Financial News for the Week of June 15, 2018

HIGHLIGHTS OF THE WEEK

- The FOMC raised the fed funds target rate by 25 bp this week. Additionally, median expectations for the fed funds target rose to 2.4% (from 2.1%), suggesting that the committee was leaning toward two more rate hikes this year.

- Data corroborated the Fed’s hawkish view of the domestic economy and faster removal of monetary accommodation. The headline and core consumer price indexes rose by 0.2pp (m/m) apiece to 2.8% (y/y) and 2.2% (y/y), respectively. Additionally, retail sales surged by 0.8% in May and small businesses expressed increased confidence in the outlook.

- While things are honky-dory for now, the threat of trade wars continues to percolate. This week the administration announced 25% tariffs on $50 billion of goods imported from China, which prompted retaliatory action by China.

Fed Raises Rate As Trade Risks Escalate

Tuesday’s inflation report got the ball rolling ahead of the FOMC rate announcement. As widely expected, inflation continued to gain traction in May. The headline and core consumer price indexes rose by 0.2pp (m/m) apiece to 2.8% and 2.2% (year over year), respectively. A strong economy, wage pressures and (now) tariffs will continue to push inflation measures higher in the coming months, particularly as businesses become more comfortable with passing higher costs to consumers (see Chart 1).

The Fed’s June rate hike looked like a done deal even before the inflation report, and indeed the FOMC raised the federal funds rate target by 25 basis points to a range between 1.75% and 2.0%. Details of the statement and the accompanying economic projections were insightful. Notably, the statement removed its forward guidance that the “federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run.” With committee member projections showing the federal funds rate rising above its anticipated “longer run” rate by 2019, this made sense. The Fed’s increased confidence in its rate hiking path was also illustrated in an edging up of the median expectation for the fed funds rate to 2.4% (from 2.1%) this year, implying two more rate hikes this year (one more than previously). During the press conference, Chairmen Powell also said that starting next year he will be holding a press conference following every FOMC meeting, a move likely aimed at freeing up Fed’s hands somewhat with respect to future rate changes.

While the U.S. economy may be sizzling, there are risks on the horizon. As with tariffs on steel and aluminum, the recent tariff announcement on Chinese goods sparked a retaliatory action by China. Taken alone these tariffs are likely to present a modest drag on U.S. growth and modest lift to inflation (please see our recent report on U.S.-China tariffs). However, while direct impacts are modest, the hit to business confidence and supply chain disruptions could result in a more deleterious effect on growth, So far, financial markets have taken these skirmishes in stride, but a further escalation or full out trade war could bring this assumption into question.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 8, 2018

HIGHLIGHTS OF THE WEEK

- Next week the Federal Open Market Committee (FOMC) will meet for the fourth time this year to discuss whether the current level of monetary stimulus is appropriate for the U.S. economy.

- Well above-trend economic growth and inflation at target should be enough to convince the FOMC to move its main policy rate up by 25 basis points.

- Elevated geopolitical uncertainty is likely to keep the FOMC on its current course of gradual rate hikes.

FOMC Locked in for Second Rate Hike of 2018

Next week the Federal Open Market Committee (FOMC) will meet for the fourth time this year to discuss whether the current level of stimulus is appropriate for the U.S. economy. During their discussions they will evaluate the health of the economy, wage and price pressures, and emerging risks before deciding on revisions to their outlook for economic activity, inflation, and the future path of the fed funds rate.

Strong economic activity is working to absorb any remaining spare capacity. The unemployment rate is at an eighteen year low, and as of April there were more job openings than there were job seekers (Chart 1). Wage growth is healthy by historical standards, but should move even higher as skilled labor becomes scarce. But, wages typically keep up with productivity growth, and on that front the U.S. economy continues to perform below historical trends (Chart 2).

Altogether, this solid outlook should be more than enough to convince the FOMC that the U.S. economy does not require the amount of monetary stimulus currently on offer. As a result, the fed funds rate is likely to move up by 25 bps next week, with another hike or even two embedded in the updated dot plot summary for this year.

That said, although further rate hikes are certain, their exact timing is still open for debate. Geopolitical risks remain elevated, and a policy misstep or two may be just enough to send financial markets, business confidence, and global trade into a tailspin. Trade skirmishes could easily escalate into trade wars, particularly if talks fail to make progress between the U.S. and its major trading partners. Although much better prepared than in past tightening cycles, emerging markets remain at the mercy of nervous investors who are more concerned with capital retention than returns in such an uncertain environment. Argentina and Turkey were the first victims of speculative attacks, but they surely will not be the last during this tightening cycle. All told, in light of these and other risks, the FOMC is likely to stay on its current path of gradual rate hikes.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of June 1, 2018

HIGHLIGHTS OF THE WEEK

- Fears of fresh elections in Italy spooked investors, who unloaded Italian bonds – sending yields on short-term government debt skyrocketing. By the end of the week, Italy’s populist coalition was finally allowed to form a government. But far from closure, this likely marks the beginning of a new chapter that will test the Eurozone’s stability.

- The U.S. turned up the heat on trade tensions by announcing that it would go ahead with tariffs on $50B of Chinese goods, and that it would end the exemption on steel and aluminum tariffs for Canada, Mexico and the EU.

- By the end of the week, markets shrugged off the latest developments in Europe and on trade, supported by a string of positive U.S. data – in particular, a very healthy May payrolls gain of 223k and wage growth that accelerated to 2.7% y/y. The latest data cement the case for a Fed rate hike at its June meeting.

Nessun Dorma (No One Sleeps)

The theatrical twists and turns of this week’s events are worthy on an opera, with the opening act set in Italy. Political turmoil and fears that new elections in Europe’s fourth largest economy could strengthen the grip of Eurosceptic parties spooked investors, who began to unload Italian assets. This sent yields on short-term government debt skyrocketing (Chart 1). Investors also steered clear of other southern European debt, with short-term Spanish, Greek and Portuguese bonds also selling off. Concerns regarding new elections subsided as the week wore on, and these moves began to reverse course. By the end of the week the populist coalition was allowed to form a government. Still, the fact that the new Italian government – which favors tax cuts and spending

Markets were thrown another curve ball when the White House announced that it would be pushing ahead with tariffs on $50B of Chinese goods and end the exemption on steel and aluminum tariffs for the E.U., Canada and Mexico. These normally close allies pledged to challenge the tariffs through the WTO and NAFTA channels and levy retaliatory tariffs. At around $12.6B and $7.7B of U.S. products targeted by Canada and the E.U. respectively, and an estimated $4B in trade with Mexico, the amount of affected trade is still quite small. But the wide list of products marked for tariffs, which stretch from agricultural products to motorcycles, are sure to strike a sour cord with the U.S. Ultimately, the tariffs will make goods more expensive for the American consumer. In a prior analysis, in which we expected the exemptions for the allies to stay, we estimated that the tariffs would have a muted direct impact on U.S. economic activity and inflation. The recent events make us more confident that while the impact on U.S. economic activity is still expected to be limited, the tariffs are likely to boost consumer price inflation by at least 0.1 percentage points this year and next.

The latest data cement the case for a Fed rate hike on June 13th. But this is no time to fall asleep, with further policy rate normalization also requiring a watchful eye on developments out of Europe and the potential fallout from heightened trade tensions. For now, Nessun Dorma.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

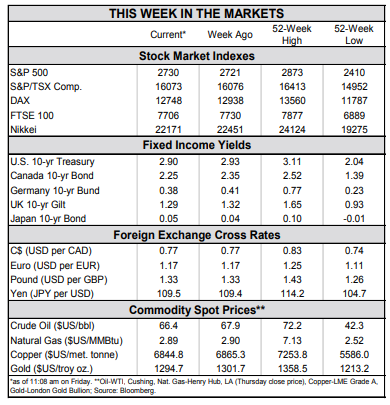

Financial News for the Week of May 25, 2018

HIGHLIGHTS OF THE WEEK

- U.S. trade tensions with China have temporarily subsided, however they have flared up elsewhere, as President Trump ordered a review of U.S. automotive imports.

- Trade tensions were also flagged as a key risk in the latest FOMC minutes. However, the Committee remained in agreement that it would soon need to “take another step” in removing monetary accommodation.

- Falling affordability and lack of inventory, continued to weigh on the U.S. housing market activity. After a weak first quarter, existing home sales have started the second quarter on a weak footing, falling 2.5% in April. Sales of new homes also declined during the same month.

Markets Respond to Geopolitics and the Fed

Financial markets rallied on Monday on the news of positive weekend developments in the U.S.-China trade dispute. Details of the agreement were vague and largely unquantifiable as far as trade deficit reduction targets are concerned. In the follow-up statement China agreed to “meaningfully” increase imports of U.S. agricultural and energy products, and lowered tariffs on imports of autos and parts. These relatively limited concessions were sufficient to put the proposed tariffs on $50 billion worth of Chinese goods set to take effect on May 21 on hold.

Although U.S. trade tensions with China have eased for now, they have flared up elsewhere, weighing on market sentiment later in the week. On Wednesday President Trump ordered a review of automotive imports, citing national security concerns. The decision drew sharp international criticism and warnings of retaliatory tariffs, but was also opposed domestically. Automakers as well as Republican lawmakers expressed concerns that, if imposed, auto tariffs will raise auto prices for consumers, disrupt supply chains, start trade wars and alienate U.S. allies.

Higher interest rates will certainly have an impact on the housing market. After declining by 6% in the first quarter, existing home sales have started the second quarter on a weak footing as activity fell 2.5% in April. Sales of new homes also took a break in April, declining by 1.5%. Since the start of the year, the average rate on a 30-year mortgage rose by 70 basis points. Rising rates alongside brisk growth in home prices have dented affordability; however, this is only part of the story behind relatively tepid home sales. Low inventory of houses on the market has been the most important factor restraining resale activity (Chart 1), but the pace of construction remains modest and will likely be contained by labor shortages and rising input costs. The price of American steel rose 40% this year, while lumber prices are up 34%. Some relief to the housing shortage may come as more existing homeowners, with fully rebuilt home equity (Chart 2), become encouraged to list their homes. However, the overall pace of activity in the housing market will likely once again remain modest this year.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 18, 2018

HIGHLIGHTS OF THE WEEK

- Equity markets were buffeted by plenty of anxiety-producing events from uncertainty on trade negotiations to right wing coalitions in Italy. Americans may also be a bit nervous about higher prices, both at the pump and for borrowing.

- The rise in oil prices is expected to be a modest drag on consumer spending. Ditto for mortgage rates and the housing market. Much of this was anticipated, and had already been baked in to our last quarterly forecast.

- We continue to expect growth to run around 3% over the remaining quarters of 2018 as the boost from fiscal stimulus offsets these modest headwinds.

Onwards and Upwards

Drivers may be getting sticker shock as they fill up their tanks, with the national average gasoline price approaching $3 per gallon. However, about half of the 10% rise in gasoline prices since March is the typical seasonal increase. Still, this will leave a bit less cash in wallets for spending on discretionary items. To put some numbers to it, in 2017 each American consumed about 442 gallons of gasoline per year, so a 5% increase works out to about $62/month for a family of four.

Higher oil prices are acting to drive inflation expectations, and consequently Treasury yields, higher. The 10-Year yield reached 3.11% on Thursday, the highest level since mid-2011. For much of last year, we argued bond yields were too low, and now things are looking much more reasonable. What’s more, the latest readings on the economy are consistent with higher bond yields. A healthy retail report for April demonstrated that consumers are back in action after taking a breather in Q1 Consumer spending growth in the second quarter is tracking close to 3% annualized, which would help to support a similar growth tally for the economy as a whole.

Mortgage rates have followed Treasury yields higher. The average rate on a 30-year fixed-rate mortgage rose to 4.61% this week, very close to the 2013 taper tantrum episode highs. The impact of higher mortgage rates is less far reaching than gasoline prices. It will only affect new borrowers and homeowners who are refinancing. The average new mortgage was $317,300 in March, so the impact of the 74 basis point increase in rates since the beginning of the year will raise the average monthly payment about $138 per month. This should hinder affordability in the housing market, and lean against demand.

That said, we remain confident that the positive fundamentals for housing will underpin gains in residential construction going forward. Housing starts may have been off a bit in April, but looking through the monthly volatility, the trend in the forward-looking permits data is still positive (Chart 2). Moreover, the monthly decline was due to the always volatile multi-family component. True, there are headwinds to homebuilding activity, including labor shortages in the construction industry, rising building material costs and a lack of buildable lots. But, after some weakness over the winter, homebuilder sentiment took a tentative step higher in May, suggesting these barriers are not insurmountable.

The pinch of higher prices and borrowing rates is expected to restrain consumer spending and housing investment slightly versus 2017’s performance. But, for the remainder of 2018 we expect business investment and government spending to power real GDP growth of around 3%.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

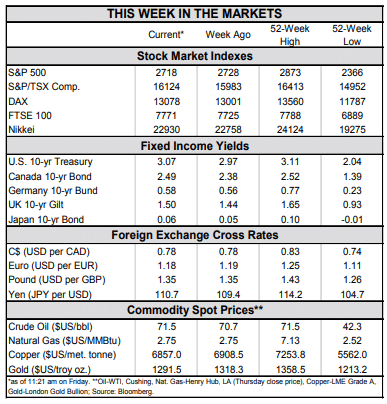

Financial News for the Week of May 11, 2018

HIGHLIGHTS OF THE WEEK

- Domestic equity markets shrugged off news that the U.S. administration is pulling out of the current Iran deal while leaving the door open to renegotiation.

- WTI oil rose for a fifth consecutive week. Rising U.S. gasoline prices helped drive headline inflation to 2.5% y/y, the fastest pace of price growth since February 2017.

- A loss of momentum in underlying inflation in April should help reduce concerns that the Federal Reserve isn’t moving fast enough to cool a hot U.S. economy.

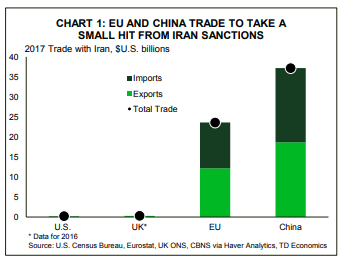

Upping the Stakes

Financial markets were caught somewhat off-guard by the decision, with conflicting news headlines generating gyrations throughout the day. Since a renegotiation of the deal is a possibility, markets shrugged off the news, with domestic equity markets likely to end the week up 2%. WTI oil prices also moved higher this week, holding above US$70 on this and other news of escalating Middle East tensions.

Abstracting from energy and other volatile prices, underlying price pressures remain fairly subdued despite strong economic activity and tightening labor markets. Core inflation lost some momentum in April, as price growth in core services slowed a touch. Still, core inflation registered a 2.1% gain year-on-year, but that includes a fading base-year effect from the dip in telecommunications prices last year that is acting to prop up inflation.

The loss of inflation momentum may help reduce concerns that the Fed isn’t moving fast enough to cool off a hot economy. Inflation is likely to hold near the Fed’s 2% target for the remainder of the year, with the economy running just hot enough to warrant two more rate hikes this year. That said, downside risks to the domestic and global outlook continue to materialize. Although they have had limited impact thus far, things can quickly escalate. While the Iran sanctions act to elevate the risk of a trade war between the U.S. and its trade partners, all parties appear open to dialogue. Still, this decision adds further pressure on Europe and China to settle trade imbalances with the United States.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of May 4, 2018

HIGHLIGHTS OF THE WEEK

- Investors were kept busy this week with plenty of top-tier data, both internationally and domestically, alongside a Fed meeting mid-week. International PMIs suggested some slowing in global economies, largely related to trade tensions.

- U.S. PMIs also pulled-back, but other data was far more constructive. Consumer spending accelerated to 0.4% in March, setting the second quarter on a solid growth path, which should come in near 3%.

- Firming inflation was the main story this week, with the PCE deflator (and core measure) accelerating to 2.0% and 1.9%, respectively. The Fed has taken notice of this, indicating in the statement a more confident view of the inflation outlook. This should enable the Fed to raise rates at least twice more times this year, with three hikes likely during 2019.

Fed Increasingly Confident On Inflation Outlook

International data this week revealed that economic momentum continued to slow in April. The most recent international PMIs softened somewhat, however much of the softness can likely be attributed to heightened trade uncertainty. Protectionist themes and tariffs have been making headlines on a regular basis, denting business confidence and stifling expansion plans. For instance, this week the Trump administration doubled down on demands for China to reduce its trade surplus with the U.S. by $200 billion.

Most critically, domestic businesses appear unable to escape the rising tide of trade protectionism. Both the manufacturing and non-manufacturing ISM indices pulled back 2 points apiece in April. However, they remain near cycle highs, and are indicative of ongoing healthy pace of growth.

mestic data confirms that growth remains solid despite the downside risks. Personal income rose by a healthy 0.3% in March, while consumer spending rose 0.4%, consistent with the narrative of tax cuts and rising jobs and wages motivating Americans to shop. A rebound in spending in the second quarter supports an outlook that sees economic activity expanding around 3%, a trend that we anticipate to hold through the end of the year.

This morning’s payroll report for April was consistent with this view despite the headline miss. Although wage growth slowed a touch, the drop in the unemployment rate to a 17-year low of 3.9% suggests that wage and price pressures should continue to gradually build.

Ultimately, inflation holding near target is consistent with our call for two more rate hikes from the Fed this year, with the next hike likely coming in June. That said, it’s not out-of-the question that the Committee raises rates by another 75 basis points this year. This gradual pace of tightening should help minimize the risk of slowing activity too quickly and resulting in a recession, something the FOMC officials are keenly trying to avoid..

Michael Dolega, Senior Economist | 416-983-0500

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of April 27, 2018

HIGHLIGHTS OF THE WEEK

- Financial markets moved sideways, rising in the first half of the week and sliding lower thereafter, but ultimately ending the week in the black.

- Economic data was more consistent, surprising to the upside. After three lackluster months, retail sales jumped 0.6% in March. Housing starts also posted a decent rebound rising by 1.9% on the month.

- Rising input costs stood out prominently in the latest Beige Book, but comments from Fed speakers saw little cause for alarm or the need for more aggressive interest rate increases.

First Quarter Growth Softens Less than Expected

Following a 4% annualized expansion in the fourth quarter that was partly boosted by post-hurricane recovery spending, consumer spending slowed markedly, contributing just a measly 0.7 percentage points to growth. Consumer spending should regain a firmer footing ahead, buoyed by upbeat consumer confidence, a healthy labor market and tax cuts. This narrative is corroborated by stronger monthly spending toward the end of the first quarter, including the surge in March retail sales and a second consecutive monthly gain in existing home sales. The latter rose 1.1% m/m, but the recent performance would have likely been even better if it weren’t for very tight inventories.

Overall, the better-than-expected GDP outturn and healthy outlook ahead may augur a faster pace of rate hikes. But the evolution of price pressures will be the deciding factor. On that front, higher oil prices this week –WTI reached $68/barrel for the first time since late 2014 – accentuated concerns about rising inflation. This helped push Treasury yields higher, with the 10-year yield briefly breaching the 3% mark for the first time since 2014. The rise in yields propped up the trade-weighted U.S. dollar and weighed on equity valuations midweek. But a slew of broadly positive earnings reports, coupled with the upside surprise on GDP, eventually helped markets recover losses.

Ultimately, we believe that there is still time for the U.S. and China to settle their trade differences without much collateral damage – something that appears more likely now with the Treasury secretary scheduled to embark on a trip to China shortly. However, there is still a possibility that the talks fail and tariffs are implemented, with this scenario expected to weigh on economic growth. In a recent report that considers the impact on regional economies, focusing on TD’s East Coast footprint, we find that the Eastern Seaboard is roughly half as exposed to trade with China compared to the rest of the country combined (Chart 2). This would enable most states in the footprint to duck much of the blow from the prospective tariffs. That said, South Carolina’s elevated trade with China leaves it’s economy more vulnerable to the economic drag from protectionist trade policy.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of April 20, 2018

HIGHLIGHTS OF THE WEEK

- Financial markets moved sideways, rising in the first half of the week and sliding lower thereafter, but ultimately ending the week in the black.

- Economic data was more consistent, surprising to the upside. After three lackluster months, retail sales jumped 0.6% in March. Housing starts also posted a decent rebound rising by 1.9% on the month.

- Rising input costs a stood out prominently in the latest Beige Book, but comments from Fed speakers saw little cause for alarm or the need for more aggressive interest rate increases

The Fed Preaches Patience Amid Rising Inflation Tide

Markets moved sideways this week, rising in the first half and sliding thereafter, even as energy stocks rallied. Still, there was no shortage of economic data and Fed speeches, giving investors plenty of news to digest.

Rising inflationary pressures also stood out prominently in the latest Federal Reserve Beige Book. Businesses reported rising steel prices in the aftermath of the tariff announcement. Prices for building materials, such as lumber, drywall, and concrete, also continued to rise briskly. Transportation costs, meanwhile, increased on the back of higher fuel prices, with oil prices rising to the highest level in more than three years this week. Labor shortages were also reported across a wide range of industries and skills. All in all, businesses are increasingly facing rising input costs for both labor and raw materials, and with declining unemployment, strong economic growth and the risk of further tariffs, this trend looks set to continue. It is likely only a matter of time before companies pass these higher costs onto consumers, ultimately pushing inflation higher (see our recent report).

Nonetheless, this week’s many Fed speakers downplayed the need for faster rate hikes. New York Fed President William Dudley said that the case for “tightening policy more aggressively is not compelling”. Meanwhile, Federal Reserve Vice Chair Randal Quarles said that he didn’t view recent flattening of the yield curve as a signal of an imminent recession. This suggests that the Fed remains on track (but not in a hurry) for continued gradual interest rate normalization.

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

Financial News for the Week of April 13, 2018

HIGHLIGHTS OF THE WEEK

- Financial markets bounced back from the selloff last week as trade tensions between China and U.S. eased somewhat.

- Both headline and core CPI inflation ticked up in March on a year-on-year basis.

- FOMC March meeting minutes indicate that some members contemplated a faster pace of rate hikes this year. Overall, we believe the balance of risks remains consistent with a total of three rate hikes in 2018.

Trade Deals (not Wars) Back on the Agenda

Although there has been more bark than bite on trade protectionism from the U.S. administration thus far, a hot trade war could do a lot of damage. However, events this week provide some hope that a trade war can be averted. Speaking at the Boao forum for Asia, Chinese President Xi repeated past promises to expand intellectual property protections and open various sectors of China’s economy to foreign investment. Later in the week, word spread that President Trump was directing officials to explore returning to the Trans Pacific Partnership, an agreement that he withdrew from shortly after coming to office.

Rising wages and input costs will eventually drive consumer prices higher. For the month of March, consumer prices rose 2.4% (year-on-year), but a more meagre 0.1% monthly change owing to decline in gas prices. Most importantly, core inflation (CPI ex-food and energy) ticked up to 2.1% y/y from 1.8% in the previous month, largely on the back of base-year effects (Chart 2). Still, core inflation rose a healthy 0.2% on the month, suggesting that a hot economy is leading to a broad build-up in price pressures.

Labor shortages, solid wage growth, and rising prices should reassure the Federal Reserve that higher interest rates are warranted. Although there was little new information in the March FOMC meeting minutes released this week, there were still some discussions worth noting. Strong economic growth along with rising price pressures are evidence that the economy is coping well with past rate hikes and can absorb more. In fact, some participants think that a total of four rate hikes may be warranted this year, while also suggesting that the language in the monetary policy statement be changed to reflect a view that interest rates are exerting a more neutral rather than accommodating impact on economic activity. Still, uncertainty about the ultimate impact of fiscal stimulus on output and the downside risks posed by trade protectionism is more consistent with a total of three rate hikes this year.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.