Auto sales rounded out 2017 strongly, helping make the annual total the fourth best in history for auto dealers. Although pent-up demand for vehicles dwindled over 2017, sales in 2018 should continue to be supported by lengthening loan terms and tightening labor markets. Moreover, personal income tax cuts should provide an additional boost to demand.

Tax reform was also a topic discussed by the FOMC in December. The pace of monetary policy normalization could increase to offset any inflationary pressures that materialize from the plan. This prospect sent the U.S. dollar higher temporarily while the ten-year benchmark bond yield rose. Still, the Committee expressed concern over low inflation that has remained despite persistent labor market tightening.

Indeed, this morning’s data confirms that the U.S. labor market continues to tighten. December’s solid jobs report capped the end of a stellar year for the labor market as the unemployment rate remained at a 17-year low of 4.1% for the third consecutive month. Strong hiring brought the total jobs added in 2017 up to roughly 2.2 million, outperforming 2016 (Chart 2). As the labor market approaches full employment, the pace of hiring will subside as the unemployment rate stabilizes in the medium term. Employers will have to dole out larger pay increases in order to attract and retain workers. And, with tax cuts providing more ammunition for pay upgrades, it is just a matter of time before inflation edges higher. Additionally, the recent increase in commodity prices may squeeze profit margins further, and should translate into consumer price increases as the year progresses. Next week’s CPI report should illustrate the extent to which this has impacted price growth in December.

All told, the strong finish to 2017 provides ample momentum for a pickup in growth in 2018. We still expect the Fed to hike twice in 2018, assuming that inflation builds steadily, reaching the Fed’s 2% target later this year. However, political uncertainties still loom large. This includes a federal budget resolution, as temporary funding runs out on the 19th of this month. Although another short-term extension could be passed in order to curtail a government shutdown, several contentious issues will eventually need to be addressed.

Katherine Judge, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of December 22, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The Tax Cuts and Jobs Act was passed by Congress and signed by the President this week.

- The U.S. economy continues to show signs of strong momentum heading into 2018. Housing activity is recovering nicely from late summer hurricane-related disruptions, and consumer spending is on pace to expand at a 3.0% annualized pace this quarter.

- Looking ahead into 2018, political events in Europe are likely to continue to dominate headlines in the New Year.

Visions of Tax Cuts Dancing in our Heads

From an economist’s perspective, it’s difficult to be disappointed with how 2017 turned out. After a bumpy start to the year – courtesy of a phenomenon coined ‘residual seasonality’ – growth in the U.S. held at a 3.0% pace for the remainder of 2017, well above trend estimates at just under 2.0%. Moreover, stronger-than-expected growth became a global theme, as G7 economies broadly surprised to the upside. Since the middle of 2016, Canada, the U.S., the Euro Area, and even Japan reported growth well above trend estimates. Strong growth spurred central bank action, with the Fed raising rates thrice, but no longer alone in removing stimulus. The Bank of Canada raised rates twice in late summer, while the Bank of England followed with a rate hike in November. Not to be left out, the ECB followed through with earlier communication of reducing their pace of monthly asset purchases, halving them to €30 billion starting next month.

With the U.S. economy running hot, additional stimulus in the form of tax cuts seems unnecessary. But, after months of debate, Congress this week approved tax cuts that will leave American households and businesses with more money to spend for the next five to ten years. As covered in our note, we anticipate that the plan should help to stimulate economic activity in the medium-term, but at the expense of higher debt that may necessitate future cuts to entitlement spending, or higher taxes. Nevertheless, U.S. stock markets rallied in response to the news, while bonds markets sold off sending yields a touch higher on the week.

Heightened levels of economic optimism are to be expected with growth running hot globally. However, geopolitical events are stewing in the background, threatening to knock the current expansion off course. Looking ahead into 2018, concerns about North Korea’s military ambitions will remain, as will tensions between the major powers in the Middle East. And, like a broken record, political events in Europe remain on the radar. Phase two of Brexit negotiations are set to begin early in the New Year, and EU officials this week stated that they will have a EU-Canada style trade agreement in their pocket in case negotiations fail to make material progress by summer. Moreover, results from this week’s Catalonian election shows strong support for independence-minded parties, suggesting the potential for economic uncertainty to linger in Spain, the Euro Area’s fourth largest economy

Add elections in Italy, Sweden and Eastern Europe next year, and it’s clear European politics will dominate headlines for another year. We hope that once again strong 2,000 economic growth manages to trump uncertainty in 2018.

Fotios Raptis, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of December 15, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Economic policymakers in Washington squeezed a lot in this week before heading home for the holidays. As expected, the Fed raised rates a quarter point and upgraded their economic growth forecasts

- Republican members of Congress rushed to wrap up a compromise tax plan to be voted on early next week. While the final details are not yet known, the plan is likely to provide a modest boost to growth over the next few years. But, it has several potentially negative consequences for government finances over the longer-term.

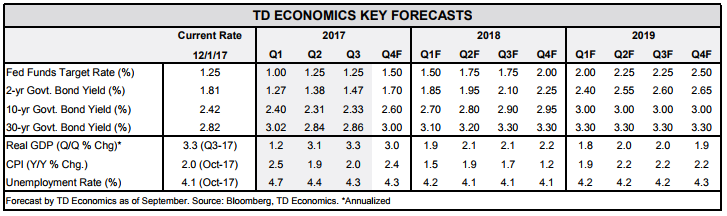

- Our Quarterly Economic Forecast also features an upgraded economic outlook, in part reflecting better momentum in the second half of the year, and fiscal stimulus.

Taxmas is Coming and the Debt is Getting Fat

The Fed also raised its economic growth forecast, but left its expectation for the number of rate hikes over the next year unchanged. The reason for the seeming inconsistency is unclear, but likely it is in part because of continued weakness in inflation would have necessitated a downgrade in the number of hikes, were it not for the offsetting growth upgrade.

All told, this is not a picture of an economy calling out for a fiscal boost. Moreover, deficit-financed tax cuts have several potentially negative consequences for the federal budget, and the economy

Finally, the plan is estimated to add about one trillion dollars to a debt burden that was already slated to grow due to rising expenditures from an aging population. This means interest costs will eat up more of the budget, leaving less room for other priorities. Larger government debt burdens also crowd out investment in the private sector, dampening productivity growth over the longer term. And, it raises the likelihood of a fiscal crisis – where interest rates on federal debt would rise suddenly and sharply as investors demand additional compensation to hold U.S. debt.

Leslie Preston, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of December 8, 2017

HIGHLIGHTS OF THE WEEK

- The Federal Reserve meets next week and is near-universally expected to raise interest rates by 25 basis points, bringing the target for the fed funds to a range of 1.25% to 1.5%.

- The U.S. labor market continues to make progress with 228k jobs added in November. Given the current rate of job creation, it is only a matter of months before the unemployment rate pushes below 4%.

- The American economy is likely to continue its winning streak. Even without tax cuts, 2018 is likely to see growth around 2.5%. With increasing prospects for fiscal stimulus to push growth even higher, the Federal Reserve will continue to remove monetary accommodation.

The Fed Can’t Ignore A 3-Handle On Unemployment

As the Federal Reserve meets next week to decide interest rate policy for the final time in 2017 it is faced with ebullient financial markets and an economy that is operating increasingly close to full capacity. With November’s gain of 228k jobs, the streak of positive job creation entered its 86th month. The unemployment rate in November held steady at 4.1% (a seventeen year low), but with job growth trending above 200k, it is only a matter of months before it pushes to lows not seen since the 1960s.

While there are some doubts about the strength of the relationship between unemployment and inflation, an unemployment rate that begins with a three handle is certain to raise eyebrows. The unemployment rate is already below the FOMC’s assumed neutral level of 4.6%, and other broader measures of labor market slack, such as long-term unemployed and the U-6 measure of labor underutilization, continue to trend lower.

The hope is that employer demand for labor will draw discouraged workers back into the labor force, but the pool of such potential workers is dwindling. Relative to the population, the share of people outside of the workforce (not actively searching for a job), who want a job now is at the same rate it was prior to the recession (Chart 1). The employment to population ratio of core working-aged women (between 25 to 54) has already regained its prerecession peak (Chart 2). The ratio is still lower for men, but it has been steadily declining for no less than seventy years. Subtracting the long-run trend, the ratio does not appear all that abnormal.

Even without tax cuts, the U.S. economy appears likely to continue its winning streak. Growth in the fourth quarter is tracking close to 3%. With supportive financial conditions, economic growth in the range of 2-2.5% appears likely over the next year. Into this environment, Congress looks increasingly likely to pass a tax cut that will raise the deficit and add as much as $1 trillion to the national debt over the next decade.

Any boost to growth from the proposed tax reform plan is likely to show up in higher wages and inflation, which may have to be offset by additional interest rate hikes. Our model simulations based on a Taylor Rule monetary policy reaction function suggest that for every 0.25 percentage points added to economic growth above its trend rate, the Fed should raise rates by an additional 25 basis points. While there is considerably uncertainty around the timing of tax cuts, investors should not discount the likelihood that what Congress giveth the Federal Reserve may taketh away.

James Marple, Director & Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

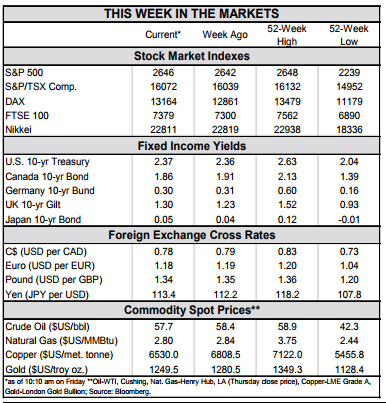

Financial News for the Week of December 1, 2017

HIGHLIGHTS OF THE WEEK

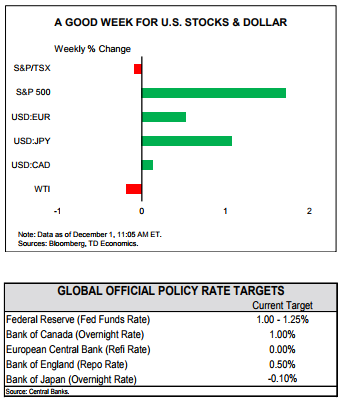

- The prospect of corporate tax cuts led both the Dow Jones Industrial Average and the S&P 500 to record highs this week, with financial stocks outperforming substantially.

- Economic data was supportive, with third quarter real GDP being revised up to 3.3% annualized, as business investment came in stronger than initially thought.

- Incoming Fed Chairman Jerome Powell stated that “conditions are supportive” of a December rate hike, and we expect the Fed to proceed with one, followed by two more in 2018.

Tax Cuts Just Around The Corner

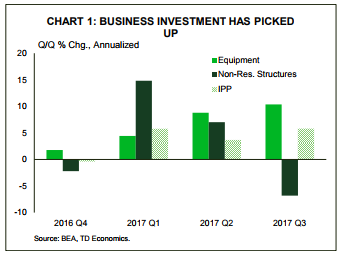

Economic data released this week also supported investor sentiment, with third quarter real GDP revised up to an impressive 3.3% as business investment accelerated (even more than previously estimated), with firms ramping up expenditures on equipment notably (Chart 1). This marks the strongest two consecutive quarters of growth for the American economy in three years. Momentum in business investment is expected to continue, with shale oil production likely to be a key contributor. Producers have ramped up activity this year in response to a rising price of WTI crude oil. OPEC’s commitment to extend supply cuts through 2018, announced this week, should maintain this momentum. As a result, the upside for the price of crude oil will be limited; we expect the price of WTI crude to sit in the US$50-55 range as the market balances out.

Incoming Fed Chairman Jerome Powell stated that “conditions are supportive” of a December rate hike at his confirmation hearing on Tuesday. Mirroring this view were Yellen and Kaplan in their speeches this week, in contrast to Kashkari who would like to see firmer evidence of inflationary pressures building before proceeding with a hike. At this point, markets are fully pricing in a December hike and we expect the Fed to proceed with one, followed by two more in 2018. Making this scenario increasingly likely is progress on the tax reform front which will require faster monetary policy normalization in order to temper the potential inflationary pressures

Katherine Judge, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of November 10, 2017

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- With little to digest on the data front, attention was devoted to political developments this week. Stock markets remained upbeat through Wednesday, given optimistic expectations on tax reform, supportive earnings reports and gains among energy stocks.

- However, market sentiment turned down thereafter, as developments on tax reform failed to meet expectations, given key differences between the House bill and the newly-released Senate bill.

- While tax reform will remain top of mind in the days ahead, a number of important data releases next week will help tilt the narrative back toward economic fundamentals, with emphasis placed on the upcoming CPI report.

Tax Bills: When Two Is Not Better Than One

Markets remained upbeat through midweek, given optimistic expectations on tax reform, supportive earnings reports and gains among energy stocks. The latter were buoyed by a surge in crude oil prices, with rising geopolitical uncertainty in the Middle East, particularly in Saudi Arabia, being the main catalyst behind the move (Chart 1). Global demand has been strong and OPEC discipline is expected to continue, but the risks for oil prices are skewed to the downside as non-OPEC production is on the rise, particularly U.S. shale. The EIA reported that U.S. production reached 9.62 million (B/D) last week, which is at the top range of historical highs.

In short, there are enough differences between the two bills to make immediate passage less likely. Much rides on tax reform, with expectations for major change being one of the main supporting factors behind the impressive post-election gains in stock markets (Chart 2). As such, the delay is likely to weigh on near-term sentiment, with prospects for a later introduction of corporate tax cuts of particular concern to investors.

Tax reform is likely to remain top of mind in the days ahead, but a number of important data releases next week will help tilt the narrative back toward economic fundamentals. Hurricane-related volatility should begin to taper off in upcoming reports, supporting the Fed’s decision-making process. With the economy still on a solid course and the labor market tightening further, we remain of the view that the Fed will hike rates once more by year’s end. But, this will require some cooperation from inflation metrics, with the emphasis placed on next week’s CPI report.

Financial News- November 10th, 2017

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.